Ookla® Market ReportsTM identify key data about internet performance in countries across the world. This quarter we’ve provided updated analyses for 26 markets that include details on fastest mobile and fixed broadband providers, performance of most popular devices and chipsets, and internet speeds in cities. Click a country on the list below to see highlights or scroll through the article to learn what Speedtest Intelligence® revealed in all 26 markets:

Côte d’Ivoire: Speedtest Intelligence reveals there was no statistical winner among top mobile providers in Côte d’Ivoire during Q2 2022, with MTN showing a median download speed of 15.17 Mbps and Orange clocking in at 14.56 Mbps. There was also no statistical winner for fastest fixed broadband provider in Côte d’Ivoire during Q2 2022, though CANALBOX had a median download speed at 38.86 Mbps, Moov Africa at 34.41 Mbps, and Orange at 32.22 Mbps.

Jordan: Speedtest Intelligence finds fixed broadband provider Orange again provided the fastest median download speed in Jordan at 89.11 Mbps during Q2 2022, a modest increase over its speed in Q1 2022 (78.08 Mbps). Umniah was again the fastest mobile operator in Jordan during Q2 2022, delivering a median download speed of 33.74 Mbps.

Kenya: Mobile operator Safaricom had the fastest median mobile download speed in Kenya at 22.74 Mbps during Q2 2022. On fixed broadband, Faiba had the fastest median download speed (24.94 Mbps) and highest Consistency (50.6%) in Kenya during Q2 2022. At the city-level, Mombasa was home to the fastest mobile and fixed broadband download speeds at 23.59 Mbps and 12.03 Mbps, respectively, during Q2 2022.

Libya: Speedtest Intelligence reveals that mobile operator Libyana again had the fastest median mobile download speed in Libya at 12.34 Mbps during Q2 2022. Among top fixed broadband providers, AWAL Telecom had the fastest median download speed in Libya at 17.70 Mbps during Q2 2022.

Tanzania: Among top mobile operators in Tanzania, Halotel again had the fastest median download speed (17.12 Mbps) during Q2 2022. Mwanza had the fastest median mobile download speed among Tanzania’s most populous cities at 17.25 Mbps during Q2 2022.

Turkey: Speedtest Intelligence reveals mobile provider Turkcell again had the fastest median download speed and highest Consistency in Turkey at 54.62 Mbps and 92.2%, respectively, during Q2 2022. Among popular device manufacturers, Apple devices bested Samsung devices in Turkey at 41.77 Mbps compared to 30.55 Mbps during Q2 2022. For fixed broadband in Turkey, TurkNet again had the highest median download speed (49.46 Mbps) and Consistency (77.2%) during Q2 2022.

China: According to Speedtest Intelligence, fixed broadband provider China Unicom’s median download speed of 172.81 Mbps was the fastest in the country, overtaking China Telecom’s 162.30 Mbps in Q2 2022. The race for fastest 5G in China was likewise tight in Q2 2022, with China Mobile again edging out China Telecom 299.26 Mbps to 290.70 Mbps, with China Unicom following at 272.66 Mbps. Among top device manufacturers, Huawei devices had the fastest median download speed in China at 113.70 Mbps during Q2 2022.

Belgium: Telenet decisively retained its spot as Belgium’s fastest fixed broadband provider during Q2 2022, posting a median download speed of 129.30 Mbps. VOO followed at 111.93 Mbps. Among top mobile operators, Telenet/BASE again had the fastest median download speed at 76.09 Mbps, a modest rise over its speed in Q1 2022 (66.92 Mbps). Antwerp had the fastest median mobile download speed at 120.10 Mbps among Belgium’s most populous cities during Q2 2022.

Czechia: Speedtest Intelligence reveals T-Mobile was again Czechia’s fastest mobile provider during Q2 2022, recording a median download speed of 57.17 Mbps. When it comes to fixed broadband, Vodafone was again Czechia’s fastest fixed broadband provider during Q2 2022, delivering a median download speed of 90.60 Mbps. At the city-level, Brno was home to both the fastest mobile and fixed broadband median download speeds in Q2 2022.

Denmark: Fastspeed was Denmark’s fastest fixed broadband provider again during Q2 2022, achieving a median download speed of 283.79 Mbps. YouSee was Denmark’s fastest mobile operator, registering a median download speed of 125.76 Mbps during Q2 2022, which marked a modest increase over 115.87 Mbps in Q1 2022. The Apple iPhone 13 Pro Max and iPhone 13 Pro were ahead of the competition at 177.17 Mbps and 174.31 Mbps, respectively, during Q2 2022.

Estonia: According to Speedtest Intelligence, Elisa was again the fastest fixed broadband provider in Estonia during Q2 2022, achieving a median download speed of 77.19 Mbps. Telia again had the fastest median mobile download speed in Estonia at 71.48 Mbps during Q2 2022.

Finland: DNA edged out Elisa and Telia as Finland’s fastest fixed broadband provider in Q2 2022, recording a median download speed of 91.08 Mbps. DNA also took top honors as Finland’s fastest mobile operator at 72.24 Mbps. In addition, DNA had the fastest 5G download speed in Finland, achieving a median download speed of 279.95 Mbps.

Germany: Vodafone was Germany’s fastest fixed broadband provider during Q2 2022, earning a median download speed of 110.42 Mbps. Telekom achieved the fastest median mobile download speed (77.35 Mbps) and highest Consistency (88.9%) among top German mobile operators during Q2 2022. Telekom also took the top spot by a wide margin for the fastest median 5G download speed in Germany at 195.38 Mbps during Q2 2022.

Latvia: Balticom had the fastest median fixed broadband download speed in Latvia at 198.90 Mbps and highest Consistency (91.7%) during Q2 2022. LMT had the fastest median mobile download speed in Latvia at 68.48 Mbps during Q2 2022 — a large increase from 50.70 Mbps during Q1 2022. Among Latvia’s most populous cities, Olaine achieved the fastest median fixed broadband download and upload speeds at 127.09 Mbps and 126.30 Mbps, respectively during Q2 2022.

Lithuania: Telia had the fastest median mobile download speed in Lithuania at 90.11 Mbps during Q2 2022, a modest increase from 77.77 Mbps during Q1 2022. Cgates again had the fastest median fixed broadband speed in Lithuania at 113.78 Mbps during Q2 2022.

Poland: UPC was the fastest fixed broadband provider in Poland, achieving a median download speed of 203.69 Mbps during Q2 2022. Mobile operator Plus had the fastest median 5G download speed in Poland at 171.14 Mbps during Q2 2022, a gain of roughly 4 Mbps over its speed in Q1 2022.

Argentina: Personal was Argentina’s fastest mobile operator with a median download speed of 27.22 Mbps during Q2 2022. Buenos Aires (24.30 Mbps) and Rosario (23.93 Mbps) led the way among Argentina’s most populous cities for fastest median mobile download speed.

Brazil: Speedtest Intelligence finds Claro was the fastest and most consistent mobile operator in Brazil during Q2 2022, achieving a median download speed of 31.93 Mbps and Consistency of 84.2%.

Canada: Shaw was again Canada’s fastest fixed broadband provider, clocking a median download speed of 209.44 Mbps during Q2 2022. TELUS took the top spot as the fastest mobile operator in Canada, achieving a median download speed of 79.09 Mbps during Q2 2022. Competition for the fastest 5G in Canada was tight during Q2 2022 with no statistical winner, but Bell (139.75 Mbps) and TELUS (137.17 Mbps) led the way, with Rogers trailing at 93.06 Mbps.

Chile: Among popular device manufacturers in Chile during Q2 2022, Apple devices were the fastest, with a median download speed of 34.59 Mbps.

Colombia: Apple devices had the fastest median download speed among major device manufacturers in Colombia at 16.62 Mbps during Q2 2022.

Ecuador: According to Speedtest Intelligence, Netlife was Ecuador’s fastest and most consistent fixed broadband provider during Q2 2022, achieving a median download speed of 58.22 Mbps and Consistency of 77.2%, both of which marked increases over Q1 2022. CNT was the fastest and most consistent mobile operator in Ecuador during Q2 2022, with a median download speed of 33.32 Mbps and Consistency of 86.3%.

Guatemala: According to Speedtest Intelligence, Claro was the fastest and most consistent mobile operator in Guatemala during Q2 2022, achieving a median download speed of 20.05 Mbps and Consistency of 78.4%. Tigo was the fastest and most consistent fixed broadband provider in Guatemala, with a median download speed of 27.51 Mbps and Consistency of 58.4% during Q2 2022.

Mexico: Telcel was Mexico’s fastest mobile operator during Q2 2022, leading the market with a median download speed of 33.24 Mbps. Totalplay was the fastest and most consistent fixed broadband provider in Mexico, achieving a median download speed of 60.55 Mbps and Consistency of 78.2% during Q2 2022, both moderate increases over Q1 2022.

Peru: According to Speedtest Intelligence, Winet Telecom was Peru’s fastest fixed broadband provider by a wide margin, achieving a median download speed of 106.90 Mbps during Q2 2022. Claro was the fastest mobile operator in Peru during Q2 2022, delivering a median download speed of 21.52 Mbps.

United States: Speedtest Intelligence reveals Cox claimed the fastest fixed broadband download speed among top providers in the United States during Q2 2022, achieving a median download speed of 196.73 Mbps. T-Mobile took the top spot as the fastest and most consistent mobile operator in the U.S. during Q2 2022, achieving a median download speed of 116.54 Mbps and Consistency of 85.7%. Looking at tests taken only on 5G, T-Mobile achieved the fastest median 5G download speed at 187.33 Mbps during Q2 2022. The Samsung Galaxy S22 Ultra was the fastest popular device in the U.S. at 105.26 Mbps during Q2 2022.

Read the full market analyses and follow monthly ranking updates on the Speedtest Global IndexTM

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

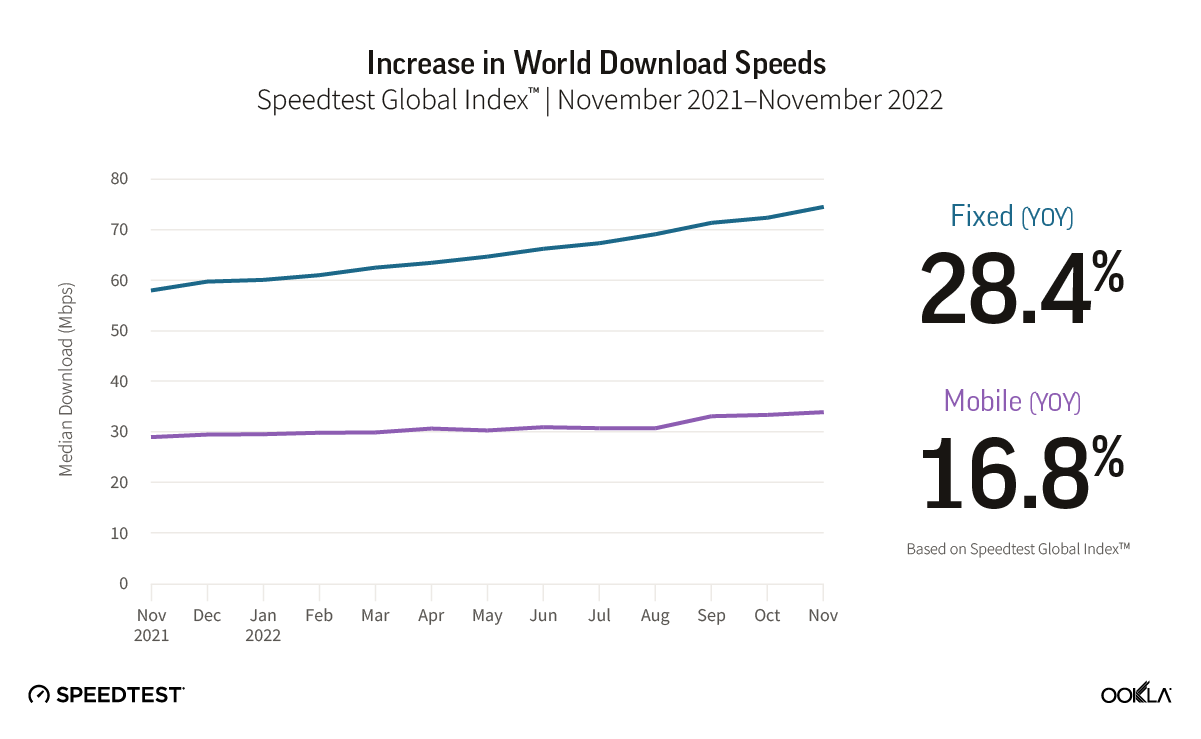

Internet connectivity continues to speed ahead for people around the world, especially as countries prioritize and improve mobile and fixed broadband networks. That’s nowhere more apparent than on the Speedtest Global Index™, which tracks countries’ internet speeds and the overall global median internet speeds. Last year, we took a look at the state of the internet speeds over the years, and today we’re back to see how most of 2022 fared from November 2021 to November 2022, and what countries made our top 10 fastest mobile and fixed broadband lists.

Mobile download speed jumped nearly 17% over the last year globally, fixed broadband up at least 28%

The improvement of global median download speeds has been somewhat asymmetrical over the past year on the Speedtest Global Index. Fixed broadband speeds made greater strides over the past year than mobile download speeds, with fixed broadband speeds becoming at least 28% faster and mobile becoming nearly 17% faster from November 2021 to November 2022. Gains in upload speed were even more pronounced with mobile becoming at least 9% faster and fixed broadband becoming at least 30% faster. Latency, which is becoming an increasingly important metric, decreased on mobile over the course of the year from 29 ms in 2021 to 28 ms in 2022, while fixed broadband latency remained the same at 10 ms.

Top 10 rankings remain relatively constant over the past year, U.A.E. joins fixed broadband list and Denmark, Macau (SAR), and Brunei race ahead for mobile during 2022

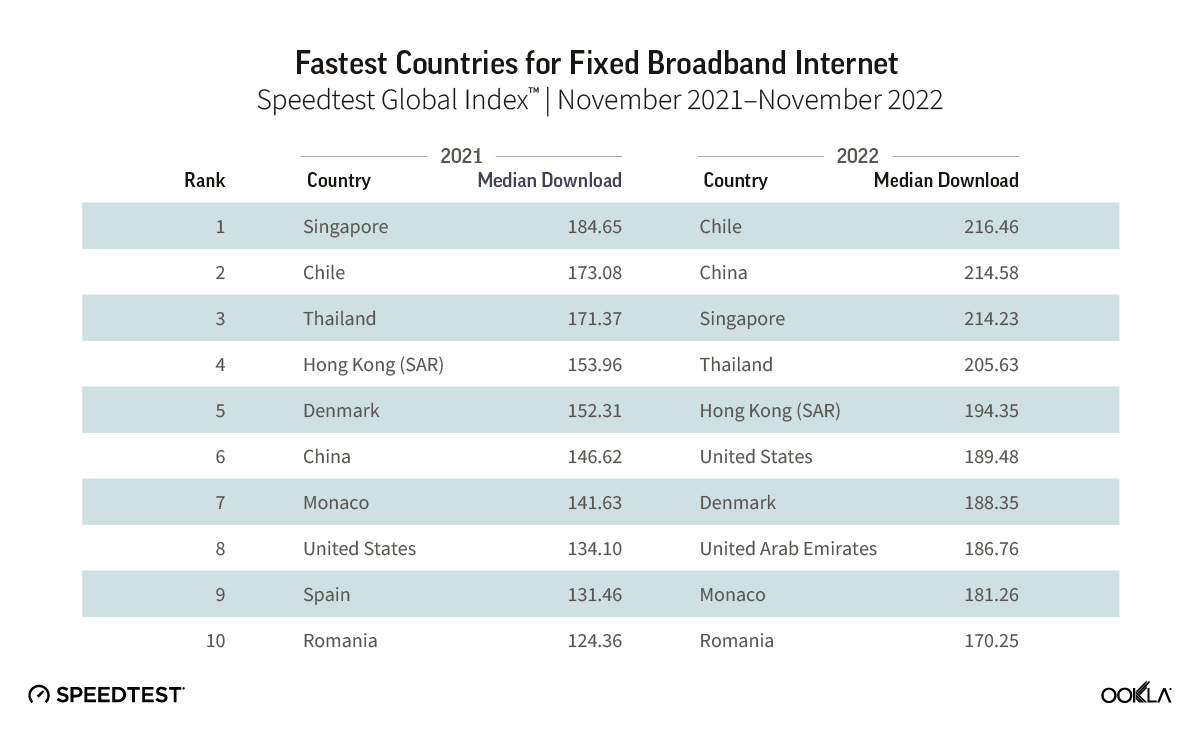

Chile raced ahead on fixed broadband

The competition for the fastest fixed broadband was neck-and-neck on the Speedtest Global Index during 2022, with Chile (216.23 Mbps) taking top honors and China (214.23 Mbps) and Singapore (214.23 Mbps) a hair behind. Over the course of the year, the top 10 countries for fastest fixed broadband remained relatively the same while each country jostled up and down the list for fixed broadband superiority. Only Spain was replaced from the top 10 with the U.A.E. taking its place. Notably, China jumped four places from sixth to second, improving its median download speed from 146.62 Mbps in 2021 to 214.58 Mbps in 2022. Romania’s tenth place finish in 2022 would have earned fourth place in 2021, showing how fast these countries are all prioritizing improved fixed broadband speeds.

