Japan has been a leader in mobile technology since its inception, and Japanese companies continue to occupy the cutting edge of mobile telephony. LTE networks in Japan have been able to deliver very competitive speeds in the densest urban areas, which speaks volumes about the cell density of the country’s networks. This article explores how Japanese mobile operators are applying this leading mindset to 5G.

How Japan utilizes spectrum

Japanese operators utilize a “layer cake” spectrum approach, which aggregates multiple frequency bands into data lanes that provide faster speeds. This approach utilizes low 700, 800 and 900 MHz bands, coupled with mid-band 1500 and 2100 MHz and topped off with the high-band 2500 MHz band. With this approach, users with modern devices are able to simultaneously access disparate spectrum bands, which enables better speeds and thus an improved user experience. Combined with Japan’s dense grid of existing cell sites, the spectrum layer cake should provide a good base for the overlay of sub-6 GHz spectrum that Japan has allocated for 5G services.

Timelines for launching 5G in Japan

For the past few years, Japan has been building toward the 2020 Summer Olympic Games in Tokyo as an opportunity to showcase their next-generation wireless technology. Japan began conducting 5G trials as early as 2017. In 2018, Japan’s Ministry of Internal Affairs (MIC) revised the spectrum allocation process to encourage new operators to enter the 5G market. Then in April 2019 the MIC approved 5G spectrum allocations to four applicants: KDDI (au), NTT DOCOMO, Rakuten Mobile and SoftBank.

KDDI, NTT DOCOMO and SoftBank launched 5G this month, with NTT DOCOMO and KDDI first to market on March 25. NTT DOCOMO’s initial 5G launch will leverage sub-6GHz spectrum assets, offering peak download speeds of up to 3.4 Gbps, and peak upload speeds of up to 182 Mbps. Later in June, the operator will start selling 5G devices capable of operating on the mmWave band and accessing 400 MHz of high-band spectrum. This will allow for peak download speeds of 4.1 Gbps and upload speeds of 480 Mbps. SoftBank will launch second on March 27. Rakuten plans to launch 5G by June 2020.

