A year on from our inaugural report, the global 5G SA narrative in 2026 has shifted from a coverage race to a capability contest. The GCC now delivers median download speeds five times those in Europe, while the U.S. has completed its Tier-1 SA launches. Europe is accelerating, but from a low base, and the gap with global leaders risks widening as 5G Advanced scales elsewhere.

The second edition of Ookla and Omdia’s flagship report on the global state of 5G Standalone confirms that the technology has moved beyond launch announcements into an execution-driven phase. By the close of 2025, the “coverage gap” between major economic blocs had narrowed, but a more consequential “capability gap” has emerged, reflecting divergent spectrum strategies, investment depth, and the extent to which operators have moved beyond baseline SA deployment toward end-to-end network optimization.

Globally, 5G SA availability based on Speedtest® sample share reached 17.6% in Q4 2025, up modestly from 16.2% a year earlier, indicating that roughly one in six 5G Speedtests worldwide now occurs on a standalone network. The headline global median SA download speed of 269.51 Mbps represents a 52% premium over non-standalone networks, though this figure masks significant regional variation driven by spectrum allocation depth, carrier aggregation maturity, and user-plane engineering.

For governments and regulators, the stakes of the SA transition have intensified. National competitiveness, digital sovereignty, and AI readiness have converged to reshape investment priorities across major markets. The European Commission’s Digital Networks Act, the U.S.’ supply chain diversification program, and China’s integration of 5G Advanced into its 15th Five-Year Plan all signal that 5G SA is now treated as foundational national infrastructure central to AI ambitions, and not merely a connectivity upgrade.

This year’s report significantly expands the scope of the analysis. For the first time, our research examines 5G SA’s impact on end-user battery life and voice performance (VoNR), quality of experience (QoE) metrics to cloud and gaming infrastructure, and the first wave of commercial monetization strategies spanning consumer network slicing, enterprise SLAs, and 5G Advanced segmentation. We also provide an assessment of the geopolitical context now shaping SA’s evolution, from Europe’s Digital Networks Act to the GCC’s sovereign AI infrastructure strategies.

Key Takeaways:

The GCC has established itself as the global 5G SA performance leader, with the UAE setting the speed benchmark

Led by e& and du’s aggressive 5G Advanced deployments, the Gulf Cooperation Council (GCC) delivered the world’s fastest 5G SA median download speeds in Q4 2025 at 1.13 Gbps, nearly five times that of Europe. The UAE alone reached a median of 1.24 Gbps on SA networks, a speed that would be considered exceptional even for full-fiber broadband in developed markets. The deployment of four-carrier aggregation and enhanced MIMO technology, coupled with the strategic allocation of premium mid-band spectrum to the SA network, demonstrates the performance ceiling that a fully realized 5G SA architecture can achieve.

South Korea followed at 767 Mbps, driven by wide 3.5 GHz channel bandwidth, with the U.S. at 404 Mbps following the completion of nationwide SA deployments by all three Tier-1 operators. Europe, at 205 Mbps, trails all developed regions, though the region’s SA networks still deliver a 45% download speed premium over NSA, confirming the performance value of the SA transition where material spectrum depth is allocated.

Europe’s 5G SA gap with global peers is narrowing, but the region still trails North America by 27 percentage points

Europe’s 5G SA sample share more than doubled from 1.1% to 2.8% between Q4 2024 and Q4 2025, driven by accelerated deployments in Austria (8.7%), Spain (8.3%), the United Kingdom (7.0%), and France (5.9%). These four markets now account for the vast majority of European SA connections. The United Kingdom and France registered the strongest year-on-year acceleration in Europe, each gaining 5.3 percentage points, reflecting the impact of investment-linked merger conditions and competition in the United Kingdom, as well as targeted R&D policy support in France.

U.S. Widens 5G SA Lead Over Europe & Gulf

Speedtest Intelligence® | Q1 2023 – Q4 2025

However, the region still trails North America by 27 percentage points and emerging Asia by 30. At the global level, the U.S. remains the largest accelerator in absolute terms over the last year, with SA sample share rising 8.2 percentage points to 31.6% year-on-year, driven by the sequential rollout of SA across all Tier-1 operators beyond T-Mobile. Firmware fragmentation, where handset OEMs gatekeep SA network access pending individual carrier certification, and tariff structures that fail to incentivize migration from NSA, remain the primary barriers to faster European adoption.

5G SA delivers measurable performance and quality of experience gains, but end-to-end optimization separates leaders from laggards

Globally, SA connections delivered a 52% download speed premium (mostly an artifact of rich spectrum allocation and lower network load) and improved median multi-server latency by over 6% compared to NSA. However, this year’s report finds that a standalone core migration alone does not guarantee a better end-user experience. Quality of experience analysis reveals a nuanced picture: SA improves video and cloud infrastructure latency in Europe versus NSA, but underperforms NSA for gaming latency within the same region. North America records the lowest absolute SA cloud and gaming latency, consistent with dense hyperscaler adjacency and mature interconnect ecosystems.

Among European markets, France (41 ms to cloud endpoints), Austria (48 ms), and Finland (50 ms) demonstrate what is achievable where backbone quality, peering density, and routing discipline are strong. These outcomes reflect an underappreciated end-to-end network stack optimization dividend, encompassing data-center proximity, fiber backhaul depth, and user-plane topology, rather than a pure “SA dividend” alone.

The report also presents early evidence of a tangible consumer benefit of SA: battery life. In the UK, devices on EE’s 5G SA network recorded median discharge times approximately 22% longer than those on NSA, with O2 showing an 11% advantage. These gains likely stem from features like SA’s unified control plane, which eliminates the dual-connectivity overhead of NSA configurations.

Core network investment is accelerating as monetization transitions from concept to selective execution

Omdia’s latest forecasts confirm the industry’s shift toward software-defined core capability as the primary driver of next-cycle investment. Global 5G core software spending is projected to grow at an 8.8% CAGR between 2025 and 2030, with EMEA leading at 16.7%, significantly outpacing North America (5.5%) and Asia & Oceania (4.2%). This reflects EMEA’s later position in the deployment cycle, as the region is entering its period of peak 5G core adoption, while North America’s core spending trajectory is expected to have peaked in 2025 following the commercial launches by AT&T and Verizon. By end of Q3 2025, 83 operators worldwide had deployed 5G core networks, with 5G core investment accounting for 63.6% of global core network function software spending.