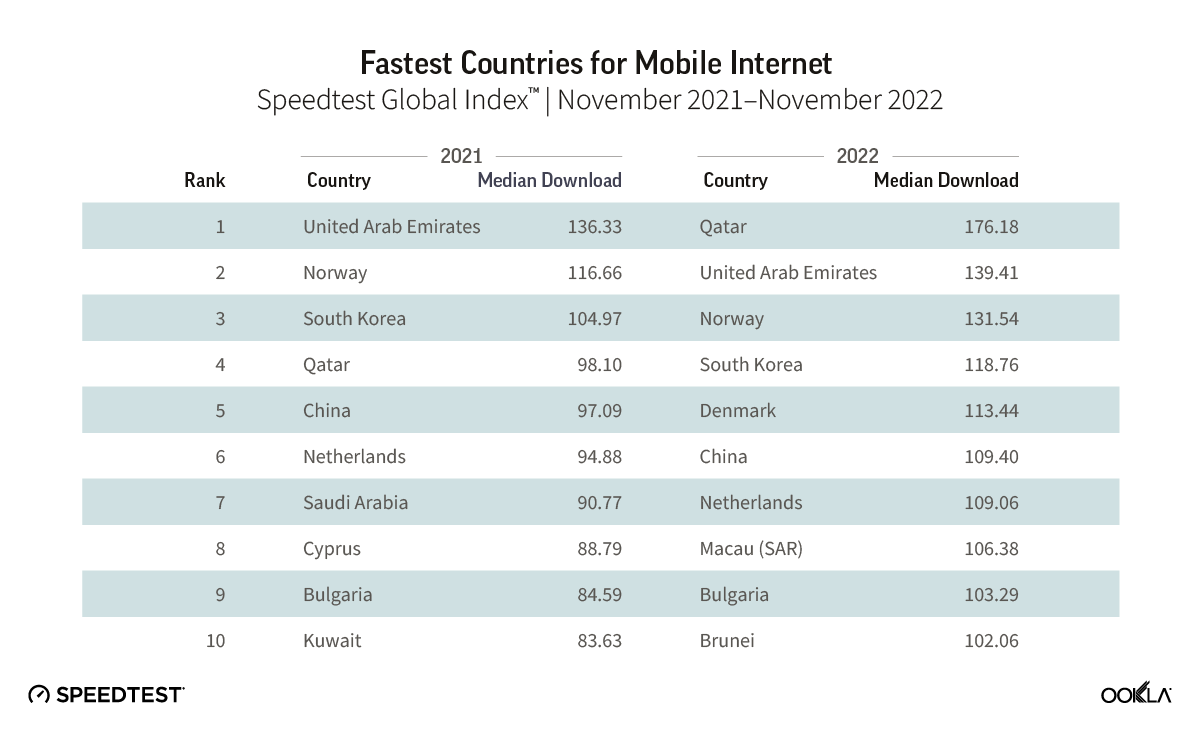

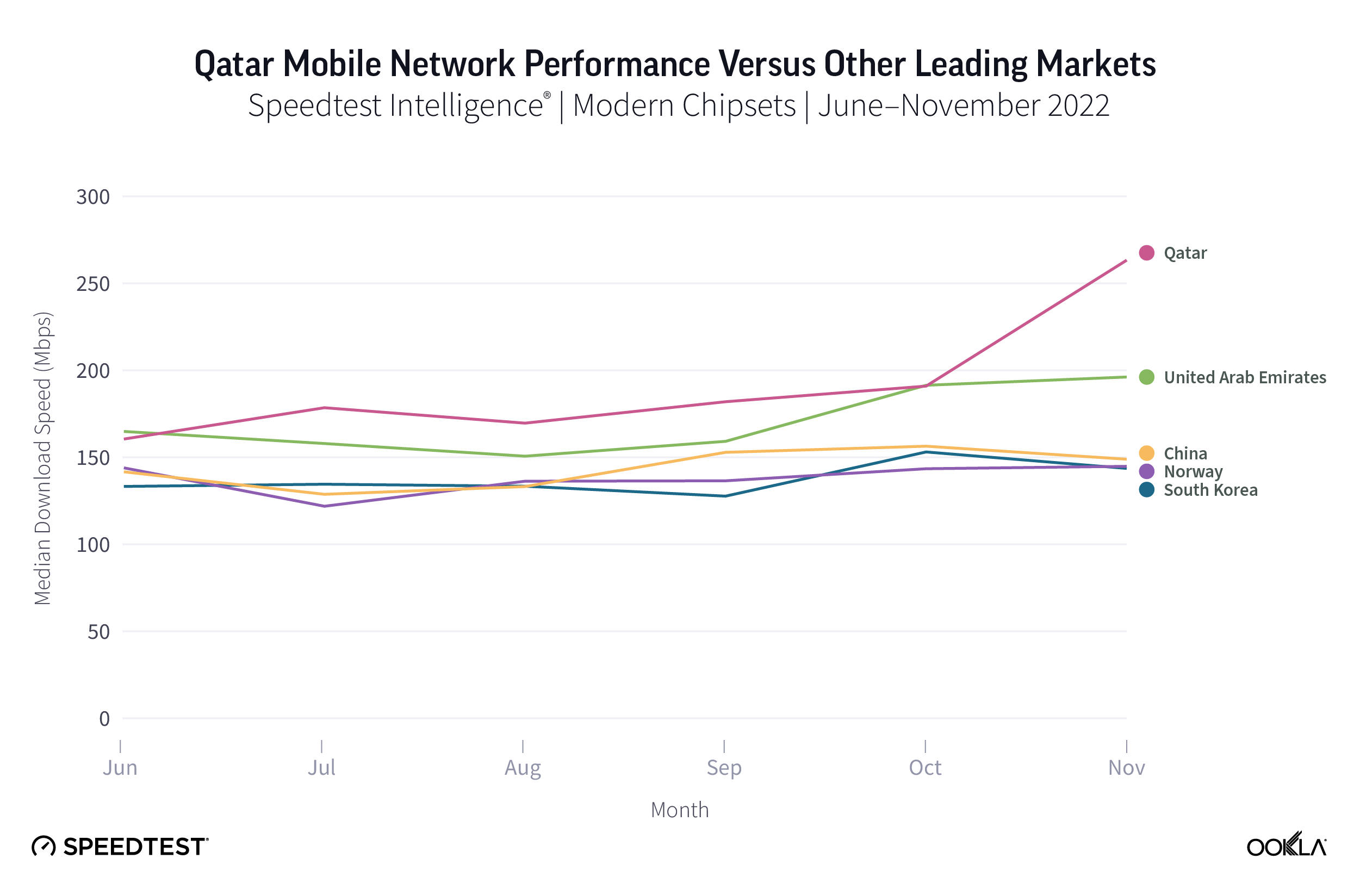

Qatar soars to first for fastest mobile country

Ahead of hosting the FIFA World Cup 2022®, Qatar rocketed to first place on the Speedtest Global Index with a median download speed of 176.18 Mbps in November 2022 from 98.10 Mbps in November 2022. Next on the list was the U.A.E. at 139.41 Mbps, which had the fastest median download speed in November 2021. Notably, all 10 countries on our November 2022 list had median mobile download speeds greater than 100 Mbps. New to our 2022 list Denmark (113.44 Mbps), Macau (SAR) (106.38 Mbps), and Brunei (102.36 Mbps) replaced Saudi Arabia, Cyprus, and Kuwait from our 2021 list.

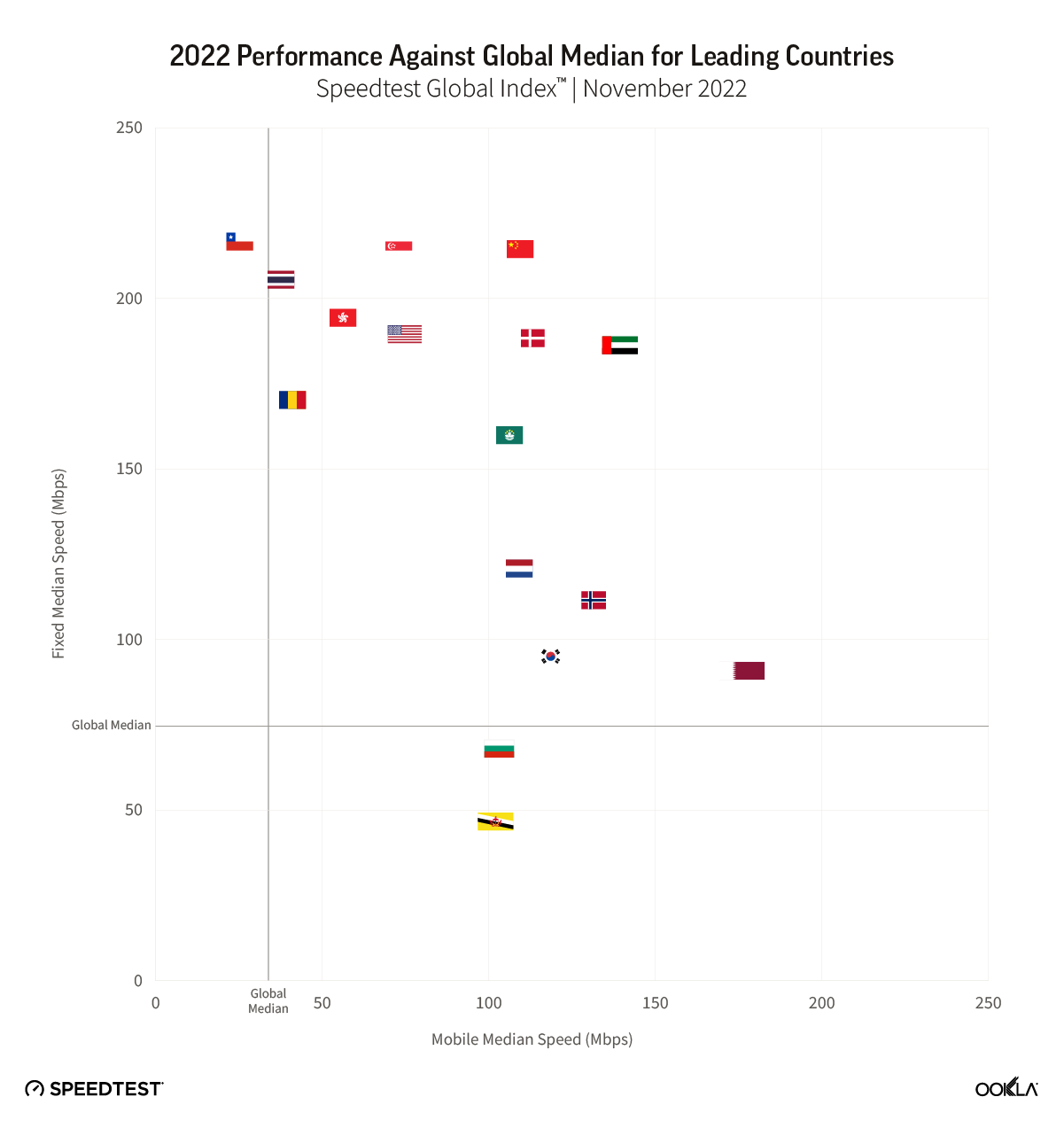

Most of the top 10 countries perform well for fixed and mobile

Out of the 17 countries appearing on either the fastest fixed broadband or mobile Speedtest Global Index top 10s during November 2021 — with China, Denmark, and the U.A.E. appearing on both lists — all but Monaco met the statistical threshold to be included to look at overall fixed and mobile performance. Looking at the remaining 16 countries, most every country on both lists performed relatively well against the global median for both fixed and mobile, which appear as gray lines in the image above. Three countries underperformed a global median: Brunei and Bulgaria for fixed, and Chile for mobile. Thailand performed at about roughly the global median for mobile, as did Romania.

We’re excited to see how global speeds and rankings change over the next year as individual countries and their providers choose to invest and expand different technologies, particularly in 5G and fiber. Be sure to track your country’s and check in on our monthly updates on the Speedtest Global Index. If you want more in-depth analyses and updates, subscribe to Ookla Research™.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

Malaysia launched its nationwide 5G network less than two years ago, adopting a distinctive 5G deployment approach. Ookla® data shows that the country’s 5G performance has been impressive, ranking as one of the top performers globally. In this article, we will compare Malaysia’s 5G performance with 5G in select countries, and we will also look at Malaysia’s 5G utilization based on the devices running Ookla Speedtest®.

Key takeaways

Malaysia continues to improve its Speedtest Global Index ranking. Malaysia’s overall mobile speed performance has steadily increased since the introduction of 5G at the end of 2021. In September 2023, the country’s median download speed was 61.50 Mbps, 2.9 times faster than its pre-5G speeds in September 2021. This led to a 45-place climb on the Speedtest Global Index™, from 86th place in September 2021 to 41st place in September 2023 after 5G had been deployed in Malaysia.

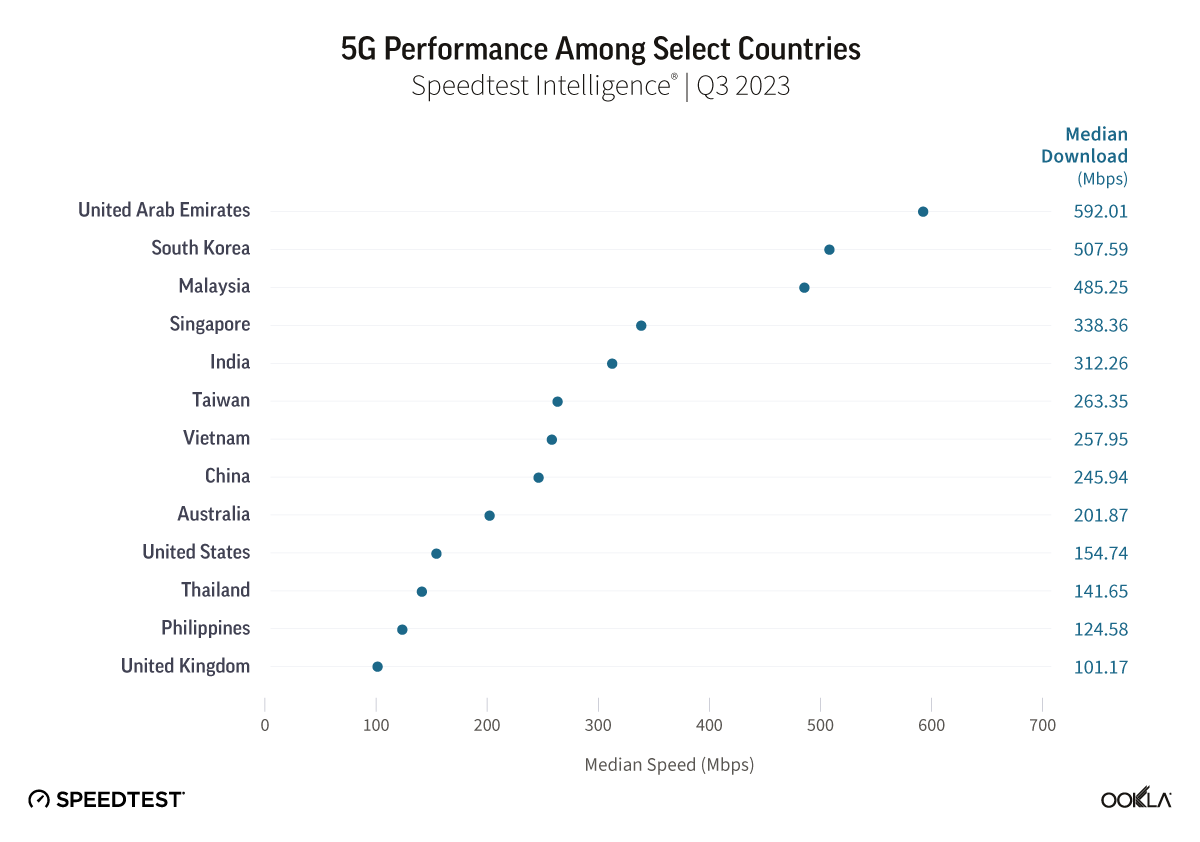

Malaysia is one of the top performing 5G markets globally. Malaysia ranks third globally for 5G download speed, with a reported speed of 485.25 Mbps, according to Speedtest Intelligence® data for Q3 2023. This puts Malaysia not only ahead of its Southeast Asian neighbors but also some developed markets, including the United Kingdom, Japan, and Germany.