How Japanese operators will use spectrum for 5G

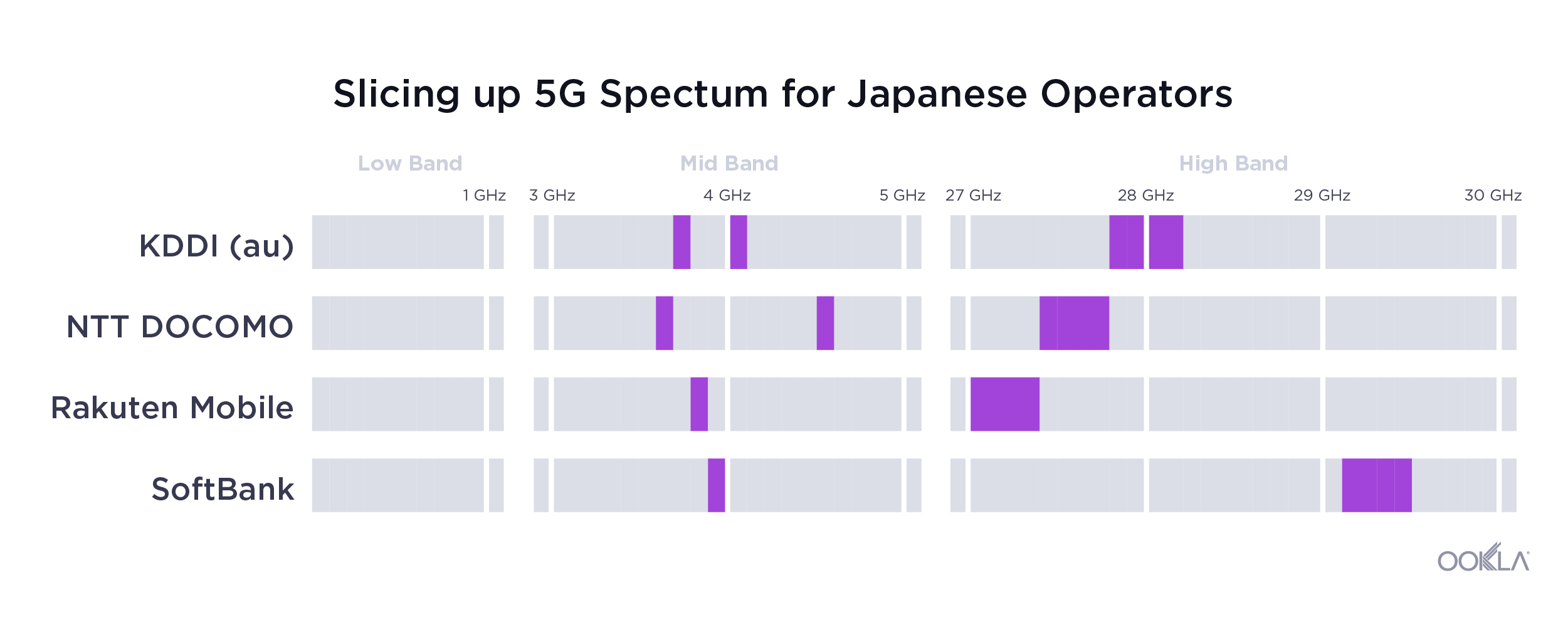

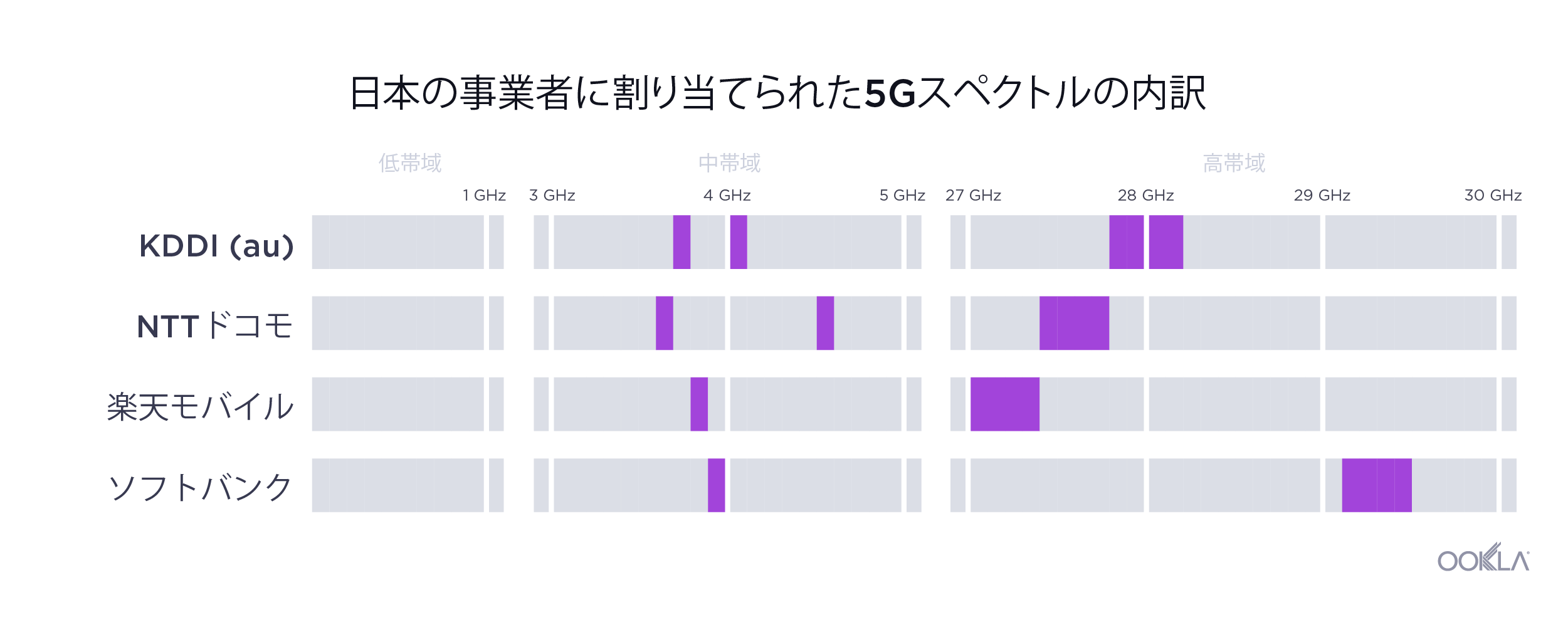

Japanese operators are deploying 5G networks in both FR1 (sub-6GHz) and FR2 (millimeter-wave) frequency bands. Each licensee has been awarded 400 MHz of FR2 spectrum and KDDI, NTT DOCOMO and SoftBank have been awarded 200 MHz of FR1 spectrum. The exception is Rakuten, which requested 100 MHz of FR1 spectrum.

Early trials and infrastructure

KDDI (au) 5G trials started in 2017 with Ericsson, Nokia and Samsung. KDDI awarded all three vendors with 5G contracts. KDDI also inked a seven-year roaming deal with Rakuten, the newest entrant in the wireless space, to provide LTE coverage to Rakuten’s subscribers when they roam outside of their coverage area.