5G Core Investment Accelerates Across Regions

Omdia | 2023-2030

On monetization, consumer strategies now span speed tiers (primarily Europe), network slicing (Singapore, France, and the U.S.), and 5G Advanced segmentation packages (China). Enterprise slicing presents the much larger long-term revenue opportunity, with T-Mobile’s SuperMobile representing the first nationwide commercial B2B slicing service in the U.S. Countries with coordinated regulatory frameworks, implementing clear coverage obligations, investment incentives, or infrastructure consolidation policies with deployment remedies, consistently outperform those with fragmented or reactive approaches, reinforcing the report’s finding that policy has emerged as a primary competitive differentiator in 5G SA outcomes globally.

Download the full report

For the comprehensive analysis of 5G SA and 5G Advanced deployment, performance, and monetization across global markets, including new research on battery life, voice performance, quality of experience, geopolitical context, and expanded policy case studies from the UK, France, Brazil, Japan, and the UAE, download the full report, 5G Standalone and 5G Advanced: A Global Reality Check on 5G SA and 5G Advanced in 2026.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

Luke Kehoe leads Ookla’s research and thought leadership efforts in Europe.

An electronic engineering alumnus of University College Dublin, Luke has extensive experience collaborating with mobile operators, telecoms vendors, and government agencies in research and advisory roles across Europe. He has contributed to internationally recognised thought leadership publications in areas such as 5G, IoT, open RAN, and edge computing, working with prestigious organisations like the Telecom Infra Project and the World Economic Forum.

5G SA rollouts are accelerating globally, but device and tariff-side fragmentation continue to drag on real-world usage

Editor’s Note: The 5G SA map in this poster has been updated. The revised version uses Zoom Level 11 tile resolution, consistent with last year’s edition, to better capture full-year network patterns, particularly in highly urbanized markets like China.

The deployment of 5G Standalone networks is accelerating across a widening number of markets, driven by maturing device ecosystems, rising core network investment, and the growing commercial imperative to deliver the performance improvements that the SA architecture can enable. Despite this progress, the gap between operator-reported coverage of 5G SA networks and real-world usage of these networks continues to widen, held back by tariff inertia and device-side fragmentation in network access.

Regional disparities in commercialization progress persist, but the direction of travel is clear. Markets that were virtually absent from the 5G SA landscape a year ago are now registering meaningful deployment levels, and several advanced operators are pushing into the next evolutionary phase with early deployments of 5G Advanced capabilities built on the SA foundation, including new levels of spectrum depth through advanced carrier aggregation features.

Building on the success of last year’s inaugural edition, Ookla® has released an updated high-resolution downloadable poster based on Speedtest Intelligence® data, offering a unified view of the global reach of both 5G NSA and 5G SA networks through 2025. This visual accompanies a new flagship global study in collaboration with Omdia, comparing the competitiveness of leading regions and countries in 5G SA deployment, performance, and monetization.

Key Takeaways

Asia Pacific continues to lead in 5G SA reach, but new entrants are reshaping the global leaderboard

In 2025, six of the top ten countries by 5G SA reach were in Asia Pacific, with China (79.0% 5G SA sample share), India (49.2%), and Singapore (37.0%) maintaining dominant positions globally. China’s lead has been reinforced by multi-operator SA deployments across all major carriers, while India’s position reflects the deep nationwide low-band coverage strategy pushed by Reliance Jio on the 700 MHz band, supplemented by growing mid-band SA rollout. Singapore’s strong showing, meanwhile, reflects the favorable deployment conditions provided by a small landmass and very high urbanization.

The United States (27.6%) has continued its upward trajectory, propelled by T-Mobile’s maturing SA network and commercial launches by both AT&T and Verizon for the first time during the year, while Australia (15.4%) has similarly benefited from multi-operator SA deployments. Thailand (8.5%) and the Philippines (9.0%) round out the Asia Pacific contingent, reflecting growing SA ambitions in Southeast Asia. The UAE (8.0%) has entered the top ten for the first time, signaling a geographic diversification of SA adoption beyond advanced Asian markets. Austria (8.0%) and Spain (8.1%) remain the only European markets in the upper ranks, though the region’s broader trajectory has shifted meaningfully.

APAC Claims 6 of Top 10 Spots in Global 5G SA Reach

Speedtest Intelligence® | 2025

The U.S. sustains its 5G SA performance lead, while the UAE and South Korea demonstrate the ceiling for optimized networks

The United States now combines relatively high 5G SA reach with strong download speeds, a combination that is unusual globally. In Q4 2025, median download speeds on 5G SA in the U.S. reached 403.97 Mbps, building on the gains recorded in the prior year, and significantly ahead of large-scale Asian deployments such as China (212.40 Mbps) and India (222.11 Mbps).

T-Mobile’s “layer cake” spectrum strategy remains the foundation of U.S. 5G SA performance. By pairing broad 600 MHz coverage, initially launched as 5G NSA in 2019 before transitioning to SA in 2020, with dense mid-band deployment in the 2.5 GHz band, the operator has matured its SA network to the point where advanced features such as uplink carrier aggregation and Voice over NR (VoNR) are now widely deployed. Recent 5G SA launches by AT&T and Verizon have extended multi-operator coverage and added the U.S. to the small but burgeoning list of Western markets in which all operators now support nationwide 5G SA networks.

At the top of the global performance table, the UAE has emerged as the clear leader in absolute 5G SA download speeds, registering a median of 1.24 Gbps in Q4 2025. This result is driven by large, contiguous TDD mid-band deployments, intensive carrier aggregation, and site grid densification by Etisalat and du. South Korea sustains its position as a high-performance market at 766.92 Mbps, propelled by its exclusive use of the 3.5 GHz band for 5G, though it continues to trail regional peers in SA reach due to limited commercialization beyond KT. This marks a notable shift from the global leadership South Korea held at the start of the 5G cycle.

5G SA delivers performance uplift across key metrics, but real-world gains in QoE require more than just a core migration

Globally, 5G SA networks are delivering materially improved performance compared to the non-standalone architecture, and the performance gains have held even as SA deployments mature with higher traffic onboarding. In Q4 2025, median download speeds on 5G SA were more than 120% higher than on NSA networks in North America, 57% higher in advanced Asia and Oceania, and 45% higher in Europe. The regional variation reflects differences in spectrum depth, network maturity, and the degree to which operators have activated advanced SA features such as carrier aggregation, rather than any inherent advantage of SA in downlink performance.