A proportion of 5G-capable devices have yet to utilize the 5G network. Over 55% of all nationwide tests were conducted on 5G-capable devices in Q3 2023. However, only 25.1% of those tests were conducted on a 5G network. Operators with a lower subscriber base in the country reported a better percentage of Speedtests conducted on Malaysia’s 5G network.

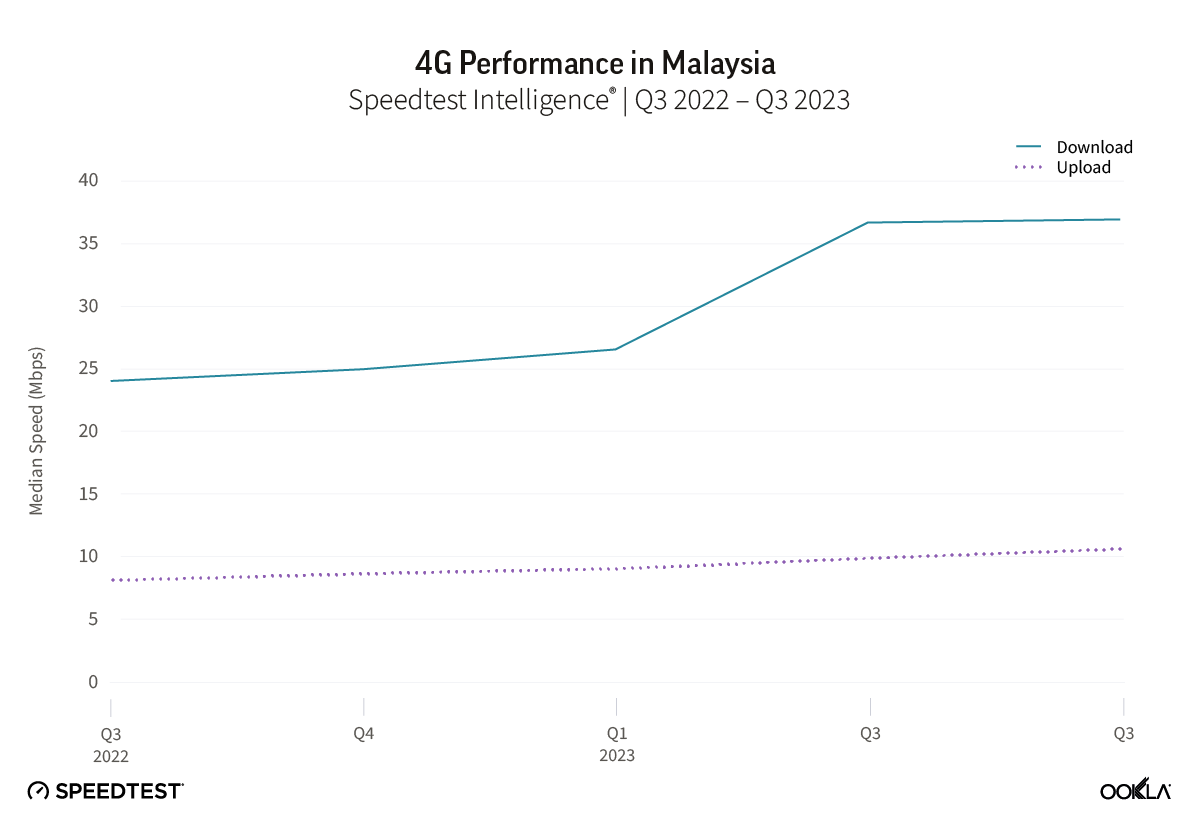

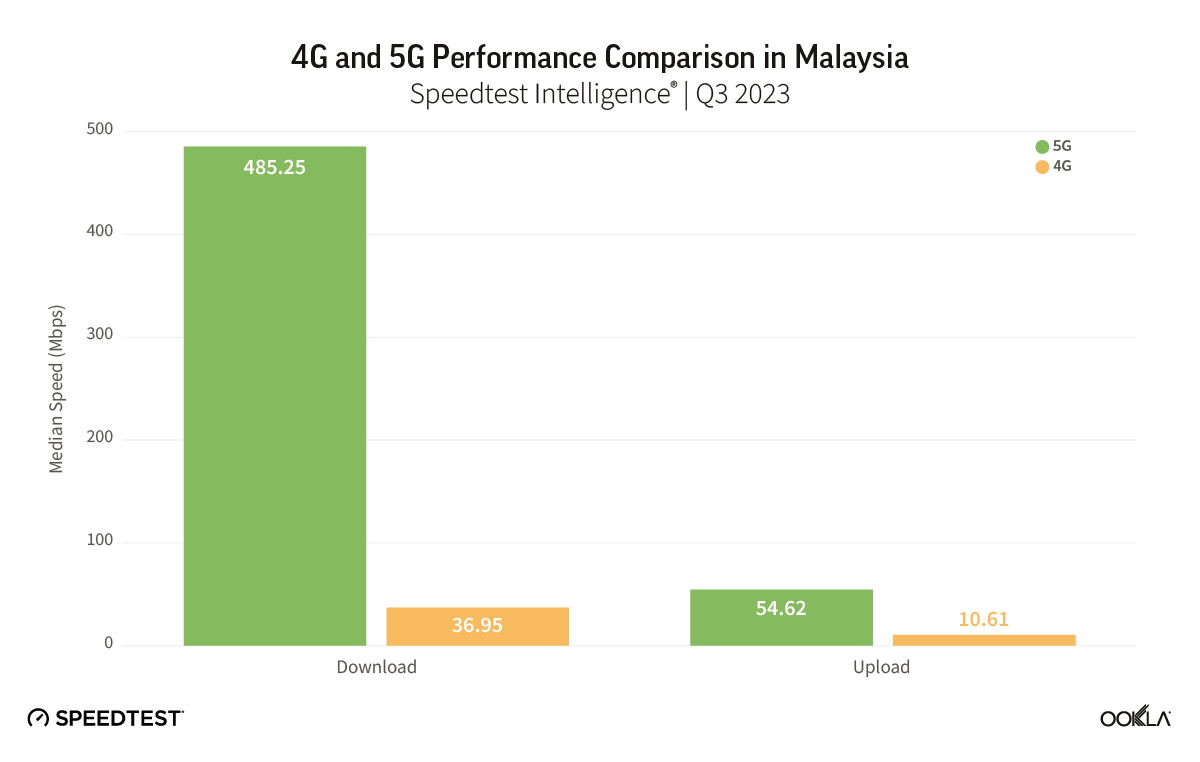

4G LTE performance sees continued improvement alongside 5G rollout. Median download speeds on 4G have increased from 24.04 Mbps to 36.95 Mbps from Q3 2022 to Q3 2023. 5G network offers much stronger performance than 4G, with 5G providing thirteen times faster download speeds and five times faster upload speeds than 4G.

Unique deployment strategy utilizing a Single Wholesale Network

In 2021, the government of Malaysia established Digital Nasional Berhad (DNB), responsible for rolling out a nationwide single wholesale network (SWN) to deliver 5G coverage. According to DNB, the 5G SWN model aimed to centralize infrastructure rollout, promoting efficient resource use, cost savings, and equitable 5G access across urban and rural landscapes.

The Malaysian Communications and Multimedia Commission (MCMC) assigned 5G spectrum to DNB in the 700 MHz, 3.5 GHz, and 26-28 GHz bands. DNB is currently utilizing 3.5 GHz spectrum across selected deployment areas. As discussed in our recent spectrum analysis, the upper mid-band (otherwise known as C-band) offers the best of both worlds in terms of coverage and capacity, which is important for DNB as they aim to reach 80% of populated areas by 2024. As of the end of September 2023, DNB has achieved 70.2% coverage of populated areas (COPA), with more than 5,800 sites deployed.

Yes was the first operator to enter into the Access Agreement with DNB and launch 5G services in Malaysia in Q4 2021. Following Yes, other operators such as Celcom, Digi, Unifi (Telekom Malaysia), and U Mobile launched their 5G services in early November 2022. In August 2023, Maxis became the latest operator to launch 5G services in Malaysia.

5G helped Malaysia climb 45 places in Speedtest’s mobile rankings

Ookla’s Speedtest Intelligence® data reveals that Malaysia has experienced a noteworthy increase in mobile median download speeds for all technologies since the launch of Malaysia’s first 5G network. In September 2023, Malaysia’s median mobile download speed increased to 61.50 Mbps, 2.9 times faster than the country’s 21.27 Mbps median download speed recorded in September 2021, before the launch of 5G in the country. As a result, Malaysia has improved its position on the Speedtest Global Index™, climbing 45 places from 86th in September 2021 to 41st in September 2023. This development places Malaysia ahead of some of its Southeast Asia neighboring countries, such as Indonesia, Thailand, Philippines, and Vietnam, as well as some developed markets, including the United Kingdom, Japan, and Germany.

Malaysia leads on 5G performance in Southeast Asia

In our recent report discussing 5G in the Asia Pacific region, we discussed how the region is on track to become the largest 5G market globally, with some markets in the region outpacing major European markets in terms of 5G performance. Comparing global 5G performance, Malaysia has emerged as one of the top performers in 5G connectivity. According to Speedtest Intelligence data in Q3 2023, Malaysia ranked third globally for 5G download speed, with a reported speed of 485.25 Mbps. This puts Malaysia ahead of its Southeast Asian neighbors, such as Singapore (338.36 Mbps), Thailand (141.65 Mbps), and the Philippines (124.58 Mbps).

4G performance continues to see improvements in the 5G era

5G rollout has also propelled an increase in 4G LTE speeds thanks to the modernization of the underlying infrastructure. Improvements in 4G LTE speeds are also partly from offloading 4G traffic to the 5G network, reducing 4G network congestion.

Speedtest Intelligence data shows that, at a country level, the median download speeds for 4G between Q3 2022 and Q3 2023 have increased from 24.04 Mbps to 36.95 Mbps. Upload speeds on 4G also continued to improve over the same period, albeit slightly.

As part of the 12th Malaysia Plan (2021–2025), the government is implementing the Jalinan Digital Negara (Jendela) initiative to address the need and demand for better quality fixed and mobile broadband coverage. Operators across Malaysia continue to roll out 4G to adhere to Jendela rollout targets. According to Jendela’s Phase 1 concluding report, 4G Coverage in Populated Areas achieved its target of providing 96.9% coverage by the end of 2022.

While current 4G network performance may meet the needs of most users for everyday tasks, such as browsing, streaming, and online communication, it is still far from the uplift in performance offered by 5G.

When we compare 5G and 4G performance in Malaysia for Q3 2023, Ookla’s data show that the median 5G download speed (485.25 Mbps) was 13 times faster than that of 4G (36.95 Mbps), while the country’s median 5G upload speed (54.62 Mbps) was 5 times faster than that of 4G LTE (10.61 Mbps).

Customers residing in areas outside of urban areas or in lower-income states may be reluctant to adopt 5G technology, as it may lead to higher subscription and upfront costs compared to previous mobile technologies. To that end, convincing consumers of the transformative advantages offered by 5G becomes pivotal in this context.

Potential to increase the adoption and usage of 5G technology

Apart from looking at the 5G performance in Malaysia, we also examined the percentage of devices utilizing the 5G network. This was done to gauge consumer uptake of 5G in the country. Using Speedtest Intelligence Q3 2023 data, we compared the proportion of unique devices that conducted consumer-initiated Speedtest using a 5G network to the total number of devices running Speedtest, regardless of network technology.

According to our analysis, in Q3 2023, out of all the mobile tests initiated by consumers in Malaysia across all technologies, 30.1% of them were carried out on the 5G network. This suggests that the adoption and usage of 5G technology among the general population in Malaysia still needs to improve. Although Malaysia launched its 5G network later than most neighboring countries in the region, its percentage of 5G users, while lower, is still noteworthy. In comparison, early 5G adopters such as Thailand and Taiwan, which launched their 5G network almost two years ahead of Malaysia, have a slightly higher percentage of devices connected to 5G, at less than 10 percentage points more.

Single wholesale network model levels the playing field

Unlike Malaysia’s previous 4G era, which followed a conventional approach to network rollout where individual operators owned the spectrum and were responsible for establishing their networks separately, Malaysia’s 5G SWN initiative takes a different approach from the traditional method adopted by most countries.

As stated by DNB, adopting the 5G SWN model can bring about several benefits, one of which is eliminating the duplication of infrastructure. Other advantages include ensuring uniform national coverage and encouraging operators to move towards a more service-oriented business model. While the long-term benefits remain to be seen, upon launch, operators with smaller 4G network footprints can immediately benefit from 5G coverage areas similar to those of larger and more established operators.