NTT DOCOMO started early 5G trials using several infrastructure partners, including: Nokia and NEC Corp on 4.5 GHz spectrum band, Ericsson and Qualcomm on 4.5 GHz and the mmWave wave, and Huawei for mmWave. Fujitsu has proposed a software upgrade for existing LTE base stations which will enable 5G radio access. NEC Corp offered a small cells product supporting all three frequency bands (3.7 GHz, 4.5 GHz, 28 GHz) leveraging O-RAN (Open Radio Access Network Alliance), which aims to break the single-vendor-per-market lock and paves the way for a smooth transition to 5G software-defined networking and cloud services. NTT DOCOMO awarded NEC Corp, Fujitsu and Nokia with contracts, claiming the world’s first 4G/5G multi-vendor RAN (radio access network) interoperability.

SoftBank initially partnered with Chinese vendors Huawei and ZTE in 2017 to conduct mmWave trials in the 28 GHz frequency band. SoftBank awarded the contracts to Nokia and Ericsson.

A completely new approach from Rakuten, the “optimistic” entrant

Rakuten is a premier Japanese ecommerce company founded in 1997. Rakuten means “optimism” in Japanese, and now the company offers products and services across a multitude of industries, including: banking, mobile payment, mobile messaging (via the Viber app), travel and their own MVNO, to name a few. The company understands the importance of controlling the entire user experience for their customers — and the value of running their own facilities-based mobile network in addition to OTT (over-the-top) services.

Since Rakuten is deploying a mobile network from the ground up using greenfield licensed spectrum assets, the company has decided to do something that nobody has ever done before: disaggregating the hardware from the software and running a fully virtualized, cloud-native network. This LTE network has been fully operational with over 3,000 cell sites in three markets (Tokyo, Nagoya and Osaka) running limited trials since last year — and is expected to launch commercially on April 8. Because of its software-defined nature, the network can be upgraded to 5G, and the operator expects to have the upgrade pushed later this year.

Rakuten’s network architecture is unique, leveraging only antenna-integrated radios from traditional telecom vendors. Radios are fiber-fed via the fronthaul, and instead of processing at cell site cabinets, all the processing is happening remotely at centralized locations using off-the-shelf computer hardware running virtualized network functions. According to Rakuten CTO Tareq Amin, the process of activating a new cell site takes only eight and a half minutes instead of days. After Rakuten’s April launch, years worth of Rakuten’s research and development will be available to other operators globally via the Rakuten Mobile Platform (RMP), which could be very attractive to new entrants in the wireless space, such as DISH in the United States.

We will continue to monitor how these different 5G setups perform as 5G is rolled out in Japan and we look forward to providing future analysis on this topic.

日本国内における5Gへのユニークなアプローチ

日本は当初からモバイルテクノロジーのリーダーであり、日本企業は最先端のモバイルテレフォニーを占有し続けています。日本のLTEネットワークは、最も人口密度の高い都市地域でも非常に競争力のある速度を継続的に提供しています。これは、この国のネットワークの基地局密度の高さを物語っています。この記事では、日本の携帯電話事業者がこのような先進の考え方を5Gにどのように適用しているかを探ります。

日本のスペクトル活用法

日本の事業者は、複数の周波数帯域をデータレーンに集約して速度を高める「レイヤーケーキ」スペクトルアプローチを活用しています。このアプローチでは、700 MHz、800 MHz、900 MHzの低帯域と1500 MHz、2100 MHzの中帯域を組み合わせて、その上に2500 MHzの高帯域を乗せますこのアプローチにより、最新の電話機を所有するユーザーはさまざまなスペクトル帯域に同時にアクセスできます。これにより、高速化とそれに伴うユーザーエクスペリエンスの向上が実現します。このスペクトルレイヤーケーキと日本の既存の高密度基地局網との組み合わせは、日本が5Gサービスに割り当てた6 GHz以下のスペクトルのオーバーレイの良い基盤となります。

日本における5Gのローンチのタイムライン

日本は、2020年に東京で開催される夏季五輪を、次世代ワイヤレステクノロジーをアピールする機会ととらえ、ここ数年それに向けて準備を進めてきました。日本は、早くも2017年に5G実証実験を開始しました。2018年、日本の総務省は、新規事業者の5G市場への参入を促すため、スペクトル割り当て手続きを改訂しました。その後、2019年4月、MICは4つの申請企業への5Gスペクトル割り当てを承認しました。承認を受けたのは、KDDI(au)、NTTドコモ、楽天モバイル、ソフトバンクです。

KDDI、NTTドコモ、ソフトバンクは今月、5Gをローンチする予定です NTTドコモとKDDIが最初で、3月25日に発売された。NTTドコモの最初の5Gローンチでは、6GHz以下のスペクトルアセットを活用し、最大3.4 Gbpsのピークダウンロード速度と最大182 Mbpsのピークアップロード速度を提供します。7月後半、NTTドコモは、mmWave帯域で動作し、400 MHzの高帯域スペクトルにアクセスすることができる5Gデバイスの販売を開始する予定です。これにより、4.1 Gbpsのピークダウンロード速度と480 Mbpsのピークアップロード速度が可能になります。 ソフトバンクが2番目で、3月27日にローンチする予定です。楽天は2020年6月までに5Gを発売する予定です。