Headline latency improvements, a touted beneficiary of the transition to the 5G core, continue to be significant. SA networks delivered median multi-server latency reductions of more than 27% in advanced Asia and Oceania, nearly 24% in North America, and 17% in Europe compared to NSA. However, it is important to note that a standalone core migration alone does not guarantee a better end-user experience in real-world applications. Our quality of experience (QoE) analysis reveals a nuanced picture. SA improves video and cloud infrastructure latency in Europe versus NSA, but underperforms NSA for gaming latency within the same region. North America records the lowest absolute SA cloud and gaming latency, consistent with dense hyperscaler adjacency and mature interconnect ecosystems.

Among European markets, France (41 ms to cloud endpoints), Austria (48 ms), and Finland (50 ms) demonstrate what is achievable where backbone quality, peering density, and routing discipline are strong. These outcomes reflect an underappreciated end-to-end network stack optimization dividend, encompassing data-center proximity, fiber backhaul depth, and user-plane topology, rather than a pure “SA dividend” alone.

The upload story has begun to diverge by region. North America’s SA networks deliver 54% higher upload speeds than NSA, reflecting the early implementation of advanced uplink capabilities. In Europe, however, the upload advantage is just 6%, highlighting the still nascent deployment of features such as higher-order MIMO and uplink carrier aggregation in the region beyond leading countries like the United Kingdom. Advanced Asia and Oceania sit in between at 21%, suggesting that the ecosystem for advanced SA uplink capabilities remains at an early stage in most global markets.

A detailed analysis of the state of 5G SA and 5G Advanced around the world is featured in Ookla’s flagship report, produced in collaboration with Omdia, on regional competitiveness in the technology.

Ookla will be at Mobile World Congress this year, located at Booth 2I28 in Hall 2. Please drop by to discuss the state of connectivity in your market, and how Ookla’s network insights can help deliver better connected experiences.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

Luke Kehoe leads Ookla’s research and thought leadership efforts in Europe.

An electronic engineering alumnus of University College Dublin, Luke has extensive experience collaborating with mobile operators, telecoms vendors, and government agencies in research and advisory roles across Europe. He has contributed to internationally recognised thought leadership publications in areas such as 5G, IoT, open RAN, and edge computing, working with prestigious organisations like the Telecom Infra Project and the World Economic Forum.

Mobile network download speeds declined by more than 50%, while Starlink usage experienced a nearly 200% increase compared to pre-storm baselines

Less than a year after the April 2025 Iberian Peninsula blackout exposed deep vulnerabilities in Portugal’s telecom infrastructure, the country faced another severe test. Between late January and early February 2026, a rapid succession of powerful extratropical cyclones battered the country, knocking out power to over a million customers, disrupting mobile connectivity for hundreds of thousands, and triggering a dramatic spike in satellite broadband usage. Speedtest Intelligence® data captures the scale of network impact and the emerging role of low-earth orbit (LEO) satellite connectivity as a layer of redundancy when terrestrial networks falter.

Key Takeaways:

Median mobile download speeds in Portugal fell by as much as 52.4% from their pre-storm baseline, dropping from 107.3 Mbps to just 51.1 Mbps at their lowest point on February 8, as successive storms compounded network strain.

Mobile upload speeds declined by up to 46.6%, while latency increased by 15.6% and jitter by 27.1% during the worst of the disruption, reflecting significant network congestion and infrastructure stress.

Starlink user activity in Portugal surged by approximately 196% above pre-storm levels at its peak on February 12, with elevated adoption persisting well into late February even as mobile networks began to stabilize.

The data highlights a clear network substitution pattern, with Starlink activity climbing in near-lockstep with mobile speed declinesand fixed network disruptions, reinforcing the case for satellite as a meaningful resilience layer during prolonged terrestrial outages.

Portugal, like many European countries outside the Nordics, continues to lack any binding requirements for specific minimum backup power levels at mobile sites. Recent policy developments in Switzerland and in the EU’s Digital Networks Act (DNA) suggest resilience planning is moving from concept to practical action.

A devastating storm sequence

Storm Kristin made landfall in Portugal’s Leiria district on the night of January 28, 2026, bringing record-breaking winds of over 200 km/h in the Coimbra region and generating over 1,500 emergency incidents in a single night. The storm was the most destructive to hit the country in recent memory, surpassing wind speed records previously held by Hurricane Leslie. Initial disruption was severe, with Reuters reporting more than 3,000 weather-related incidents and electricity distributor E-REDES indicating that outage levels had earlier reached 855,000 customers before restoration work began to reduce that figure.

On the grid side, the damage split across transmission and distribution layers. REN reported 61 very high-voltage pylons knocked down during Storm Kristin and 774 km of very high-voltage lines out of operation, which it said was equivalent to about 7% of Portugal’s transmission grid. E-REDES separately reported more than 600 damaged medium-voltage poles and said that more than one million customers had been left without power at one stage of the event. This distinction is significant because it highlights how resilience bottlenecks emerge across multiple network tiers, not only at the local distribution level.

Telecom disruption was also prolonged. Paulo Fernandes (head of the Central Region Reconstruction Mission Structure) said the affected area started with 307,900 mobile and landline users without communications on 30 January, and that nearly 84,000 customers in the central region still lacked communications almost three weeks later. He also said around 40% of cases were linked to the restoration of electricity supply to mobile sites.

This power dependency aligns with local expert commentary. INESC TEC-linked analysis highlighted that many telecom outages were driven first by loss of electricity at network sites, with a share of the remainder linked to infrastructure faults such as fiber breaks. It was also reported that ANACOM had recommended activation of national roaming, which could help by allowing users to attach to alternative networks where available.

Mobile network performance degradation was severe and sustained, with recovery still ongoing

Analysis of Speedtest Intelligence data paints a detailed picture of how Portugal’s mobile networks responded to the storm sequence. To assess the impact, we established a pre-storm performance baseline using daily median values from January 3 through January 27, 2026, then measured deviations across three distinct phases of disruption.

Prior to the storms, Portugal’s mobile networks were delivering a median download speed of 107.3 Mbps and median upload speed of 15.7 Mbps, with a multi-server latency of 33.5 ms. These figures are consistent with a well-performing mobile market (ranking in the top 30 globally in the latest iteration of the Speedtest Global Index).

The onset of Storm Kristin on January 28 triggered an immediate and sharp decline. Median download speeds fell to 64.5 Mbps that day, a 39.9% drop from baseline, while upload speeds declined 37.4% to 9.8 Mbps. Latency spiked 15.6% to 39 ms and jitter surged 27.1% to 10 ms, indicating significant network congestion as damaged infrastructure concentrated traffic on surviving cells (likely compounded by the loss of fixed connectivity in homes driving more traffic onto the depleted mobile grid).