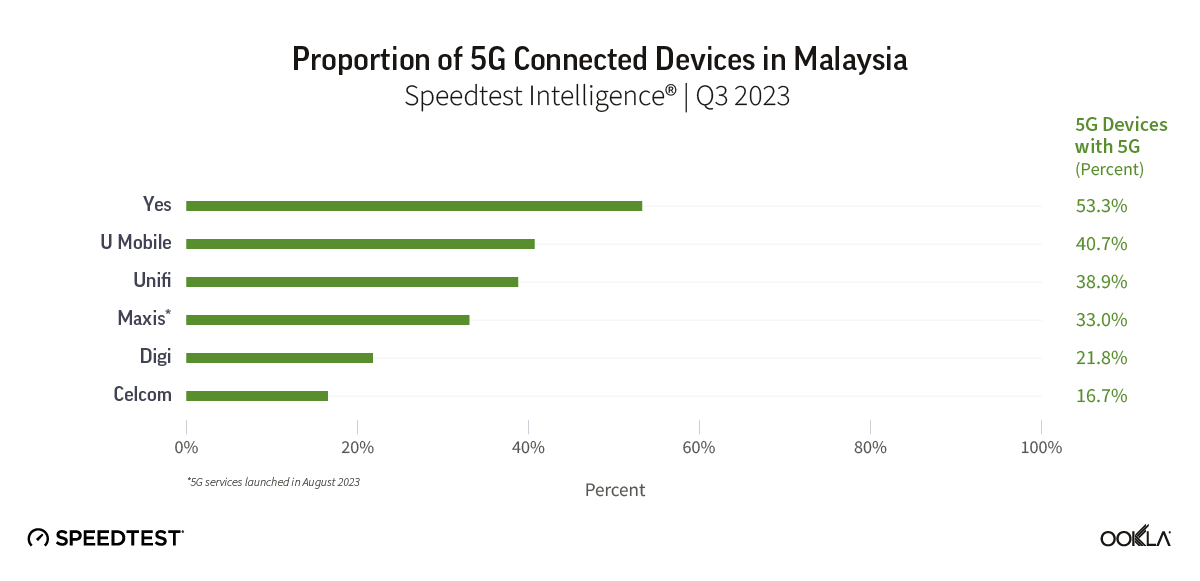

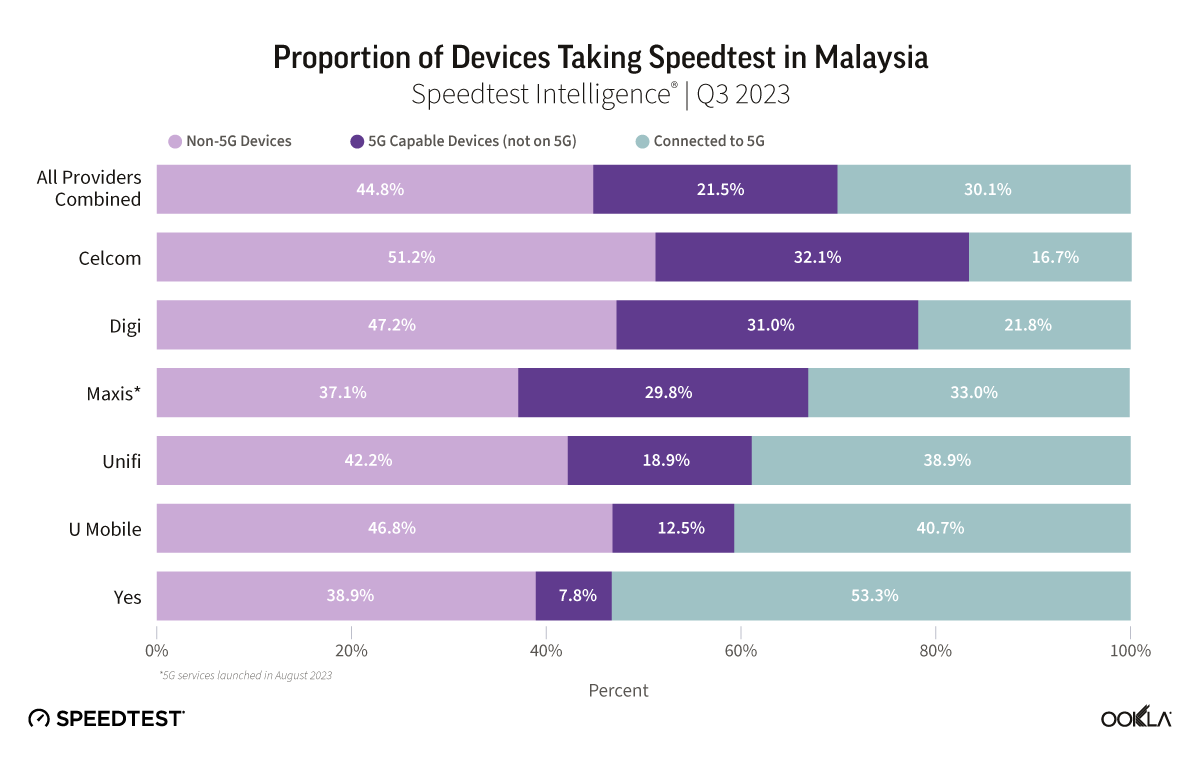

Ookla’s data shows that operators with smaller subscriber bases in the country reported a higher percentage of Speedtests performed on 5G-capable devices on the 5G network. Yes, the first operator to enter into an Access Agreement with DNB and the first to launch 5G in Malaysia in Q4 2021 reported the highest percentage at 53.3% in Q3 2023. U Mobile and Unifi, which launched their 5G networks in Q4 2022, reported 40.7% and 38.9% respectively.

Maxis, one of the larger mobile operators in Malaysia, had 33.0% of tests carried out on 5G. This is a notable uptake considering that Maxis only launched its 5G services in August 2023 after delays in its decision to enter into the Access Agreement with DNB. Both Celcom and Digi reported percentages below 22%.

One of the reasons for the variation in the number of 5G users is that the implementation of the 5G SWN model has enabled relatively smaller mobile players to offer more competitive plans, creating a more equitable playing field in the market. At the time of this report, Yes, U Mobile, and Unifi automatically included 5G services to their current and new customers. In contrast, Maxis, Digi, and Celcom, depending on which current plan their customers are on, imposed an additional surcharge between MYR 10 to MYR 20 (USD 2.20 to USD 4.40) per month for customers on lower-tiered plans to upgrade to a 5G plan.

Proportion of 5G-capable devices shows opportunities for better adoption

As DNB continues to expand its 5G network access to all populated areas across the country, motivating consumers to subscribe to the newer technology is critical. Operators already have a base of consumers who own 5G-capable devices, and we expect to see more consumers investing in 5G-capable devices going forward.

According to Speedtest Intelligence data, in Q3 2023, over 55% of all tests conducted in Malaysia were carried out on unique 5G-capable devices. Of these devices, 30.1% of the tests were conducted on 5G networks, while the remaining 21.5% were on non-5G networks.

Around 50% of Celcom’s and Digi’s customer bases own 5G-capable devices, but only 16.7% of Celcom’s and 21.6% of Digi’s customers conducted tests on 5G in Q3 2023. Maxis, which has the highest percentage of 5G-capable devices (62.8%), saw only 33% of its customers perform tests on 5G. For these operators, approximately 30% of their customer base that own 5G-capable devices have yet to initiate a Speedtest on the 5G network. There is an opportunity to transition these customers to adopt 5G as they likely have not yet subscribed or reside in areas without 5G coverage. Again, it is important to note that Maxis launched 5G services in August.

Unifi and U Mobile had 18.9% and 12.5%, respectively, of users that own 5G-capable devices yet to take advantage of the 5G network. On the other hand, Yes customers with 5G-capable devices are already benefiting from 5G, with less than 8% of them yet to subscribe to 5G or reside in areas without 5G coverage.

The government’s active participation is instrumental in achieving the national 5G connectivity agenda

Over the years, Malaysia has consistently invested in enhancing its digital infrastructure. With its National Fiberisation and Connectivity Plan (NFCP) and the MyDIGITAL initiative, it is already ahead of some of its neighbors in terms of connectivity. This groundwork creates a conducive environment for 5G and the readiness to embrace next-gen technology into its digital infrastructure.

Malaysia has adopted a distinctive strategy by implementing a single wholesale 5G model. DNB serves as a neutral party responsible for deploying 5G infrastructure and network across the country. By the end of 2022, the country has achieved its target of providing 40% coverage of populated areas. The performance of 5G technology has been impressive so far, making Malaysia one of the top performers globally. However, DNB has an obligation to expand its coverage to 80% of populated areas by 2024. 5G performance is also expected to decrease over time as network traffic grows and more and more users switch to 5Gs.

A few pieces of the puzzle still need to fall into place before 5G can be widely adopted in Malaysia. Apart from encouraging users with 5G-capable devices to adopt 5G services, around 45% of tests were carried out on non-5G devices, leaving a significant portion of users in the country still reliant on 4G. To further encourage the adoption of 5G, The Communications and Digital Ministry recently kicked off the 5G Rahmah initiative, where participating operators will now offer more affordable 5G data and device bundle plans to Malaysians, with additional incentives for low-income groups and civil servants.

It is evident that the government and regulatory authorities have a vital role in making 5G accessible to consumers. Now that all operators have agreed to provide 5G services, they also have the responsibility to keep the service’s cost affordable and educate consumers about its benefits. Earlier this year, the Malaysian government announced its plan to transition to a dual network model once the current rollout under DNB has reached the targeted 80% coverage of populated areas. However, the impact of this transition and factors such as the speed of the rollout, 5G adoption, and infrastructure management by operators remains to be determined and requires further assessment.

We will keep a close eye on the progress and effectiveness of 5G implementation in Malaysia. If you are interested in benchmarking your performance or if you’d like to learn more about internet speeds and performance in other markets around the world, visit the Speedtest Global IndexTM.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

Affandy Johan is the Industry Analyst at Ookla Research. He utilizes Ookla's data to develop insightful analyses covering various factors and aspects impacting the market. Affandy has extensive experience in the telecom industry, having worked for major vendors and operators in the Asia Pacific region.

Speedtest Global Index™ Market Analyses from Ookla® identify key data about internet performance in countries across the world. This quarter we’ve provided updated analyses for 44 markets that include details on fastest mobile and fixed broadband providers, performance of most popular devices and chipsets and internet speeds in cities. Click a country on the list below to see highlights or scroll through the article to learn what Speedtest Intelligence® revealed in all 43 markets:

Speedtest Intelligence revealed mobile provider MTN had the fastest median download speed (15.71 Mbps) and Consistency Score™ (71.1%) in Côte d’Ivoire during Q1 2022.

There was no statistical winner for fastest fixed broadband provider in Côte d’Ivoire during Q1 2022, though Orange had a median download speed of 33.65 Mbps and CANALBOX had a median download speed of 33.35 Mbps.

Fixed broadband provider ipNX had the fastest median download speed (21.34 Mbps) and highest Consistency Score (45.9%) in Nigeria during Q1 2022.

There was no statistical winner for fastest top mobile operator in Nigeria during Q1 2022, though Airtel and MTN led the way at 22.42 Mbps and 21.71 Mbps, respectively.

Speedtest Intelligence shows Cool Ideas had the fastest fixed broadband median download speed (46.05 Mbps) and highest Consistency Score (73.2%) in South Africa during Q1 2022.

MTN had the fastest median 5G download speed in South Africa at 213.37 Mbps during Q1 2022, much faster than Vodacom (132.11 Mbps).

The Samsung Galaxy S22 Ultra dominated for fastest popular device in South Africa during Q1 2022 and achieved a median download speed of 105.21 Mbps. The Apple iPhone 13 Pro Max followed at 82.23 Mbps.

Among top mobile operators in Tanzania, Halotel had the fastest median download speed (17.84 Mbps) and highest Consistency Score (80.1%) during Q1 2022.

Mwanza had the fastest median mobile download speed among Tanzania’s most populous cities at 13.76 Mbps during Q1 2022.

Speedtest Intelligence reveals mobile provider Turkcell had the fastest median download speed and highest Consistency Score in Turkey at 53.77 Mbps and 92.7%, respectively, during Q1 2022.

For fixed broadband in Turkey, TurkNet had the highest median download speed (47.43 Mbps) and Consistency Score (76.8%) during Q1 2022.

According to Speedtest Intelligence, China Telecom was the fastest fixed broadband provider in China with a median download speed of 146.70 Mbps during Q1 2022.

During Q1 2022, China Mobile achieved the fastest median 5G download speed at 300.96 Mbps, ahead of China Telecom (296.97 Mbps) and China Unicom (280.62 Mbps).

Among top device manufacturers, Huawei had the fastest median download speed in China at 108.94 Mbps during Q1 2022.

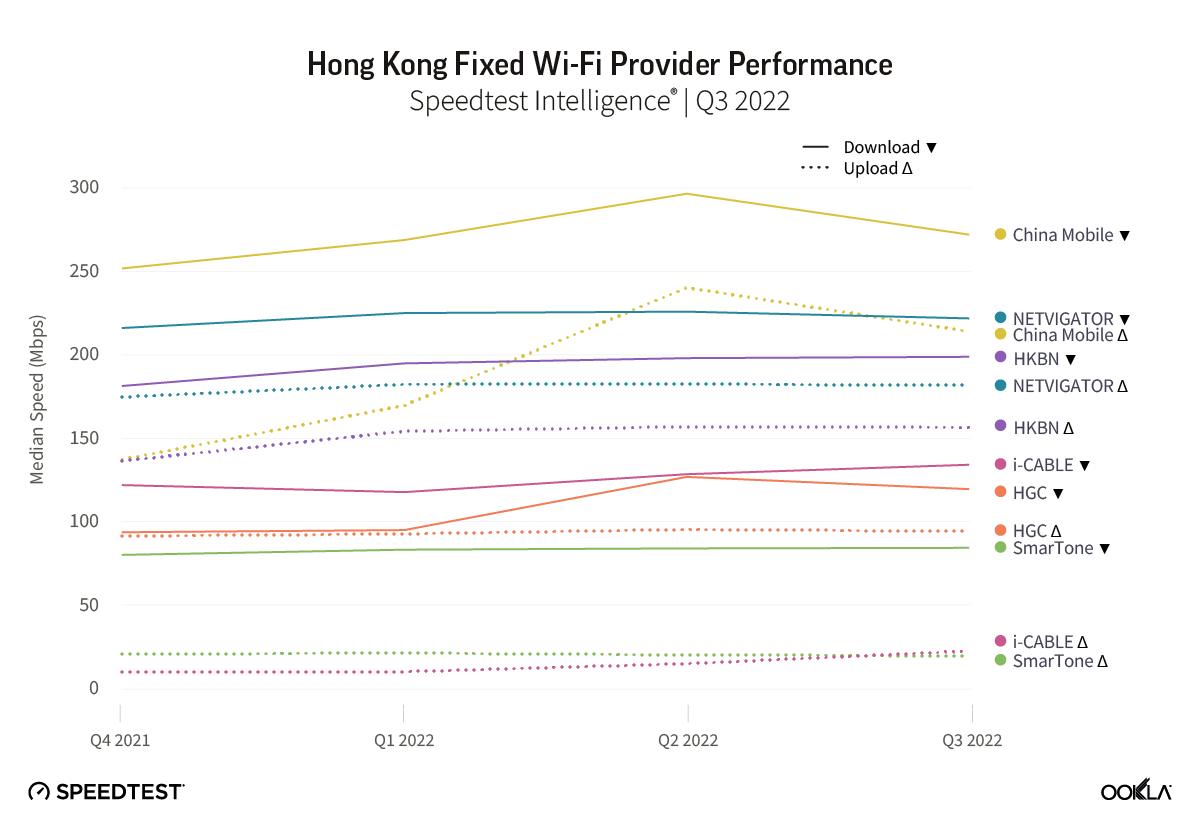

China Mobile Hong Kong was the fastest mobile operator in Hong Kong, achieving a median download speed of 66.11 Mbps during Q1 2022.

China Mobile Hong Kong also showed the fastest 5G download speed, achieving a median speed of 172.19 Mbps during Q1 2022. Mobile provider 3 followed at 155.81 Mbps.

Vodafone was the fastest mobile operator in New Zealand during Q1 2022, earning a median download speed of 59.65 Mbps.

2degrees blazed ahead with the fastest median 5G download speed in New Zealand at 479.71 Mbps during Q1 2022, beating out Vodafone (342.45 Mbps) and Spark (307.21 Mbps).

For fixed broadband, MyRepublic achieved the fastest median download speed in New Zealand at 217.66 Mbps during Q1 2022.

Speedtest Intelligence shows Singtel was the fastest top mobile operator in Singapore with a median download speed of 93.00 Mbps during Q1 2022.

Singtel blazed ahead of the competition for fastest median 5G download speed in Singapore at 360.31 Mbps during Q1 2022 — a strong rise over its median 5G download speed of 289.01 Mbps during Q4 2021.

Speedtest Intelligence revealed that AIS had the fastest median download speed on mobile in Thailand at 43.52 Mbps during Q1 2022, beating out TrueMove H and dtac.

AIS also had the fastest median 5G download speed in Thailand during Q1 2022 at 261.19 Mbps, followed by TrueMove H and dtac.

Vinaphone was Vietnam’s fastest mobile operator during Q1 2022, reaching a median mobile download speed of 42.43 Mbps, just faster than Viettel (40.61 Mbps).

Apple’s iPhone 13 Pro had the fastest median download speed among popular devices in Vietnam at 70.91 Mbps during Q1 2022.

Magenta took the top spot as Austria’s fastest fixed broadband provider with a median download speed of 154.44 Mbps during Q1 2022. LIWEST was the closest competitor (88.75 Mbps).

A1 was the fastest mobile provider in Austria during Q1 2022, achieving a median download speed of 69.80 Mbps. Operator 3 followed at 53.73 Mbps.

Telenet decisively claimed its spot as Belgium’s fastest fixed broadband provider during Q1 2022, earning a median download speed of 129.18 Mbps. VOO followed at 109.76 Mbps.

Among mobile operators, Telenet/BASE had the fastest median download speed at 66.92 Mbps.

Fastspeed was Denmark’s fastest fixed broadband provider during Q1 2022, achieving a median download speed of 284.28 Mbps. Hiper followed at 239.43 Mbps.

YouSee was Denmark’s fastest mobile operator, earning a median download speed of 115.87 Mbps during Q1 2022.

According to Speedtest Intelligence, Elisa was the fastest fixed broadband provider in Estonia during Q1 2022, achieving a median download speed of 74.48 Mbps.

Telia had the fastest mobile median download speed in Estonia at 73.20 Mbps during Q1 2022.

According to Speedtest Intelligence, DNA took the top spot as Finland’s fastest mobile operator in Q1 2022, earning a median download speed of 70.76 Mbps. DNA also edged out Telia for the highest Consistency Score 93.1% to 91.7%.

In addition, DNA had the fastest 5G download speed in Finland, achieving a median download speed of 297.70 Mbps. Telia (259.68 Mbps) and Elisa (230.35 Mbps) followed.

Competition was tight for Finland’s fastest fixed broadband provider during Q1 2022. DNA (87.87 Mbps) raced past Elisa (86.54 Mbps) and Telia (86.13 Mbps) to take the top spot.