日本の事業者による5G用スペクトラムの使用方法

日本の事業者は、FR1(6GHz以下)とFR2(ミリメートル波)の両方の周波数帯域で5Gネットワークを展開しています。各ライセンシーは400 MHzのFR2スペクトルを割り当てられ、KDDI、NTTドコモ、ソフトバンクは200 MHzのFR1スペクトルを割り当てられました。例外は楽天です。楽天は100 MHzのFR1スペクトルを申請しました。

早期実証実験とインフラストラクチャ

KDDI(au)は、2017年にEricsson、Nokia、Samsungと共同で5G実証実験を開始しました。KDDIは、3つのベンダーすべてと5G契約を結びました。KDDIはまた、ワイヤレス市場の最も新しい参入企業である楽天と7年間のローミング契約を結び、楽天の加入者が楽天のサービス区域外でKDDIのLTEサービスを利用できるようにしました。

NTTドコモは、複数のインフラストラクチャパートナーと共同で早期5G実証実験を開始しました(4.5 GHzスペクトル帯域でNokiaとNEC、4.5 GHzとmmWave波でEricssonとQualcomm、mmWaveでHuawei)。富士通は、既存のLTE基地局を対象に、5G無線アクセスを可能にするソフトウェアアップグレードを実施することを提案しました。NECは、O-RAN(Open Radio Access Network Alliance)を活用して3つの周波数帯域(3.7 GHz、4.5 GHz、28 GHz)をすべてサポートする小型基地局製品を提案しました。このソリューションは、「市場ごとに1つのベンダー」体制を打破することを目的とし、5Gソフトウェアデファインドネットワーキングおよびクラウドサービスに円滑に移行するための道筋をつけるものです。NTTドコモは、NEC、富士通、Nokiaと契約を結び、世界初の4G/5GマルチベンダーRAN(無線アクセスネットワーク)相互運用をアピールしています。

ソフトバンクは当初、2017年に中国のベンダーであるHuaweiおよびZTEと提携し、28 GHz周波数帯域でmmWaveの実証実験を実施しました。ソフトバンクは、NokiaおよびEricssonと契約を結びました。

「楽観的」な新規参入企業である楽天のまったく新しいアプローチ

楽天は1997年に設立された日本の最大手eコマース企業です。楽天は日本語で「楽観主義」を意味しており、同社は現在、銀行、モバイル決済、モバイルメッセージング(Viberを使用)、旅行、楽天独自のMVNOなど、多数の業界に製品とサービスを提供しています。同社は、顧客のユーザーエクスペリエンス全体をコントロールすることの重要性と、OTT(オーバーザトップ)サービスに加えて独自の設備ベースのモバイルネットワークを稼働させることの価値を理解しています。

楽天は、認可を受けた未開発のスペクトルアセットを活用してモバイルネットワークをゼロから展開しているため、これまで誰もやったことがないことに取り組むことを決めました。それはハードウェアをソフトウェアから切り離し、完全に仮想化されたクラウドネイティブのネットワークを稼働させるというものです。このLTEネットワークは、3つの市場(東京、名古屋、大阪)で3,000以上の基地局によって完全に機能しており、昨年以降、限定的な実証実験が実施されています。商業ローンチは4月8日の予定です。このネットワークは、ソフトウェアデファインドの特性を持っているため、5Gにアップグレード可能で、楽天は今年の後半にアップグレードを行う予定です。

楽天のネットワークアーキテクチャは独特で、従来の電気通信ベンダーのアンテナ統合型無線のみを使用しています。無線は、フロントホールからファイバで送信され、基地局のキャビネットで処理される代わりに、リモートの集中拠点で仮想ネットワーク機能を実行する市販コンピューターハードウェアによってまとめて処理されます。楽天のCTOであるTareq Amin氏によると、新しい基地局は数日ではなくわずか8分半で稼働させることができます。楽天の4月のローンチ後、他の事業者は楽天モバイルプラットフォーム(RMP)を介して楽天の3年分の研究開発の成果を利用できるようになります。これはワイヤレス市場への新規参入を目指す企業(米国のDISHなど)にとって非常に魅力的でしょう。

私たちは、今後日本で5Gが展開されるにつれてこれらの異なる5Gセットアップがどのように機能するかを引き続きモニタリングしていきます。このトピックについての将来の分析を皆様にご提供できる機会を楽しみにしています。

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.