Rather than recovering, network performance continued to deteriorate in the days that followed as Storms Leonardo and Marta exacerbated the damage. During the sustained disruption phase from February 1 through 14, average median download speeds fell to 59.9 Mbps, a 44.1% decline from baseline. The single worst day came on February 8, during Storm Marta, when median download speeds bottomed out at just 51.1 Mbps, a 52.4% decline. Upload speeds during this phase averaged just 9.5 Mbps, down 39.1% from baseline.

Latency and jitter, often overlooked but critical indicators of quality of experience (QoE) in interactive applications like video conferencing, told a similar story. Median latency during the sustained phase rose to 37 ms, a 10.5% increase over baseline, while jitter averaged 9 ms, up 21.6%. Elevated jitter in particular can reflect the instability characteristic of a network under duress, where routing paths shift unpredictably as infrastructure comes on and offline.

By mid-to-late February, partial recovery was underway. Median download speeds during the February 15 through February 23 period rose to 69.8 Mbps, still 34.9% below baseline but representing meaningful improvement. Upload speeds recovered to 11.0 Mbps (down 29.7%), while latency moderated to 36 ms (up 8.3%). Notably, jitter remained stubbornly elevated at 9 ms (up 21.6%), suggesting that while raw throughput was improving, network stability had not yet fully normalized.

Starlink as a Resilience Layer

As mobile network performance declined, Speedtest data reveals a striking and sustained surge in Starlink usage across Portugal, providing one of the clearest real-world illustrations of satellite connectivity functioning as a resilience layer during prolonged terrestrial disruption.

In the weeks before Storm Kristin, Starlink activity in Portugal was relatively stable. From January 28 onward, however, user activity began climbing sharply. During the acute phase from January 28 through January 31, Starlink user activity averaged 49.4% above baseline, peaking at 61.3% above on January 31 as the scale of mobile network disruption became apparent. This initial surge likely reflects both existing Starlink subscribers increasing their usage in response to degraded mobile and fixed service and new users activating service for the first time.

The sustained disruption phase from February 1 through February 14 saw Starlink activity more than double, averaging 118.4% above baseline. The single highest day came on February 12, when user activity reached approximately 196% above pre-storm levels. This coincided with the period of deepest mobile network degradation (and, likely, fixed network unavailability either due to localized power loss or line faults), providing strong evidence of a network substitution dynamic where some users turned to satellite connectivity as their primary or sole means of internet access.

Perhaps most notably, Starlink user activity did not recede even as mobile networks began their partial recovery. During the February 15 through February 23 period, Starlink activity averaged 151.0% above baseline, substantially higher than even the acute storm phase. This pattern suggests that for many users, the storm experience catalyzed a longer-term shift in connectivity behavior, with satellite maintained as either a primary or backup connection even after terrestrial alternatives began stabilizing.

Portuguese authorities also actively deployed Starlink as an emergency communications tool. Starlink equipment was distributed to remote areas where traditional telecommunications had been knocked offline, helping to bridge the connectivity gap in the hardest-hit communities. This mirrors the pattern observed during the April 2025 Iberian blackout, when Starlink remained operational across the peninsula by routing through ground stations in Italy as Spanish facilities went dark.

It is worth noting that Starlink speeds did moderate as user load increased. Average download speeds during the sustained phase fell to 163.5 Mbps, a 21.7% decline from the pre-storm Starlink baseline of 208.8 Mbps. However, even at their most congested, Starlink speeds remained materially higher than the degraded mobile network’s performance during the same period, delivering nearly three times the median download speed that mobile users were experiencing.

The Regulatory Gap and the Road to Resilience

The storm sequence reinforces a core resilience lesson: in prolonged extreme-weather events, telecom continuity is heavily shaped by power autonomy at sites, restoration logistics, and transport network redundancy, not only by RAN capacity. In practice, the biggest outages often reflect cross-sector interdependence between electricity, fibre transport and mobile access infrastructure.

Indeed, domestically, the storms have reignited debate around the resilience of Portugal’s telecom infrastructure, particularly the adequacy of backup power provisions at mobile sites. The finding that 40% of failures stemmed from power loss at mobile sites, rather than direct storm damage, points to a structural vulnerability that is within regulatory reach to address.

Portugal currently lacks binding requirements for specific minimum backup power autonomy levels at mobile sites. This stands in contrast to Nordic markets such as Norway and Finland, where regulators require between two and six hours of backup power at critical sites, alongside routine stress testing and contingency planning obligations.

In Norway, Nkom’s forsterket ekom programme is a state-backed resilience scheme that hardens selected sites in priority municipalities. Designated mobile sites must have at least 72 hours of backup power, the main transmission path must also have 72 hours, and a separate reserve transmission path is required. Switzerland has also recently codified a phased minimum backup approach. In January 2026, the Federal Council adopted an FDV revision requiring mobile operators to install emergency power at key sites and antennas so mobile service can be maintained for at least four hours from 2031 (with emergency calls covered first, and other services phased in later).

Within the EU, meanwhile, Brussels’ Electronic Communications Code (EECC) permits member states to mandate such provisions but does not require them. The Commission’s DNA proposal, adopted on 21 January 2026, is framed around investment and simplification, but it also directly elevates resilience by introducing an EU-level Preparedness Plan to address rising risks from natural disasters and foreign interference, and by embedding security and resilience criteria into the pan-EU satellite mechanism.

The resilience policy implications arising from this are important. The DNA gives the EU a stronger coordination spine for preparedness, but it does not remove the need for national regulators to set concrete, site-level resilience expectations (including backup-power minimums) that reflect local grid conditions and risk exposure.

On the operator side, Vodafone’s Enhanced Power initiative, launched in November 2025 with Portugal as a first deployment region, targets 10,000-plus mobile infrastructure sites across Europe with backup power provisions ranging from four hours at critical access sites to 72 hours at core mobile data centers. The initiative incorporates AI-based systems to predict and conserve backup power duration. Separately, Portugal’s government has announced a €400 (US$ 471) million investment package for grid resilience, including a 750 MW battery storage expansion.

The experience of January and February 2026 reinforces what the Storm Éowyn analysis across the UK and Ireland also demonstrated: that the resilience of mobile networks in extreme weather is fundamentally a function of power autonomy at mobile sites. Where terrestrial infrastructure falls short, satellite connectivity is increasingly proving its value, not as a replacement for mobile networks, but as a complementary layer of redundancy that can sustain connectivity when ground-based systems falter.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

Luke Kehoe leads Ookla’s research and thought leadership efforts in Europe.