Orange earned the top spot as France’s fastest and most consistent mobile operator with a median mobile download speed of 81.03 Mbps and a Consistency Score of 89.8% during Q1 2022.

During Q1 2022, Orange dominated the competition as France’s fastest 5G provider by achieving a median 5G download speed of 366.42 Mbps. SFR followed at 247.32 Mbps.

According to Speedtest Intelligence, Vodafone was Germany’s fastest fixed broadband provider during Q1 2022, earning a median download speed of 108.67 Mbps.

Telekom achieved the fastest median mobile download speed (79.34 Mbps) and Consistency Score (90.9%) among German mobile operators during Q1 2022.

Telekom took the top spot for the fastest median 5G download speed in Germany at 193.09 Mbps during Q1 2022.

Vodafone was Hungary’s fastest fixed broadband provider with a median download speed of 159.59 Mbps during Q1 2022. Vodafone also had the highest Consistency Score at 87.9% during Q1 2022.

Yettel was Hungary’s fastest mobile operator during Q1 2022, earning a median download speed of 50.62 Mbps.

According to Speedtest Intelligence, Balticom had the fastest median fixed broadband download speed in Latvia at 188.27 Mbps and highest Consistency Score (91.9%) during Q1 2022.

LMT had the fastest median mobile download speed in Latvia at 50.70 Mbps during Q1 2022.

Telia had the fastest median mobile download speed in Lithuania at 77.77 Mbps during Q1 2022. Tele2 followed at 41.75 Mbps, then BITE (29.81 Mbps).

Speedtest Intelligence reveals that Cgates had the fastest median fixed broadband speed in Lithuania at 99.50 Mbps during Q1 2022, edging out Penki (93.52 Mbps) and Telia (86.84 Mbps).

Melita took the top spot as Malta’s fastest and most consistent fixed broadband provider during Q1 2022, earning a median download speed of 117.68 Mbps and Consistency Score of 85.2%.

According to Speedtest Intelligence, Orange dominated as Moldova’s fastest fixed broadband provider, achieving a median download speed of 203.54 Mbps during Q1 2022.

Tiraspol showed the fastest median mobile download speed among Moldova’s most populous cities at 35.62 Mbps during Q1 2022.

Speedtest Intelligence revealed that UPC was the fastest fixed broadband provider in Poland, achieving a median download speed of 195.74 Mbps during Q1 2022.

Mobile operator Plus had the fastest median 5G download speed in Poland at 167.37 Mbps during Q1 2022, a slight gain over Q4 2021.

Orange took the top spot as Slovakia’s fastest mobile operator with a median download speed of 53.30 Mbps, edging out Telekom’s 45.90 Mbps during Q1 2022.

Orange also dominated as the fastest 5G operator in Slovakia with a median 5G download speed at 299.09 Mbps during Q1 2022. 4ka followed at 177.76 Mbps.

UPC took the top spot as Slovakia’s fastest and most consistent fixed broadband provider with a median download speed of 146.65 Mbps and a Consistency Score of 87.5% during Q1 2022.

Movistar provided the fastest and most consistent mobile experience among Spanish mobile operators during Q1 2022 with a median download speed of 52.44 Mbps and Consistency Score of 89.4%.

Vodafone was Spain’s fastest 5G provider by a wide margin, achieving a median download speed of 192.40 Mbps during Q1 2022.

Speedtest Intelligence revealed Personal was Argentina’s fastest mobile operator with a median download speed of 25.57 Mbps during Q1 2022.

There was a tight race for the fastest median mobile download speed in Argentina’s most populous cities with no statistical winner during Q1 2022. However, Buenos Aires (25.26 Mbps) and La Plata (25.18 Mbps) led the way.

Speedtest Intelligence reveals Claro was the fastest and most consistent mobile operator in Brazil during Q1 2022, achieving a median download speed of 33.53 Mbps and Consistency Score of 84.6%.

Claro achieved the fastest median 5G download speed in Brazil at 72.35 Mbps during Q1 2022. TIM (62.80 Mbps) and Vivo (62.38 Mbps) followed.

According to Speedtest Intelligence, Netlife was Ecuador’s fastest and most consistent fixed broadband provider during Q1 2022, achieving a median download speed of 45.53 Mbps and Consistency Score of 75.5%.

CNT was the fastest and most consistent mobile operator in Ecuador during Q1 2022, with a median download speed of 33.11 Mbps and Consistency Score of 87.4%.

According to Speedtest Intelligence, Claro was the fastest and most consistent mobile operator in Guatemala during Q1 2022, achieving a median download speed of 21.40 Mbps and Consistency Score of 80.5%.

Tigo was the fastest and most consistent fixed broadband provider in Guatemala with a median download speed of 26.56 Mbps and Consistency Score of 58.3% during Q1 2022.

Speedtest Intelligence reveals Telcel was Mexico’s fastest mobile operator during Q1 2022, leading the market with a median download speed of 40.25 Mbps.

Totalplay was the fastest and most consistent fixed broadband provider in Mexico, achieving a median download speed of 49.33 Mbps and Consistency Score of 74.3% during Q1 2022.

According to Speedtest Intelligence, Winet Telecom was Peru’s fastest fixed broadband provider by a wide margin, achieving a median download speed of 102.83 Mbps during Q1 2022.

Claro was the fastest mobile operator in Peru during Q1 2022, earning a median download speed of 19.55 Mbps.

Speedtest Intelligence reveals Verizon was the fastest fixed broadband provider in the United States during Q1 2022, edging out XFINITY with a median download speed of 184.36 Mbps to XFINITY’s 179.12 Mbps.

T-Mobile took the top spot as the fastest and most consistent mobile operator in the U.S. during Q1 2022, achieving a median download speed of 117.83 Mbps and a Consistency Score of 88.3% — both increases over Q4 2021.

Looking at tests taken only on 5G, T-Mobile achieved the fastest median 5G download speed at 191.12 Mbps during Q1 2022. Verizon also had a notable increase in 5G download speed during Q1 2022 over Q4 2021 , which was helped by turning on new C-Band spectrum in January.

The Samsung Galaxy S22 Ultra was the fastest popular device in the U.S. at 116.33 Mbps during Q1 2022.

Read the full market analyses and follow monthly ranking updates on the Speedtest Global Index.

Editor’s note: This article was updated on May 11, 2022.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

Ookla® is a global leader in connectivity intelligence that provides consumers, businesses, and other organizations with data-driven insights to improve networks and connected experiences.

Tower companies, DAS, neutral hosts, and other infrastructure providers are heavily investing in wireless assets to deliver expansive, uninterrupted connections with lightning-fast speeds to create a more connected world. While this presents wireless infrastructure providers with opportunities for major growth, they need the right data to make the most profitable investment decisions. This type of data includes network performance, user density, data usage, and other indicators to determine the best locations for investments or partnerships.

In the next Ookla® webinar, learn how wireless infrastructure providers can make smarter investments, more informed real estate decisions, and help improve network performance by using crowdsourced network intelligence to prioritize efforts.

Keep reading to learn how wireless infrastructure providers can use these insights, and sign up for the webinar on Wednesday, June 29, at 10 a.m. PDT (5 p.m. GMT), for a more in-depth discussion.

1. Make more informed wireless infrastructure planning decisions

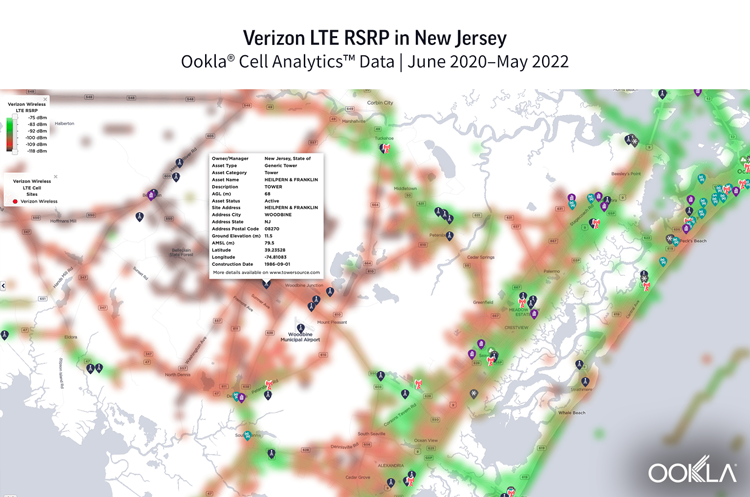

When wireless infrastructure providers are ready to invest in new assets, they need an accurate view into the availability of coverage and performance in a given area. An oversaturated, congested network may require different solutions than an underserved area.

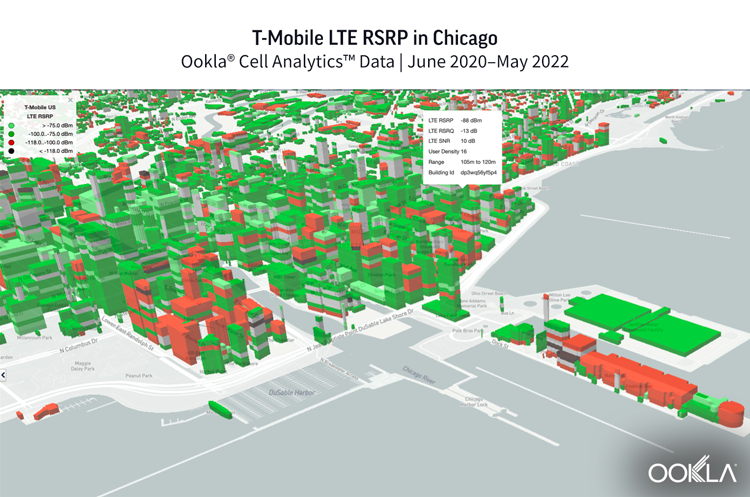

This map shows the location of a mobile network operator’s (MNO’s) towers and the corresponding signal strength on that network, allowing infrastructure providers to better understand where to approach the operator for new assets.

2. Better prioritize future deployments and investments

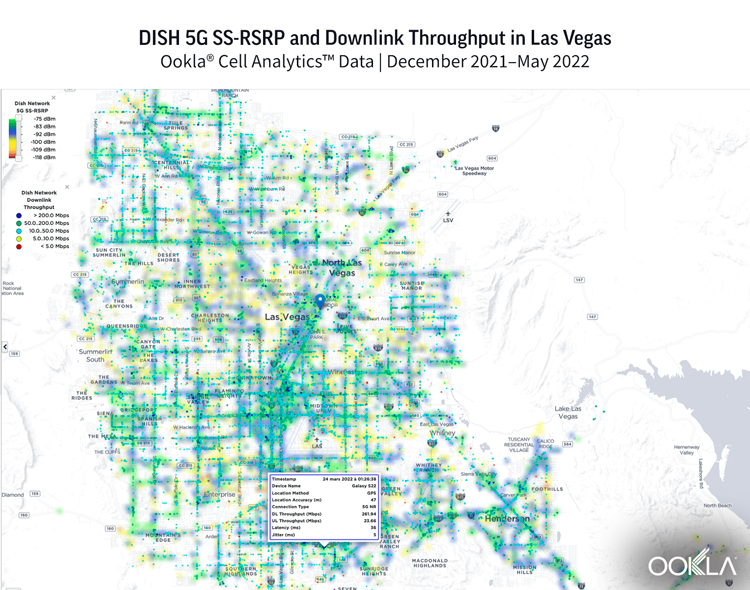

As MNOs prepare for 5G and other new network deployments, infrastructure providers can use crowdsourced data to determine spots of low coverage and performance in both urban and rural areas. This allows infrastructure providers to determine what areas need additional assets to improve connectivity to serve the population, and they can make those determinations based on usage.

As the operator deployed 5G in Las Vegas, infrastructure providers can use this information to put the right assets in place, such as adding DAS, to support a new network.

3. Benchmark the performance, quality, and availability of existing indoor and outdoor networks

Infrastructure providers can also use crowdsourced network intelligence to find potential co-location opportunities and compare operators to find new business opportunities. By analyzing KPIs for all operators in a given area, an infrastructure provider can determine which operators need to improve network coverage, performance, or quality in key locations.

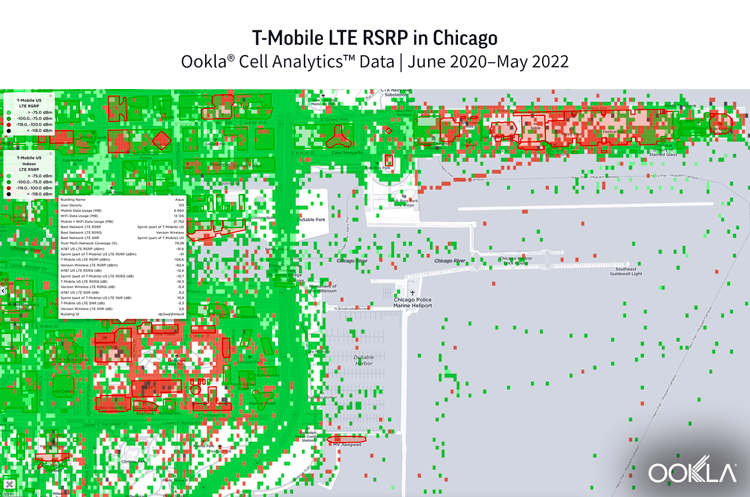

For example, the above image shows areas of poor signal strength for one operator in a city block in Chicago. Comparing this to other operators in the area, an infrastructure provider can identify new sales opportunities down to the individual building level.

4. Identify buildings and areas with high user concentration and data usage, as well as poor network quality, coverage, and performance

By pinpointing congested areas or buildings, wireless infrastructure providers can better plan where to add DAS and other equipment to help offset the network density.

This map shows infrastructure providers where new assets could help with network performance issues related to user density.

5. Drive a more efficient sales process with per-building intelligence

With accurate, detailed insights, the infrastructure provider can export data to pinpoint the exact issues building by building. The provider can then use that data to proactively determine the optimal locations for leasing roof or building space to build new equipment. They can even use that data to identify where operators should lease additional cell sites to improve coverage and performance, which gives them an advantage when starting those business development conversations.

With this data, infrastructure providers can look up the building name and see the individual operator’s performance, and then approach them with the right asset solution.

For more information on how to use crowdsourced data to improve your ROI, join us for the webinar on June 29 at 10 a.m. PDT. Even if you can’t attend at this time, you will receive a video recording after the live event. We look forward to sharing how wireless infrastructure providers are making better investment decisions and answering your questions.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

Ookla® is a global leader in connectivity intelligence that provides consumers, businesses, and other organizations with data-driven insights to improve networks and connected experiences.

5G is coming to Central Asia, begging the question: what is the current performance and availability of mobile networks? In this article, we will examine the state of mobile networks across five countries that comprise the Central Asian region: Kazakhstan, Kyrgyzstan, Tajikistan, Uzbekistan, and Turkmenistan. Central Asia is a region comprising upper-middle and low-income countries, rich in natural resources and sharing a common history. The countries within the region recognize that they have to enable good connectivity to ensure people and the economy can benefit from digital transformation.

Key takeaways

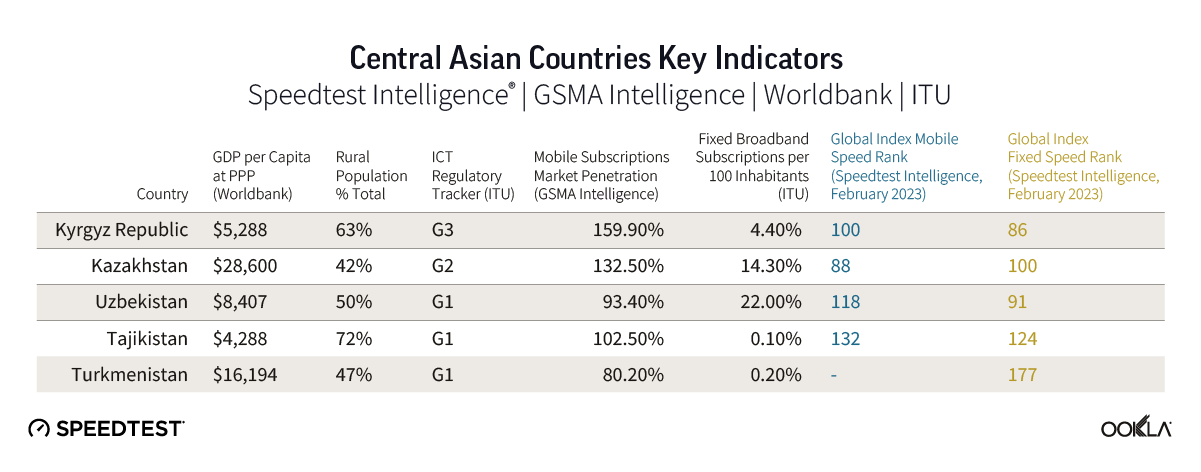

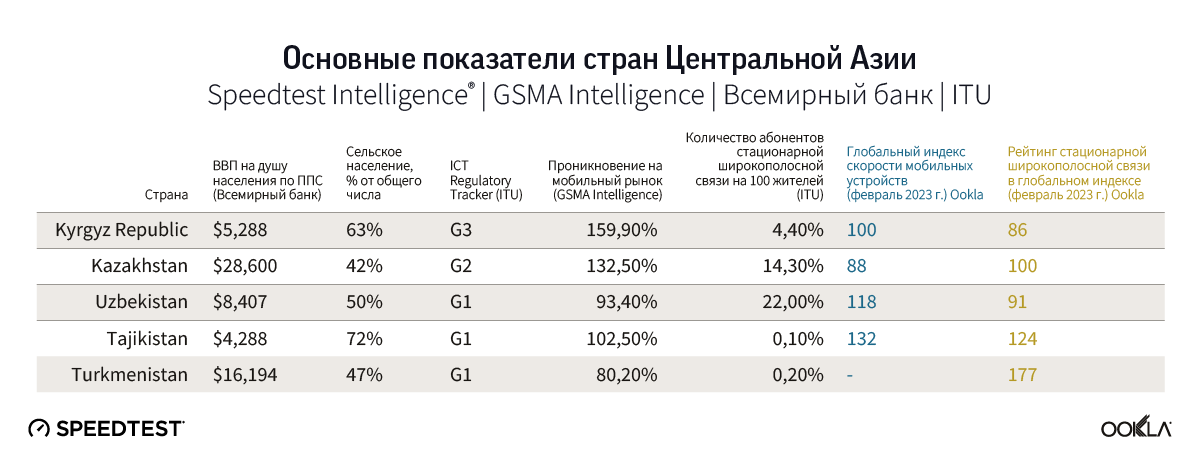

Need for more market reforms. The International Telecommunication Union ICT Regulatory Tracker puts three of the five countries: Tajikistan, Uzbekistan, and Turkmenistan, as regulated public monopolies (G1). Kazakhstan and Kyrgyzstan have more supportive regulatory environments, but none of the countries is fully transparent. According to the ICT, improved regulatory framework and performance correlate to increases in telecom investment, which positively affects coverage, price competitiveness, adoption levels, and GDP per capita.

Kazakhstan led on median download speeds. Kazakhstan topped the ranks in terms of mobile download speed, while Tele 2 Kazakhstan for median download speed across all Central Asia operators in Q4 2022.

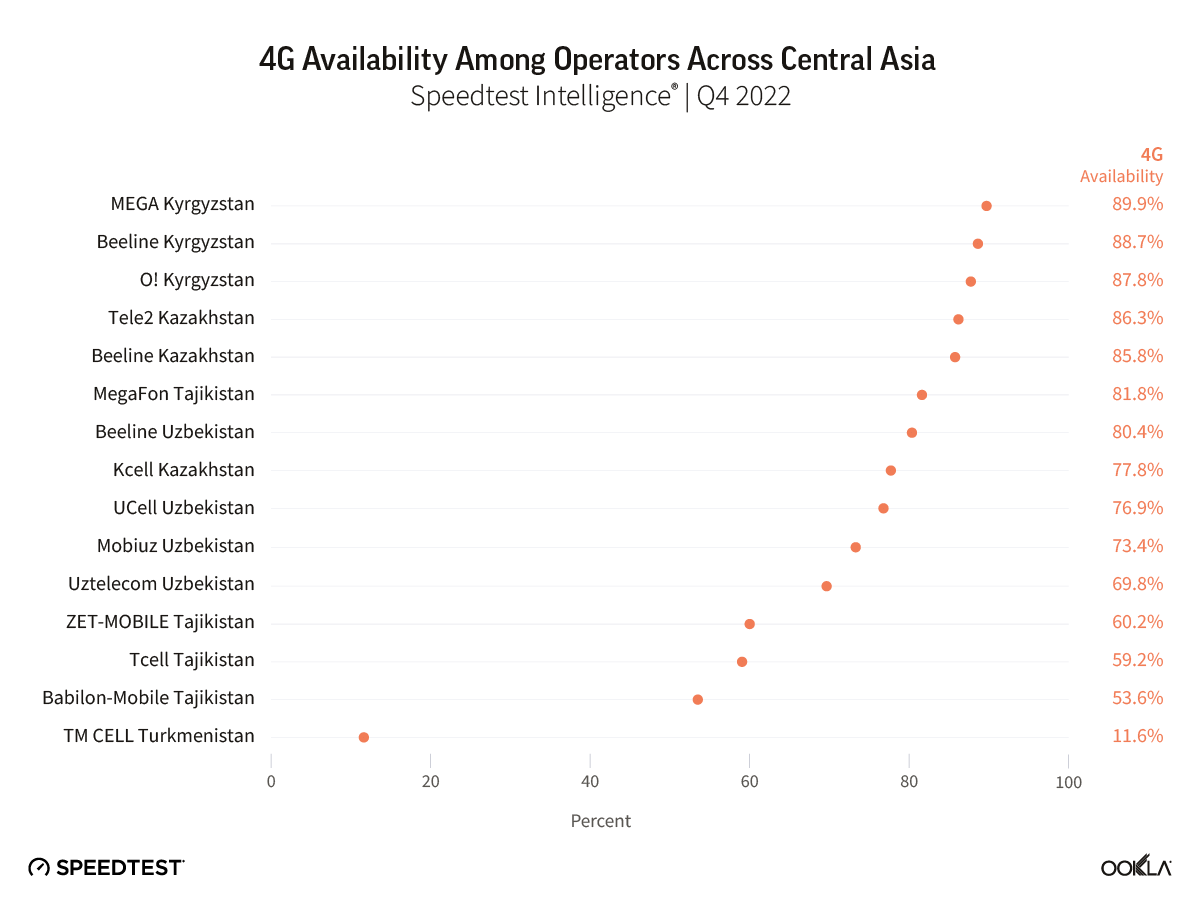

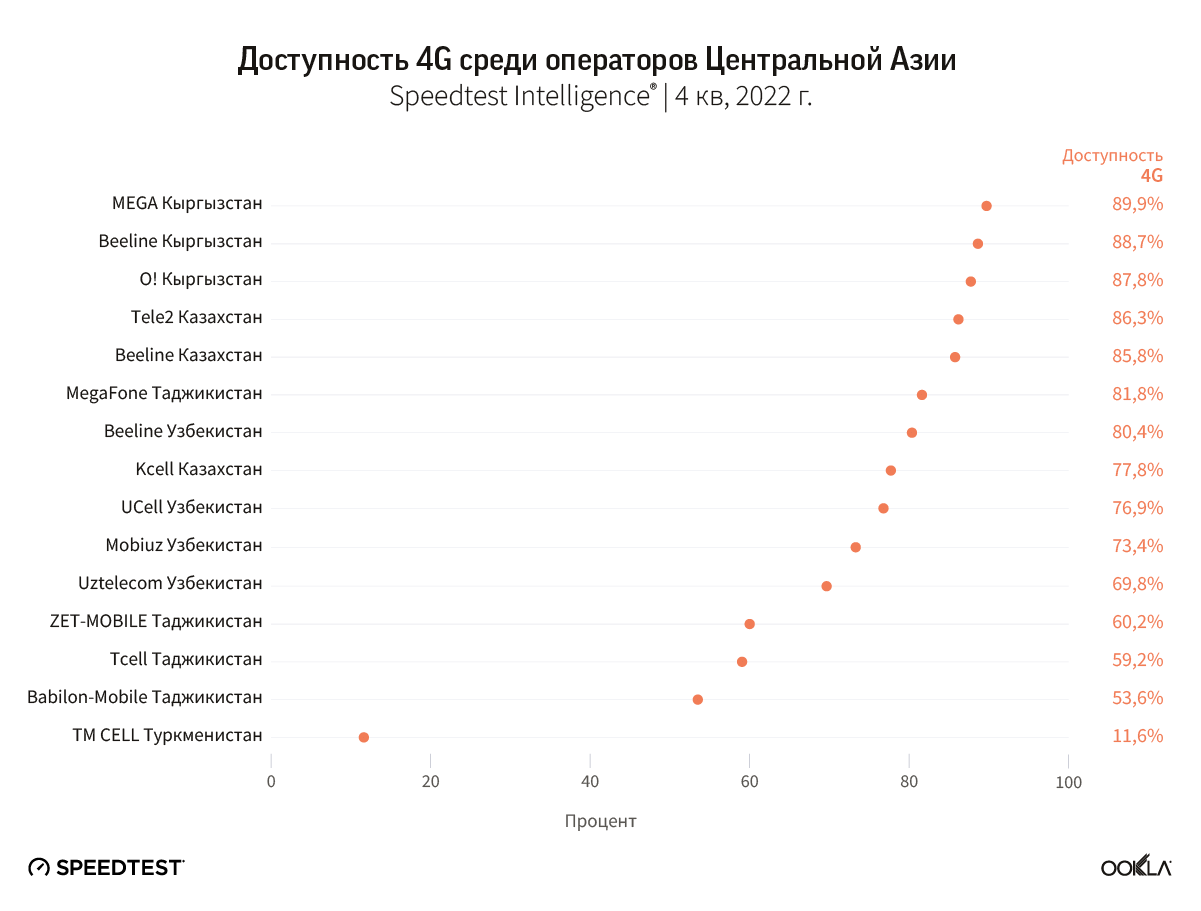

Kyrgyzstan performed well on 4G Availability. Thanks to the supportive regulatory environment, Kyrgyzstan punches above its weight in terms of mobile performance and 4G Availability compared to other, richer neighbors.

Banking on digital transformation. Apart from Turkmenistan, Central Asian countries have initiatives to stimulate mobile adoption and drive digital transformation. Uzbekistan and Kazakhstan, in particular, invest in digital infrastructure to stimulate all facets of the digital economy.

Kazakhstan and Kyrgyzstan shined the brightest for mobile across Central Asia

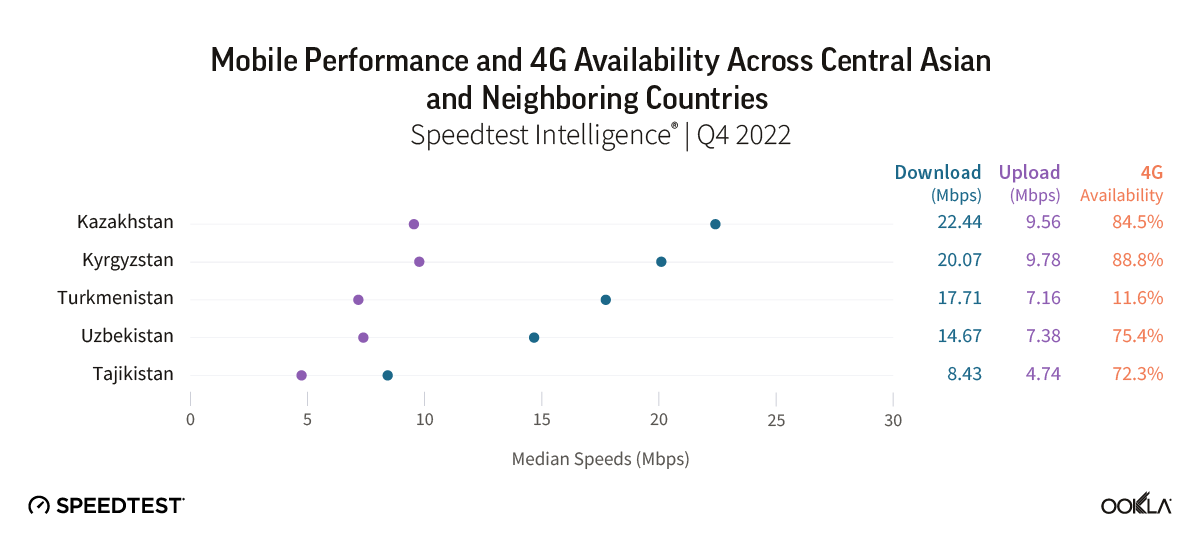

We used Speedtest Intelligence® data to compare performance across Central Asian countries. Kazakhstan had the fastest median mobile download speed at 22.44 Mbps during Q4 2022, and Kyrgyzstan topped the ranks for median upload speed at 9.78 Mbps.

Kyrgyzstan also came first in terms of 4G at 88.8%, up from 81.9% in Q2 2021. Tajikistan made the most progress with regard to 4G Availability — increasing by 12.8 ppt from 59.5% in Q4 2021 to 72.3% in Q4 2022, followed by Uzbekistan, which increased from 67.1% 4G Availability in Q4 2021 to 75.4% in Q4 2022. Turkmenistan had the lowest 4G Availability at 11.6% in Q4 2022, far behind its peers but up from a year prior (6.5% in Q4 2021).

Across Central Asia, where close to half of the population lives in rural areas, it is imperative to make sure that those communities are not left behind when it comes to fast and reliable internet. Speedtest Global Index™ shows that the “stans” still have a way to go to improve their ranking. Governments across Central Asia need to address the root cause of the poor connectivity, which partially stems from the lack of an open and competitive telecom market.

The International Telecommunication Union (ITU) ICT Regulatory Tracker sheds light on where Central Asia sits when it comes to regulatory environment — it provides a composite score derived from a set of 50 indicators across four pillars such as regulatory mandate, regulatory authority, regulatory regimen, and competitive framework, as follows:

G1: Regulated public monopolies — command and control approach

G2: Basic reform — partial liberalization and privatization across the layers

G3: Enabling investment, innovation, and access — dual focus on stimulating competition in service and content delivery, and consumer protection

G4: Integrated regulation — led by economic and social policy goal

The ITU puts three of the five countries: Tajikistan, Uzbekistan, and Turkmenistan, as regulated public monopolies (G1). Kazakhstan (G2) and Kyrgyzstan (G3) have more supportive regulatory environments, but none of the countries is fully transparent.

Central Asia embraces digitalization to level up

The availability and quality of mobile networks are crucial across Central Asia due to the low proliferation of fixed-line broadband and mobile being the only de-facto connectivity option, especially in Tajikistan, Turkmenistan, and Kyrgyzstan. Access to mobile broadband enables a range of services, such as mobile banking and remote education, which are key to digital inclusion and supporting economic growth. All Central Asian countries, bar Turkmenistan, have put strategies in place to stimulate telecom infrastructure and the wider ecosystem.

ITU ranks Kazakhstan’s regulatory status as G2 means that basic reform took place, and the market is partially liberalized and privatized. Through the Digital Kazakhstan program, Kazakhstan set an ambitious goal to ensure 100% country coverage with high-quality internet and 95% home broadband adoption by 2025. Furthermore, in 2020, Beeline, Kcell, and Tele2 agreed to deploy a shared network to support the government’s “250+” project, which aims to extend high-speed internet to all villages of more than 250 residents. Each operator will build and operate the network in one area providing equal access to the shared infrastructure to the other parties. The five-year project will deliver 3G/4G service to 600,000 people in nearly 1,000 rural settlements. Also, the operators offer a special social tariff, “Tugan zher,” for less than 900 tenges ($1.88).

The Kyrgyz Republic, known as Kyrgyzstan, has the highest levels of mobile penetration across Central Asian countries — 159.9% with 2.94 SIMs per unique mobile subscriber, according to GSMA Intelligence. Despite being the second poorest country across CA, Kyrgyzstan came first regarding 4G Availability (the proportion of users of 4G-capable devices who spend most of their time on 4G networks). The National Development Strategy of the Kyrgyz Republic 2018-2040 is one initiative that facilitates digital transformation to hasten the country’s economic development. The State Communications Agency (SCA) stated in its annual report for 2021 that a total of 2,049 settlements across the country were covered by 4G LTE mobile networks at the end of 2021, equivalent to 96% of the country’s 2,130 officially registered cities, towns and villages. 2G mobile network technology extended to 2,088 locations (98%), while 3G networks were present in 2,081 (97%). Overall, 42 settlements (1.9%) were outside mobile network coverage, some due to a lack of power transmission lines.