An electronic engineering alumnus of University College Dublin, Luke has extensive experience collaborating with mobile operators, telecoms vendors, and government agencies in research and advisory roles across Europe. He has contributed to internationally recognised thought leadership publications in areas such as 5G, IoT, open RAN, and edge computing, working with prestigious organisations like the Telecom Infra Project and the World Economic Forum.

Spain continues to lead Europe in fiber rollout, but lagging mobile performance undermines country’s overall telecoms competitiveness

The dynamism of Spain’s telecoms market stood out among its European peers last year, with a flurry of mergers reshaping the market’s structure and strong investment in next-generation networks, supported by targeted government initiatives, improving outcomes for Spanish consumers. However, while increased fiber and 5G penetration have driven notable year-on-year improvements in overall network performance, Spain’s international competitiveness in telecoms remains highly imbalanced between its fixed and mobile infrastructure.

The country’s credentials as Europe’s preeminent fiber leader remain intact. In 2024, Spain ranked among the top three in the EU for fiber-to-the-premises (FTTP) coverage (95.2%) and the share of fixed broadband subscriptions providing download speeds above 100 Mbps (93.5%), according to the latest edition of the European Commission’s ‘State of the Digital Decade’ report. This continues to position the country significantly ahead of some of the bloc’s largest economies, most notably Germany, which still lags in FTTP coverage (28.8%) due to a slow shift away from cable networks.

Analysis of Speedtest Intelligence® data reveals that median fixed download speeds in Spain increased from 173.32 Mbps to 210.46 Mbps between 2023 and 2024. This trend of improvement was mirrored across other fixed network performance metrics, with upload speeds increasing in the same period from 129.62 Mbps to 155.53 Mbps. In Q3 2024, DIGI achieved a median fixed download speed of 321.21 Mbps in the Spanish market, followed by Jazztel (273.18 Mbps), Orange (262.78 Mbps), Yoigo (255.74 Mbps) and Movistar (180.30 Mbps).

Spain Leads Europe in Fiber Deployment and Adoption, Boasting the Highest Coverage Among the EU's Top 10 Economies

European Commission | DESI 2018 – 2024

Having achieved exceptionally high levels of FTTP penetration across urban, suburban and rural areas—placing Spain among the top three in the European Commission’s DESI 2024 Index for FTTP coverage in sparsely populated rural areas—the focus in Spain is shifting toward enhancing quality of experience (QoE) in core use cases such as gaming and video streaming. Despite boasting higher FTTP coverage and take-up rates, Spain ranks below countries like France in Ookla’s Speedtest Global Index™. This disparity highlights the influence of factors such as Wi-Fi technology—France has a higher penetration of Wi-Fi 6 and 7 in ISP-provided CPE—and tariff provisioned speeds, with a larger share of fiber customers in France subscribing to multi-gigabit plans, on fixed broadband performance.

DIGI’s strong fixed download speed performance in Spain, detailed in Ookla’s Speedtest Connectivity Report for 1H 2024, is underpinned by similar favourable factors. Notably, it was first to market in Spain with a 10 Gbps service, fully leveraging its XGS-PON fiber infrastructure. With highly competitive pricing—starting at just €20 per month for 1 Gbps and €25 per month for 10 Gbps, including Wi-Fi 6 CPE as standard—DIGI has quickly secured a significant share of multi-gigabit capable connections in the Spanish market.

Autonomous Communities in Northern Spain Lead in Fixed Download Speed Performance

Speedtest Intelligence® | 2024

In addition to highlighting the importance of modern CPE and higher tariff-provisioned speeds, DIGI’s business last year exemplified the accelerating consolidation trends in Spain’s highly overbuilt and fragmented fiber market. The acquisition of DIGI’s fiber infrastructure by a Macquarie-led consortium, which solidified wholesale specialist Onivia’s status as the largest of the ‘neutral’ FTTP networks in Spain, dovetailed with developments such as Telefónica’s BlueVia wholesale spin-off, the emergence of MásOrange and Zegona-controlled Vodafone’s ‘FiberCo’ tie-ups with both Telefónica and MásOrange.

As observed in other European markets with significant fiber overbuild, such as the alt-net model in the UK, consolidation is a slow and challenging process. However, Spanish operators continue to pursue it to enhance the economics of their fiber investments in highly overbuilt urban areas, unlocking scale and resources to capture future growth in rural areas where overlapping infrastructure is less common. This begins with small local operators—of which there are hundreds—being absorbed by ‘local consolidators’. These are then integrated into the infrastructure portfolios of regional consolidators, ultimately leading to acquisition by one of the largest traditional players.

Fiber Overbuild from Smaller Players like DIGI Drives Market Share Shift from Incumbents

Analysis of CNMC Market Data | 2022 – 2024

This gradual process of consolidation is reshaping the fiber business model in Spain, as traditional operators separate their infrastructure and service units to support the growth of wholesale offerings. The coming year will provide some insight into whether a consolidated third player can successfully compete and coexist alongside the vertically integrated Telefónica and MásOrange in the long-term.

MásOrange is vying for network leadership in Spain, founded on a significant spectrum advantage

The winds of consolidation have swept through the Spanish mobile market too, culminating last year in the European Commission’s approval of a 50:50 joint venture between MásMóvil and Orange. The merger has pole-vaulted the newly formed ‘MásOrange’ into a leading position in the market, both in subscription and spectrum share. To secure regulatory approval from Brussels, the merging entity committed to divesting 60 MHz of spectrum, including 20 MHz in the 3.5 GHz band, to facilitate the entry of DIGI as a fully-fledged independent mobile operator, effectively restoring the Spanish market to a four-player structure and ‘exerting a strong competitive constraint on the joint venture’.

In addition to diversifying its portfolio of brands through the merger—with Orange and Yoigo catering to the premium segment, Jazztel and MásMóvil focusing on value for money and regional brands like Euskaltel and Telecable serving local needs—MásOrange hopes its consolidated spectrum assets will enable it to achieve network leadership in the Spanish mobile market.