At the end of 2020, Uzbekistan embarked on a “Digital Uzbekistan 2030” strategy to stimulate the country’s digital transformation across various industries. To achieve this, Uzbekistan is expanding its telecommunication infrastructure to improve communication quality and close the urban-rural divide (50% of the population lives in rural areas) by inking several partnerships. VEON, Beeline Uzbekistan’s parent company, announced in May 2022 that it would invest $250 million over the next five years to develop the communications infrastructure and ecosystem of digital services in Uzbekistan to support Digital Uzbekistan 2030.

Andrzej Malinowski, the CEO of Beeline Uzbekistan, acknowledges that “there is a clear understanding that (mobile) is a driver of the economy and the best way to further improve education level within the country. We want to enable remote education and build an education platform as a social project, make it zero-rated and available to all”.

VEON also announced it would advise and provide digitalization services to the Uzbek government during the country’s accession to the World Trade Organization (WTO). In September 2022, state-backed Uzbektelecom signed eight contracts with Huawei and ZTE worth $506.8 million. The deal, backed by Uzbekistan’s Ministry of Information Technologies and Communications (MITC), to implement a telecommunication network and infrastructure across the western and eastern regions of the country in two phases to deliver expanded population coverage and QoS. Furthermore, Uzbektelecom has also signed a contract with four Japanese companies — NTT, NEC, Toyota Tsusho, and Internet Initiative Japan (IIJ) — to deploy a telecommunications infrastructure development project to provide data center and telecommunication infrastructure to enable “Digital Uzbekistan 2030”.

Tajikistan is the poorest country in Central Asia, with most of the population living in rural areas (72%). Unsurprisingly, the country ranked low on the Speedtest Global Index, taking 132nd place for mobile and 124th for fixed networks. According to the State Communication Service, only one-third of the population (3.3 million) used mobile Internet in Tajikistan in 2021. One of the reasons behind this is the high expense of mobile broadband subscriptions which costs on average 7.5% of monthly GNI per capita, as per data from the ITU, one of the highest in the region. It also has one of the largest (20 percentage points) gender gaps in mobile ownership. Tajikistan outlined its priorities in the National Development Strategy 2030, as it aims to leverage digital technologies to fight poverty, achieve energy independence, boost food security, and create new jobs for the population.

Turkmenistan, known for its autocratic government and large gas reserves, has the least developed telecommunications sector across Central Asia, partially because of the strong government control over most economic activities, including telecommunication which prevents foreign investment. ITU gave the country an overall score of 6.70 in 2022, second worst only to Djibouti. There is only one operator in the country, Altyn Asyr, which operates under the brand name TM Cell after MTS exited the market in 2019. The lack of competition harms telecommunication services’ availability, affordability, and quality. The treatment of MTS doesn’t encourage foreign investment, which the country desperately needs to build telecom infrastructure. In late 2021, Turkmenistan reportedly purchased equipment, software, and technical support from Huawei.

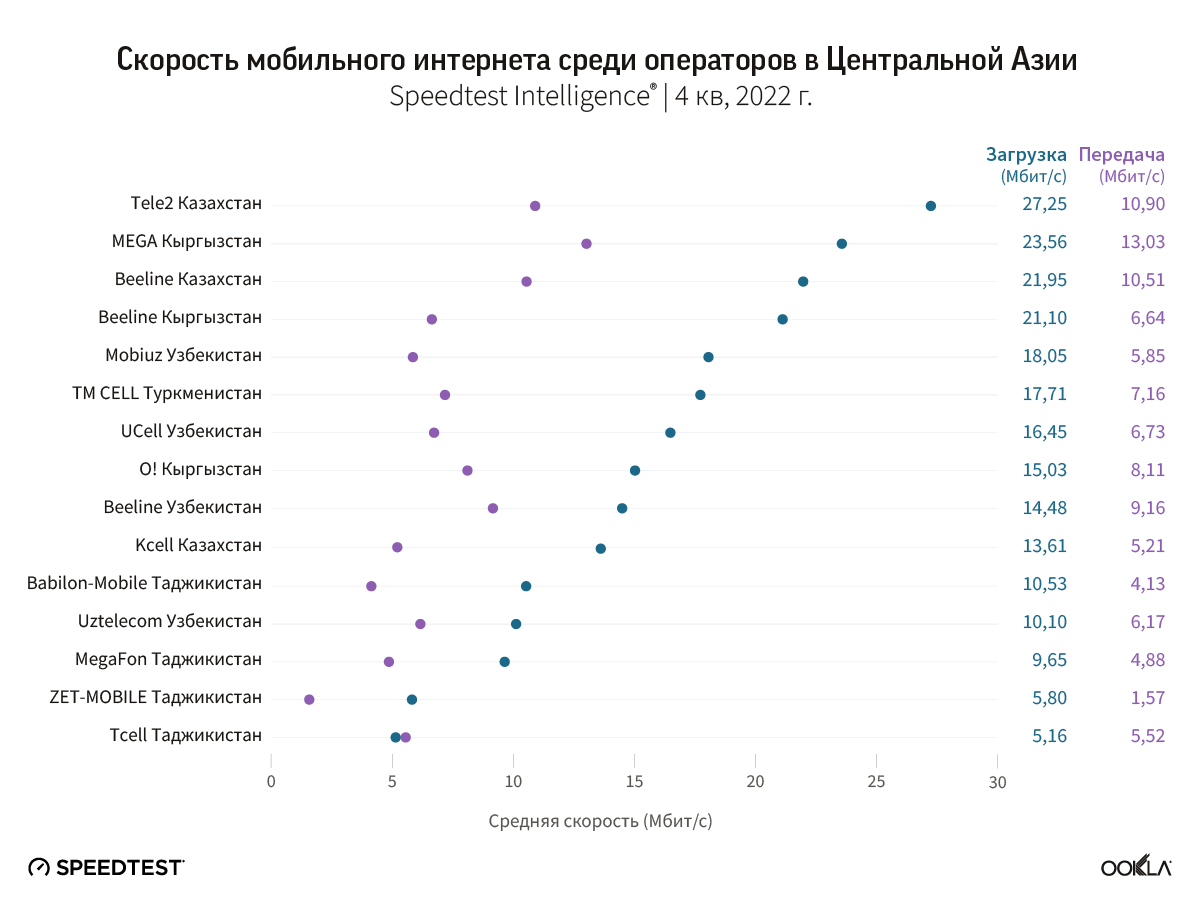

Tele 2 Kazakhstan topped median download speed; Mega Kyrgyzstan uploads

Tele 2 Kazakhstan achieved the fastest median mobile download speed across all of the operators in Central Asia in Q4 2022, of 27.25 Mbps, a slight uptick over Q4 2021 (26.13 Mbps median download speed). The only privately owned company in Kazakhstan, Beeline Kazakhstan, was the second fastest operator in Kazakhstan and third across Central Asia — the operator’s investment into mobile is paying off as it has increased its median download speed from 17.97 Mbps in Q4 2021 to 21.95 Mbps in Q4 2022. The operator reported 7.2 million 4G users in Q3 2022, a 25.5% year-on-year increase, translating into 69% 4G penetration of the total customer base (7 percentage points year over year). Beeline Kazakhstan is already the largest mobile operator in the country, with around 42% market share, and it is also the winner regarding mobile number portability.

Kyrgyz operators performed well on 4G Availability

4G Availability is a function of smartphone availability and affordability and 4G coverage. According to the National Statistics Office, smartphone shipments to Kyrgyzstan reached 968,000 units between January and July 2022, of which the majority (872,000) were from China, with an average price of $69. Affordable smartphone shipments, combined with the operators’ efforts to expand 4G LTE network coverage, resulted in Kyrgyz operators topping the 4G Availability rankings in Central Asia. The top-ranking operator regarding 4G Availability has had an eventful past couple of months. In December 2022, Megacom Kyrgyzstan, run by the state-owned Alfa-Telecom, started its rebranding campaign to MEGA following Megacom ownership transfer to the state-owned Kyrgyzstan State Development Bank. The operator announced that it expanded and upgraded its 2G, 3G, and 4G networks in seven regions and the capital of the Kyrgyz Republic. It plans to continue network coverage expansion across remote areas of Kyrgyzstan.

The second operator on the chart, Sky Mobile, operating under the Beeline Kyrgyzstan brand, announced In September 2022 that it has expanded its LTE network by deploying or upgrading 1,000 base stations. Additionally, between November 2021 and May 2022, Beeline Kyrgyzstan offered smartphones in installments for six or twelve months bundled with its mobile service package.

Tele2 and Kcell, controlled by the same company Kazakhtelecom, differ regarding 4G Availability. Kcell reported that the 4G/5G smartphone share of total subscribers was 72.8% in Q2 2022 (3.6% higher than a year prior), while LTE traffic accounted for 78.7% of all traffic. Kcell is actively working on expanding LTE coverage — it has increased from 65.1% in 2020 to 67.5% as of 1H 2022. At the end of end-2022, around Kazhtelecom’s twin subsidiaries: Kcell and Tele2-Altel, operated 14,000 cellular base stations. On the other hand, Beeline Kazakhstan, part of the VEON group, reported that it installed over 4,000 base stations during 2022, taking its total to more than 25,000 base stations. The operator also stated it provides 97% LTE coverage within each area where it has deployed 4G base stations.

Beeline Uzbekistan outperformed other Uzbek operators on 4G Availability; the operator stated that it covered 79% of the population with an LTE network in 2022, a 16% year-over-year increase. In Q3 2022, the operator reported a 40% year-over-year data revenue increase based on strong mobile data usage (+42.2% YoY). 4G users grew by almost 35% during Q3 2022 to 5.2 million, driven by an expanded network rollout and portfolio of digital products. The absence of big tech such as Spotify means Beeline can drive local content. Beeline Uzbekistan follows its parent company’s strategy of offering digital products and bundles, which helps with churn reduction and increased consumer loyalty — 33% of its customers are multiplayer consumers. My Beeline, its locally developed self-service app, had 2.6 million monthly active users (MAUs) — almost a third more than a year ago. Local entertainment platforms such as Beeline TV and Beeline Music had 1.2 million MAUs. Beeline has set up a wholly owned software house called BeeLab, which has been recently awarded a license from the Uzbekistan Central Bank to provide payment services. Beeline Uzbekistan subscribers can pay for a total of 500 services by using the Beepul mobile application. Mr Malinowski recognized a need to build an ecosystem around mobile payment to bring a third of the Uzbek population, currently unbanked, into the economy to enable a cashless society.

Megafon Tajikistan outran other Tajik operators in Q4 2022; its network investment can partially explain this — it announced that the number of 4G base stations increased by nearly 40% during 2022, while it added around 300 4G base stations until November 2022.

The International Finance Corporation (IFC), part of the World Bank, provided a $30 million loan to Tcell, the largest mobile operator in Tajikistan, to support its network expansion and improve connectivity across the country, especially in remote, less-densely populated areas of the country.

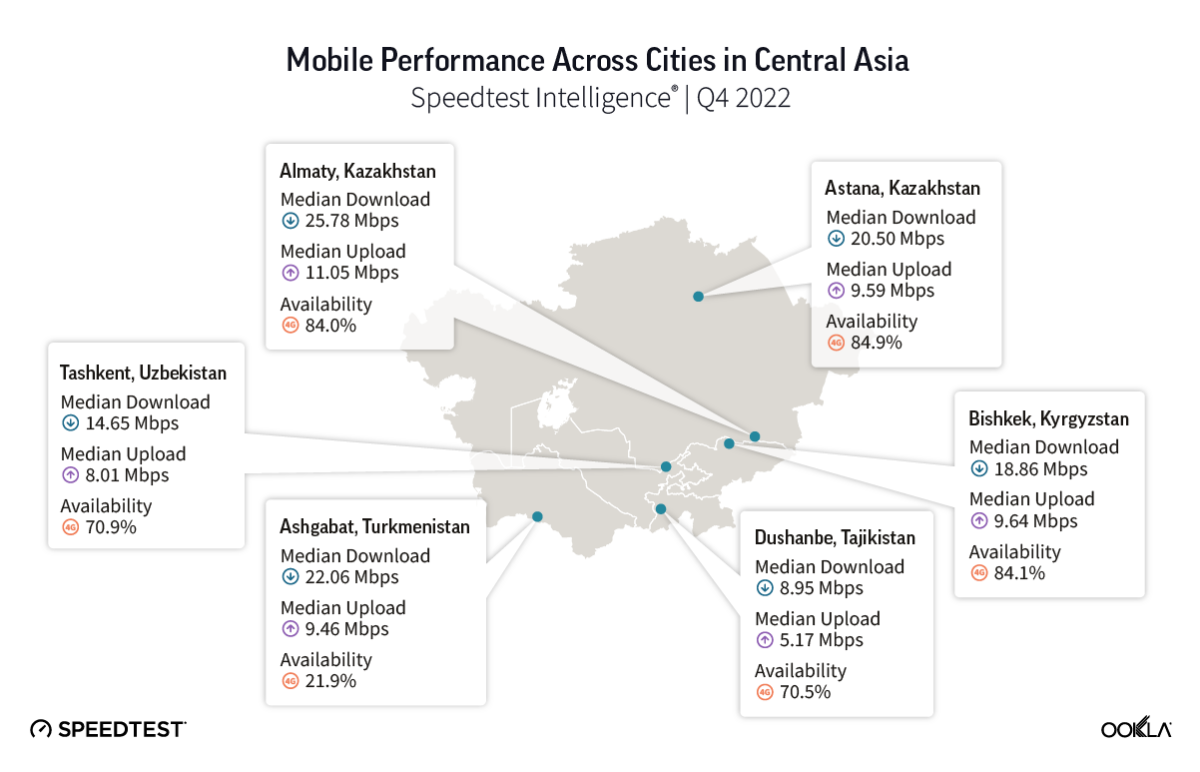

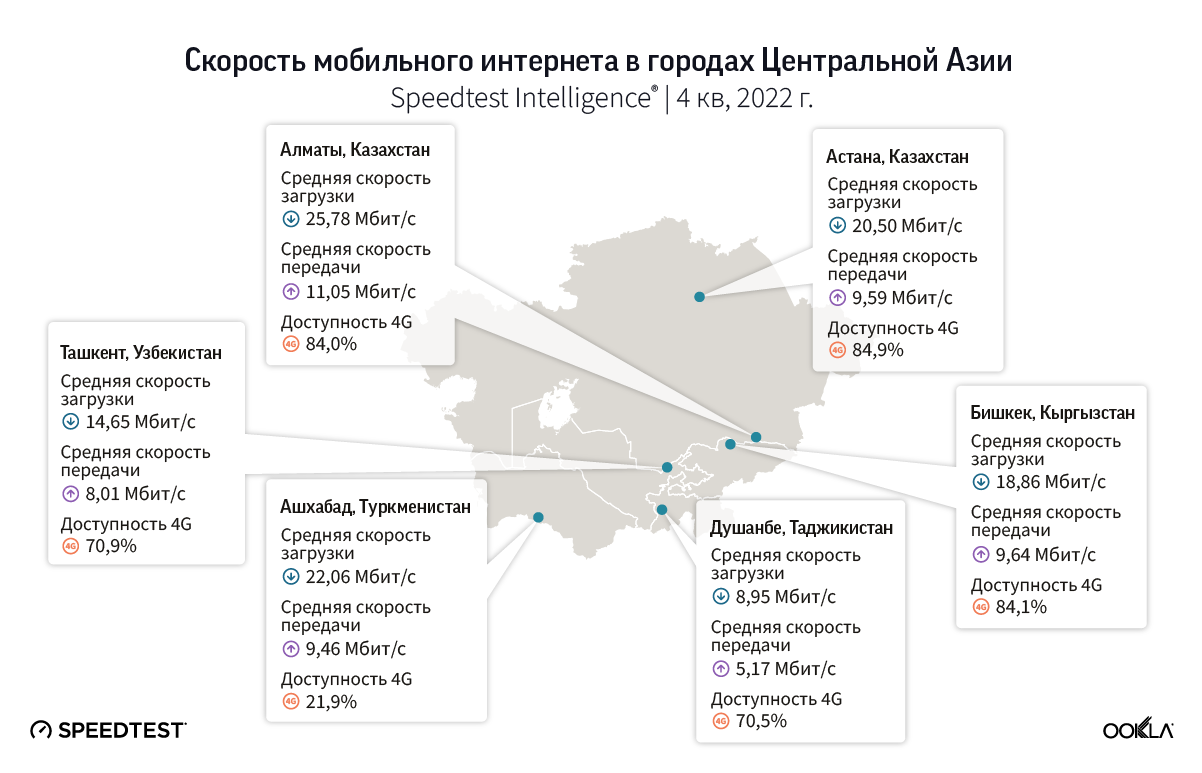

Almaty in Kazakhstan took the top spot in terms of mobile download speed

Given that Kazakhstan had the fastest mobile speed amongst its peers, it is not surprising that Almaty, the largest city in Kazakhstan, the country’s former capital, and financial and cultural center of Central Asia, was the top-ranked city in Q4 2022, with a median download speed of 25.78 Mbps and 11.06 Mbps upload speed. Tele2’s median download speed was 30.10 Mbps, just ahead of Beeline with 29.27 Mbps but double that of Kcell (12.39 Mbps download speed).

Despite Kyrgyzstan having the best 4G Availability across neighboring countries, this is not the case when it comes to capital cities; three cities share the honors here: 4G Availability in the Kazakh cities of Almaty and Astana, and the capital of Kyrgyzstan, Bishkek, exceeded 84%.

4G for all, or 5G for a few?

Across the countries Beeline operates, its strategy is to primarily deploy 4G networks rather than to focus on 5G. This was particularly visible as Beeline didn’t participate in Kazakhstan’s latest 5G spectrum auction. In December 2022, the consortium of mobile operators Mobile Telecom Services (Tele2 and Altel brands) and Kcell (Kcell and Active brand), both controlled by Kazakhtelecom, won two 100 MHz blocks in the 3.6 – 3.7 GHz and 3.7 – 3.8 GHz spectrum band. In December 2022, the Minister of Digital Development announced that 75% of Astana, Almaty, and Shymkent and 60% of regional centers will be covered by 5G networks by 2027. The state-owned operator, Kazakhtelecom, already outlined its plans concerning the 5G services launch, with the first 486 base stations scheduled to be launched in Astana, Almaty, and Shymkent in 2023, ahead of a wider rollout of over 7,000 5G cell sites across the Kcell and Tele2-Altel networks by the end of 2025.

Operators across the rest of Central Asia, apart from Turkmenistan, followed suit. Mobile operators started to deploy and test 5G networks, although with limited geographic reach.

Surprisingly Tajikistan was one of the first countries in Central Asia to launch 5G. MegaFon Tajikistan was the first in Tajikistan to activate a 5G base station in Dushanbe in February 2020, followed by Tcell in August 2020, and ZET Mobile in 2021. Operators in Kyrgyzstan are piloting 5G as well. In September 2022, MegaCom, in partnership with Huawei and the Ministry of Digital Development, launched a 5G showcase zone in Bishkek. Nur Telecom (O!) opened a second demo zone in October 2022 in the city of Osh, in addition to the one in Bishkek.

Central Asian countries understand the benefits digital transformation brings, and some, such as Uzbekistan and Kazakhstan, have initiatives to stimulate mobile adoption and drive the country’s digital transformation. Others need to take a hard look at the regulatory and competitive landscape to drive telecom market development.

Operators continue to modernize their networks and we are keeping a close eye on how the network deployments are progressing and the network performance end users experience. If you are interested in benchmarking your performance or if you’d like to learn more about internet speeds and performance in other markets around the world visit the Speedtest Global Index.

5G приходит в Центральную Азию, в связи с чем возникает вопрос: какова текущая производительность и доступность мобильных сетей? В этой статье мы рассмотрим состояние мобильных сетей в пяти странах, входящих в регион Центральной Азии: Казахстане, Кыргызстане, Таджикистане, Узбекистане и Туркменистане. Регион Центральной Азии объединяет страны с различным уровнем доходов, включая как высокий, так и низкий, а также обладающие богатыми природными ресурсами и имеющие общую историю. Страны региона признают, что они должны обеспечить хорошую связь, чтобы люди и экономика могли извлечь выгоду из цифровой трансформации.

Основные выводы

Необходимость дополнительных рыночных реформ.ICT Regulatory Tracker Международного союза электросвязи относит три из пяти стран, Таджикистан, Узбекистан и Туркменистан, к регулируемым государственным монополиям (G1). Казахстан и Кыргызстан имеют более благоприятную нормативно-правовую базу, но ни одна из стран не является полностью прозрачной. По данным ICT, улучшенная нормативно-правовая база и эффективность регулирующих органов коррелируют с увеличением инвестиций в телекоммуникации, что положительно влияет на покрытие, ценовую конкурентоспособность, уровень внедрения и ВВП на душу населения.

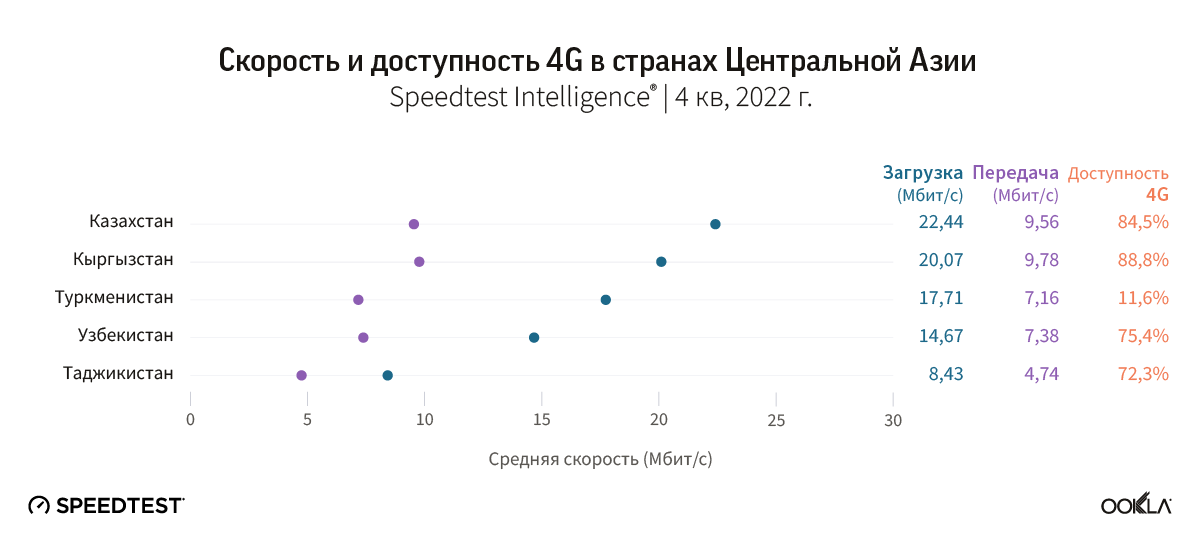

Казахстан лидирует по средней скорости загрузки. Казахстан возглавил рейтинг по скорости загрузки с мобильных устройств, а Tele 2 Kazakhstan — по средней скорости загрузки среди всех операторов Центральной Азии в четвертом квартале 2022 года.

Кыргызстан показал хорошие результаты по доступности 4G. Благодаря благоприятной нормативно-правовой среде Кыргызстан превосходит своих более богатых соседей с точки зрения скорости и доступности 4G.

Ставка на цифровую трансформацию. Помимо Туркменистана, в странах Центральной Азии есть инициативы по стимулированию внедрения мобильных устройств и цифровой трансформации. Узбекистан и Казахстан, в частности, инвестируют в цифровую инфраструктуру, чтобы стимулировать все аспекты цифровой экономики.

Казахстан и Кыргызстан имеют лучшую мобильную связь в Центральной Азии

Мы воспользовались данными Speedtest Intelligence®, чтобы сравнить скорость в странах Центральной Азии. В четвертом квартале 2022 года у Казахстана была самая высокая средняя скорость загрузки с мобильных устройств — 22,44 Мбит/с, а Кыргызстан возглавил рейтинг по средней скорости передачи — 9,78 Мбит/с.

Кыргызстан также занял первое место по доступности 4G с 88,8 % по сравнению с 81,9 % во втором квартале 2021 года. Таджикистан добился наибольшего прогресса в отношении доступности 4G, показав рост на 12,8 п. п. с 59,5 % в четвертом квартале 2021 года до 72,3 % в четвертом квартале 2022 года. Далее следует Узбекистан, в котором доступность 4G увеличилась с 67,1 % в четвертом квартале 2021 года до 75,4% в четвертом квартале 2022 года. В Туркменистане был самый низкий уровень доступности 4G — 11,6 % в четвертом квартале 2022 года, что значительно уступает показателям соседей, но выше, чем годом ранее (6,5 % в четвертом квартале 2021 года).

В Центральной Азии, где почти половина населения проживает в сельской местности, крайне важно, чтобы населению был доступен быстрый и надежный интернет. СогласноSpeedtest Global Index™, «станам» еще есть куда стремиться, чтобы улучшить свой рейтинг. Правительствам стран Центральной Азии необходимо устранить первопричину плохой связи, которая частично связана с отсутствием открытого и конкурентного рынка телекоммуникаций.

ICT Regulatory Tracker Международного союза электросвязи (ITU) проливает свет на положение Центральной Азии в том, что касается регулирования. Трекер предоставляет сводную оценку, полученную из набора 50 показателей по четырем основным элементам, таким как регулирующий мандат, регулирующий орган, режим регулирования и конкурентная среда, как показано ниже.

G1: регулируемые государственные монополии — командно-управленческий подход

G2: базовая реформа — частичная либерализация и многоуровневая приватизация

G3: обеспечение инвестиций, инноваций и доступа — двойной акцент на стимулирование конкуренции в сфере предоставления услуг и контента, а также на защиту прав потребителей

G4: интегрированное регулирование — направленное на достижение целей экономической и социальной политики

ITU относит три из пяти стран, Таджикистан, Узбекистан и Туркменистан, к регулируемым государственным монополиям (G1). Казахстан (G2) и Кыргызстан (G3) имеют более благоприятную нормативно-правовую базу, но ни одна из стран не является полностью прозрачной.

Центральная Азия проводит цифровую трансформацию, чтобы подняться на новый уровень

Доступность и качество мобильных сетей имеют решающее значение в Центральной Азии из-за низкого распространения стационарной широкополосной связи, а мобильная связь является фактически единственным вариантом выхода в сеть, особенно в Таджикистане, Туркменистане и Кыргызстане. Доступ к мобильной широкополосной связи позволяет предоставлять ряд услуг, таких как мобильный банкинг и дистанционное обучение, которые имеют ключевое значение для охвата цифровыми технологиями и поддержки экономического роста. Все страны Центральной Азии, за исключением Туркменистана, разработали стратегии по развитию телекоммуникационной инфраструктуры и расширению экосистемы.

ITU оценивает регулятивный статус Казахстана как G2, что означает, что основные реформы были проведены, а рынок частично либерализован и приватизирован. В рамках программыЦифровой Казахстан, Казахстан поставил перед собой амбициозную цель: к 2025 году на 100 % обеспечить страну качественным интернетом и на 95 % — домашним широкополосным доступом. Кроме того, в 2020 году компании Beeline, Kcell и Tele2 договорились развернуть общую сеть для поддержки государственного проекта «250+», целью которого является распространение высокоскоростного интернета на все села с населением более 250 жителей. Каждый оператор будет строить и эксплуатировать сеть в своей зоне, предоставляя равный доступ к общей инфраструктуре другим сторонам. Пятилетний проект предоставит услуги 3G/4G 600 000 человек почти в 1000 сельских населенных пунктов. Также операторы предлагают специальный социальный тариф «Туган жер» стоимостью менее 900 тенге (1,88 долл. США).

По данным GSMA Intelligence, Кыргызская Республика, известная как Кыргызстан, имеет самый высокий уровень проникновения мобильной связи среди стран Центральной Азии — 159,9 % с 2,94 SIM-карты на одного мобильного абонента. Несмотря на то, что Кыргызстан является второй беднейшей страной в Центральной Азии, он занял первое место по доступности 4G (по доле пользователей устройств с поддержкой 4G, которые проводят большую часть своего времени в сетях 4G).«Национальная стратегия развития Кыргызской Республики на 2018–2040 годы» является одной из инициатив, способствующих цифровой трансформации для ускорения экономического развития страны. Государственное агентство связи (SCA) в своемгодовом отчете за 2021 год сообщило, что на конец 2021 года мобильными сетями 4G LTE было покрыто 2049 населенных пунктов, что соответствует 96 % из 2130 официально зарегистрированных городов, поселков и сел страны. Технология мобильных сетей 2G распространилась на 2088 населенных пунктов (98 %), а сети 3G присутствовали в 2081 (97 %). Всего 42 населенных пункта (1,9 %) оказались вне зоны действия мобильной связи, в том числе из-за отсутствия линий электропередачи.

В конце 2020 года Узбекистан приступил к реализации стратегии «Цифровой Узбекистан — 2030», направленной на стимулирование цифровой трансформации страны в различных отраслях. Для этого Узбекистан расширяет свою телекоммуникационную инфраструктуру, чтобы улучшить качество связи и сократить разрыв между городом и деревней (50 % населения проживает в сельской местности) путем заключения нескольких партнерств. В мае 2022 года VEON, материнская компания Beeline Uzbekistan, объявила, что в течение следующих пяти лет инвестирует 250 миллионов долларов США в развитие коммуникационной инфраструктуры и экосистемы цифровых услуг в Узбекистане для поддержки стратегии «Цифровой Узбекистан — 2030».

Анджей Малиновский, генеральный директор Beeline Uzbekistan, признает, что «существует четкое понимание того, что (мобильная связь) является движущей силой экономики и лучшим способом помочь в улучшении уровня образования в стране. Мы хотим обеспечить дистанционное обучение и построить образовательную платформу как социальный проект, сделать ее безналоговой и доступной для всех».

В VEON также объявили, что будут консультировать и предоставлять услуги по цифровой трансформации правительству Узбекистана во время вступления страны во Всемирную торговую организацию (ВТО).В сентябре 2022 года поддерживаемая государством компания «Узбектелеком» подписала восемь контрактов с Huawei и ZTE на сумму 506,8 млн долларов США. Сделка, поддержанная Министерством информационных технологий и связи Узбекистана, предусматривает внедрение телекоммуникационной сети и инфраструктуры в западных и восточных регионах страны в два этапа, чтобы обеспечить расширенное покрытие для населения и высокое качество услуг. Кроме того, «Узбектелеком» также подписал контракт с четырьмя японскими компаниями — NTT, NEC, Toyota Tsusho и Internet Initiative Japan (IIJ) — на развертывание проекта развития телекоммуникационной инфраструктуры для предоставления центра обработки данных и телекоммуникационной инфраструктуры и поддержки стратегии «Цифровой Узбекистан — 2030».

Таджикистан — самая бедная страна в Центральной Азии, большая часть населения которой проживает в сельской местности (72 %). Неудивительно, что страна получила низкий рейтинг вSpeedtest Global Index, заняв 132-е место для мобильных и 124-е место для стационарных сетей. По данным Государственной службы связи, в 2021 году в Таджикистане только треть населения (3,3 млн человек) пользовалась мобильным интернетом. Одной из причин этого является высокая стоимость подписки на мобильный широкополосный интернет, которая в среднем составляет 7,5 % от месячного ВНД на душу населения (по данным ITU), что является одним из самых высоких показателей в регионе. В стране также наблюдается один из самых больших (20 процентных пунктов) гендерных разрывов в плане владения мобильными устройствами. Таджикистан обозначил свои приоритеты в Национальной стратегии развития до 2030 года, она направлена на использование цифровых технологий для борьбы с бедностью, достижения энергетической независимости, повышения продовольственной безопасности и создания новых рабочих мест для населения.

Туркменистан, известный своим авторитарным правительством и большими запасами газа, имеет наименее развитый телекоммуникационный сектор в Центральной Азии, отчасти из-за сильного государственного контроля над большей частью экономической деятельности, включая телекоммуникации, что препятствует иностранным инвестициям. Союз ITU дал стране общий балл 6,70 в 2022 году, что является вторым худшим показателем после Джибути. В стране действует только один оператор «Алтын Асыр», который, после того, как компания «МТС» ушла с рынка в 2019 году, работает под торговой маркой TM Cell. Отсутствие конкуренции негативно сказывается на зоне покрытия, доступности и качестве телекоммуникационных услуг. Уход «МТС» не способствует привлечению иностранных инвестиций, в которых страна остро нуждается для создания телекоммуникационной инфраструктуры. Сообщается, что в конце 2021 года Туркменистан приобрел оборудование, программное обеспечение и техническую поддержку у Huawei.

Tele 2 Казахстан лидирует по средней скорости загрузки; Mega Кыргызстан — передачи