Movistar Revenues Stable YoY in Q3 2024 while Vodafone and MásOrange Face Declines

Analysis of CNMC Market Data | 2022 – 2024

The merged entity’s consolidated network will be primarily based on Orange’s infrastructure, complemented by MásMóvil’s existing site portfolio and the deployment of new greenfield sites. The integration of MásMóvil’s network, which relies entirely on mid- and high-band spectrum and has historically depended on a national roaming agreement with Orange, creates a natural synergy for the merged entity. It enables the integrated network to leverage MásMóvil’s capacity and density in urban areas alongside Orange’s extensive coverage and nationwide reach.

MásOrange is particularly focused on vying to unseat Movistar’s dominance in the premium segment, a position it has long upheld thanks to its emphasis on superior network quality. Movistar emerged as the fastest mobile operator in the Spanish market in Ookla’s Speedtest Connectivity Report for 1H 2024, delivering the highest median download speeds of 82.68 Mbps. This placed Movistar significantly ahead of Orange (56.42 Mbps) and Yoigo (36.73 Mbps).

The merged entity’s spectrum advantage is heavily weighted toward mid- and high-bands, which are typically utilised for 5G deployments in urban and suburban areas. According to data published by MásOrange, it holds 37% of all mid- and high-band assets in the Spanish market—compared to 28% and 26% for its closest competitor, Telefónica—giving it a unique opportunity to enhance 5G speed performance and gain a competitive edge.

Movistar has maintained its strong 5G speed performance with a 100 MHz allocation in the 3.5 GHz band, but this is now overshadowed by MasOrange’s expanded allocation of 170 MHz. Capital investment by the merged entity in upgrading the 5G RAN to support advanced carrier aggregation (CA) capabilities and the standalone (SA) architecture will enable it to fully realise the performance benefits of wider channel bandwidth through the extensive deployment of its 3.5 GHz spectrum across its consolidated mobile site grid.

Seville Leads in 5G Download Speed Among Spain's Largest Cities, but Operator Performance Varies Widely

Speedtest Intelligence® | Q3 2024

To establish network leadership in coverage, however, MásOrange will need to move beyond its spectrum advantage and focus on increasing the number of physical sites in rural areas within its integrated network. In Q3 2024, Vodafone and Movistar recorded 4G Availability of 95.1% and 93.4% respectively in the Spanish market, followed by Orange at 92.7% and Yoigo at 91.5%.

In parallel to MásOrange’s network consolidation journey, DIGI is building out its own infrastructure to gradually wean itself off dependence on a national roaming and RAN sharing agreement with Telefónica (which DIGI selected over MásOrange, despite both being options under the merger conditions), starting with urban and suburban areas. The European Commission designed the spectrum divestment remedies to position DIGI to replicate the competitive pressure previously exerted by MásMóvil. The goal is for DIGI to carry a similar share of its total mobile data traffic on its own network in the coming years, at least matching the 40-60% on-net share that MásMóvil achieved pre-merger.

Spain's Rural Provinces Trail in 5G Availability, Highlighting the Importance of Government Support through UNICO

Speedtest Intelligence® | Overall 5G Availability (%) in 2024

More broadly, it is hoped that the substantial long-term investment commitments from DIGI and MásOrange, driven by the consolidation activity, combined with government support through programmes such as Unico, will bolster Spain’s international competitiveness in mobile performance in the coming years. The country has significant catching up to do, ranking 57th in the Speedtest Global Index at the end of 2024 and trailing most of its European peers across a suite of network performance metrics, including download speed, consistency and coverage.

La consolidación cambia las telecomunicaciones españolas en 2025

España sigue a la cabeza en despliegue de fibra en Europa, pero el rezagado desempeño móvil reduce la competitividad del país

El dinamismo del mercado español de telecomunicaciones destacó el año pasado frente al de otros mercados europeos, por fusiones que modificaron la estructura del sector y una fuerte inversión en redes de próxima generación, respaldadas por iniciativas gubernamentales, que supusieron mejoras para los consumidores españoles. Si bien la mayor penetración de la fibra y el 5G han impulsado año tras año notables avances en el rendimiento general de la red, la competitividad internacional de España en telecomunicaciones sigue estando muy desequilibrada entre su infraestructura fija y móvil.

Las credenciales del país como líder europeo en fibra permanecen intactas. En 2024, según la última edición del informe ‘Estado de la Década Digital’ de la Comisión Europea, España se situó entre los tres primeros países de la UE en cobertura de fibra hasta las instalaciones (FTTP), con un 95,21%, y en porcentaje de suscripciones de banda ancha fija con velocidades de descarga superiores a 100 Mbps (93,54%). Esto posicionó al país significativamente por delante de algunas de las economías más grandes del bloque, en particular Alemania, todavía rezagada en cobertura FTTP (28,80%).

Según Speedtest Intelligence la velocidad mediana de descarga fija en España aumentó de 173,32 Mbps a 210,46 Mbps entre 2023 y 2024. Esta tendencia de mejora se reflejó en otras métricas de rendimiento de la red fija, con velocidades medianas de carga que se incrementaron de 129.62 Mbps a 155.53 Mbps en el mismo período. En el tercer trimestre de 2024, DIGI alcanzó una velocidad mediana de descarga fija de 321,21 Mbps, por delante de Jazztel (273,18 Mbps), Orange (262,78 Mbps), Yoigo (255,74 Mbps) y Movistar (180,30 Mbps).

España lidera Europa en despliegue y adopción de fibra, con la mayor cobertura entre las 10 principales economías de la UE

Comisión Europea | DESI 2018-2024

Habiendo alcanzado niveles excepcionalmente altos de penetración de FTTP en áreas urbanas, suburbanas y rurales (que posicionan a España entre los tres primeros del índice DESI 2024 de la Comisión Europea sobre cobertura FTTP en zonas rurales escasamente pobladas), España está cambiando el foco hacia la mejora de la calidad de la experiencia (QoE) para casos de uso como los vídeojuegos y el streaming. A pesar de contar con más cobertura y tasas de aceptación FTTP, España está por debajo de países como Francia en el Índice Global de Speedtest de Ookla.

Este desequilibrio pone de relieve la influencia en el rendimiento de la banda ancha fija de factores como la tecnología Wi-Fi (Francia tiene una mayor penetración de Wi-Fi 6 y 7 en los router proporcionados por los operadores) y las velocidades ofrecidas en la tarifa (con una mayor proporción de clientes de fibra suscritos a planes multi-gigabit en Francia).

El sólido rendimiento de la velocidad de descarga fija de DIGI en España, detallado en Informe de Conectividad de Speedtest, está respaldado por factores favorables similares. Fue el primero en comercializar en España un servicio de 10 Gbps, aprovechando al máximo su infraestructura de fibra XGS-PON. Con precios altamente competitivos (desde sólo 20€ al mes por 1 Gbps y 25€ por 10 Gbps y router Wi-Fi 6 incluido), DIGI se ha asegurado rápidamente una cuota importante de conexiones con capacidad multigigabit en el mercado español.

Las comunidades autónomas del norte de España, líderes en rendimiento de velocidad de descarga fija

Speedtest Intelligence® | 2024

Además de evidenciar la importancia de un router moderno y velocidades más altas, el negocio de DIGI ejemplificó el año pasado la acelerada tendencia de consolidación en el fragmentado y sobredimensionado mercado español de fibra. La adquisición de la infraestructura de fibra de DIGI por parte de un consorcio liderado por Macquarie, que consolidó el estatus de Onivia como la mayor red FTTP ‘neutra’ en España, coincidió con otros acontecimientos como la escisión de BlueVia de Telefónica, la aparición de MásOrange y las alianzas de ‘FibreCo’ de Vodafone con Telefónica y MásOrange.

Como se observa en otros mercados europeos con un importante despliegue de fibra (como Reino Unido), la consolidación es un proceso lento y desafiante. Sin embargo, los operadores españoles continúan persiguiéndola para mejorar la rentabilidad de sus inversiones en fibra en áreas urbanas altamente edificadas, liberando recursos para aprovechar el crecimiento futuro en áreas rurales donde la superposición de infraestructura es menos común. Esto comienza con la absorción de pequeños operadores locales (de los que hay cientos) por “consolidadores locales”. Luego, éstos se integran en las carteras de infraestructura de los consolidadores regionales, lo que en última instancia conduce a la adquisición por parte de uno de los actores tradicionales más grandes.

El despliegue de fibra por parte de actores más pequeños como DIGI impulsa el cambio en la cuota de mercado de los operadores tradicionales

Análisis de datos de CNMC | 2022-2024

Esta consolidación gradual está modificando el negocio de la fibra en España, mientras que los operadores tradicionales separan sus unidades de infraestructura y servicios para apoyar el crecimiento de la oferta mayorista. Este año se podrá saber si un tercer actor consolidado puede competir y coexistir con éxito a largo plazo con Telefónica y MásOrange.

MásOrange compite por el liderazgo de la red en España, apoyándose en una importante ventaja de espectro

La consolidación también ha afectado al mercado móvil español. A finales del año pasado, la Comisión Europea aprobó la creación de una empresa conjunta entre MásMóvil y Orange. La fusión ha llevado a la recién formada MásOrange a una posición de liderazgo, tanto en suscripción como en cuota de espectro. Para obtener la aprobación de Bruselas, la entidad se comprometió a vender 60 MHz de espectro, incluidos 20 MHz en la banda de 3,5 GHz, para facilitar la entrada de DIGI como un operador móvil independiente de pleno derecho, convirtiendo así el mercado español en una estructura de cuatro actores.

Además de diversificar su cartera de marcas a través de la fusión (con Orange y Yoigo en el segmento premium, Jazztel y MásMóvil centrándose en la relación calidad-precio y Euskaltel y Telecable atendiendo las necesidades locales), MásOrange espera que sus activos de espectro le permitan alcanzar el liderazgo en el mercado móvil español.

Los ingresos de Movistar se mantienen estables interanualmente en el 3T de 2024 mientras que Vodafone y MásOrange afrontan caídas

Análisis de datos de mercado de CNMC | 2022-2024

La red de la entidad se basará principalmente en la infraestructura de Orange, complementada con la cartera de sites existentes de MásMóvil y el despliegue de nuevos. La integración de la red de MásMóvil, que depende íntegramente del espectro de banda media y alta e históricamente ha dependido de un acuerdo de roaming nacional con Orange, crea una sinergia para la entidad: aprovechar la capacidad y densidad de MásMóvil en áreas urbanas junto con la amplia cobertura y alcance nacional de Orange.

MásOrange está centrado en desbancar a Movistar en el segmento premium, que ha liderado durante mucho tiempo gracias a su foco en la calidad superior de la red. Movistar emergió como el operador móvil más rápido del mercado español en el Informe de Conectividad Speedtest de Ookla para el primer semestre de 2024, al ofrecer la velocidad de descarga media más alta de 82,68 Mbps. Esto sitúa a Movistar muy por delante de Orange (56,42 Mbps) y Yoigo (36,73 Mbps).

La ventaja espectral de MásOrange se inclina hacia las bandas medias y altas, normalmente utilizadas para implementaciones 5G en áreas urbanas y suburbanas. De acuerdo con los datos publicados por la compañía, MásOrange cuenta con el 37% de todos los activos de banda media y alta de España (en comparación con el 28% y el 26% de su competidor más cercano, Telefónica), lo que le da una oportunidad única de mejorar el rendimiento de la velocidad 5G y adelantarse a sus competidores.

Movistar ha mantenido su liderazgo en velocidad 5G con una asignación de 100 MHz en la banda de 3,5 GHz, pero esto se ve ahora eclipsado por la asignación de MásOrange de 170 MHz. La inversión de ésta para actualizar la RAN 5G para que cuente con capacidades avanzadas de agregación de operadores y arquitectura independiente (SA), le permitirá aprovechar los beneficios de rendimiento de un ancho de banda mayor a través del amplio despliegue de su espectro de 3,5 GHz en toda su red móvil consolidada.

Sevilla lidera en velocidad de descarga 5G entre las principales ciudades de España, pero el rendimiento de los operadores varía ampliamente

Speedtest Intelligence® | Q3 2024

Sin embargo, para liderar en cobertura de red, MásOrange necesitará ir más allá de su ventaja de espectro y centrarse en incrementar el número de sites físicos en áreas rurales. En el tercer trimestre de 2024, Vodafone y Movistar registraron en el mercado español una disponibilidad 4G del 95,1% y 93,4% respectivamente, seguidas de Orange con un 92,7% y Yoigo con un 91,5%.

Paralelamente a la consolidación de la red de MásOrange, DIGI está construyendo su propia infraestructura para dejar de depender gradualmente de un acuerdo de roaming y del uso compartido de RAN con Telefónica, comenzando con zonas urbanas y suburbanas. La Comisión Europea diseñó los remedies de desinversión de espectro para que DIGI replique la presión competitiva ejercida anteriormente por MásMóvil. El objetivo es que DIGI transporte una proporción similar de su tráfico total de datos móviles en su propia red en los próximos años, al menos igualando la cuota on-net del 40-60% que MásMóvil lograba antes de la fusión.

Provincias rurales de España, a la zaga en disponibilidad de 5G, lo que destaca la importancia del apoyo gubernamental a través de UNICO.

Speedtest Intelligence® | Disponibilidad general 5G (%) en 2024

En términos generales, se espera que los compromisos de inversión a largo plazo de DIGI y MásOrange, impulsados por la consolidación, unidos al apoyo gubernamental con programas como Único, impulsen la competitividad internacional de España en rendimiento móvil en los próximos años. El país tiene mucho por hacer, ya que a finales de 2024 ocupa el puesto 57 en Índice Global de Speedtest, situándose por detrás de la mayoría de sus colegas europeos en rendimiento de red, incluidas velocidad de descarga, coherencia y cobertura.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

Luke Kehoe leads Ookla’s research and thought leadership efforts in Europe.

An electronic engineering alumnus of University College Dublin, Luke has extensive experience collaborating with mobile operators, telecoms vendors, and government agencies in research and advisory roles across Europe. He has contributed to internationally recognised thought leadership publications in areas such as 5G, IoT, open RAN, and edge computing, working with prestigious organisations like the Telecom Infra Project and the World Economic Forum.

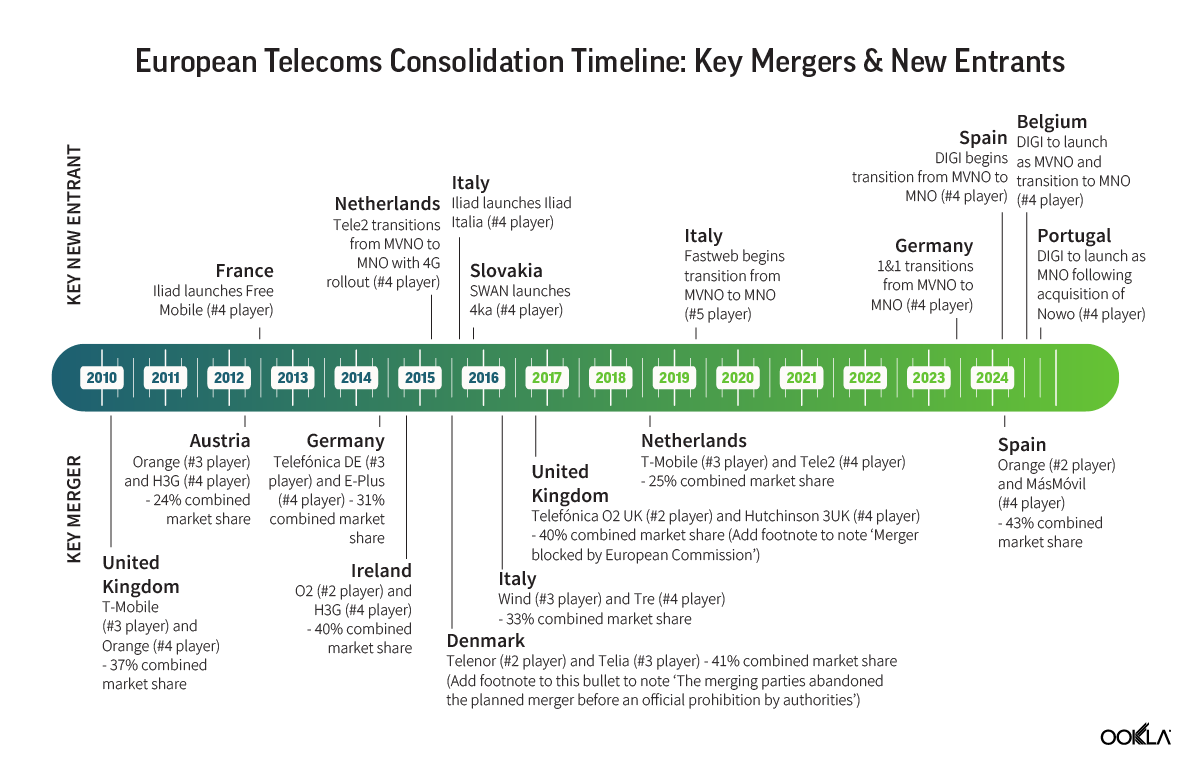

MarioDraghi has flirted with a radical restructuring of Europe’s telecoms market, seeking to cultivate pan-European scale and reinvigorate innovation and investment in telecoms. But is consolidation the answer?

Europe’s telecoms sector is at an inflection point. After a decade of stagnant revenues, lacklustre innovation and fierce competition, policymakers in Brussels are scrutinising the fundamental structure of the market. Earlier this year, a landmark report by Mario Draghi reignited discussions on consolidation, championing the creation of pan-European operators and calling for a decisive regulatory shift from proactive competition oversight (ex ante) to a reactive focus on enforcement after issues arise (ex post).

The proposed shift in policy comes as concerns over Europe’s telecoms sector’s ability to compete on a global stage reach a crescendo. A central tenet of the Draghi report is that the bloc’s fragmented telecoms market—a morass of dozens of small operators compared to just a handful in similarly sized regions elsewhere—has triggered a race to the bottom in pricing, eroding profitability and leaving Europe ill-equipped to compete with the more unified and dynamic markets of North America, the Middle East and Asia.

Mobile network quality is a key factor in the European telecoms competitiveness equation, shaping both consumer satisfaction and the bloc’s attractiveness for investment. Proponents of consolidation argue that fewer, larger operators could enhance network performance and better position the bloc to achieve the European Commission’s ambitious Digital Decade 2030 goals. The simple argument is that by cultivating market dynamics that prioritise service quality over price wars, consolidation would create stronger incentives for investment in capital-intensive mobile networks.

Critics, however, challenge this narrative that favours consolidation. Instead, they argue that network quality is not solely a function of market concentration or structure and emphasise that other factors such as pricing also play an important role in shaping Europe’s overall telecoms competitiveness. In contrast to Draghi’s position, they propose that similar outcomes could be achieved without reducing competition by deploying other policy tools, such as providing targeted funding for infrastructure rollouts or incentivising network sharing initiatives.

This white paper aims to provide independent, informed insights to support the ongoing policy discourse in Europe. It explores whether empirical evidence supports the arguments for and against consolidation in the bloc’s telecoms sector, analysing network quality, investment and pricing outcomes across the EU and a sample of other high-income countries to assess the impact of varying market structures (e.g., three or four players) and levels of market concentration.

Key takeaways

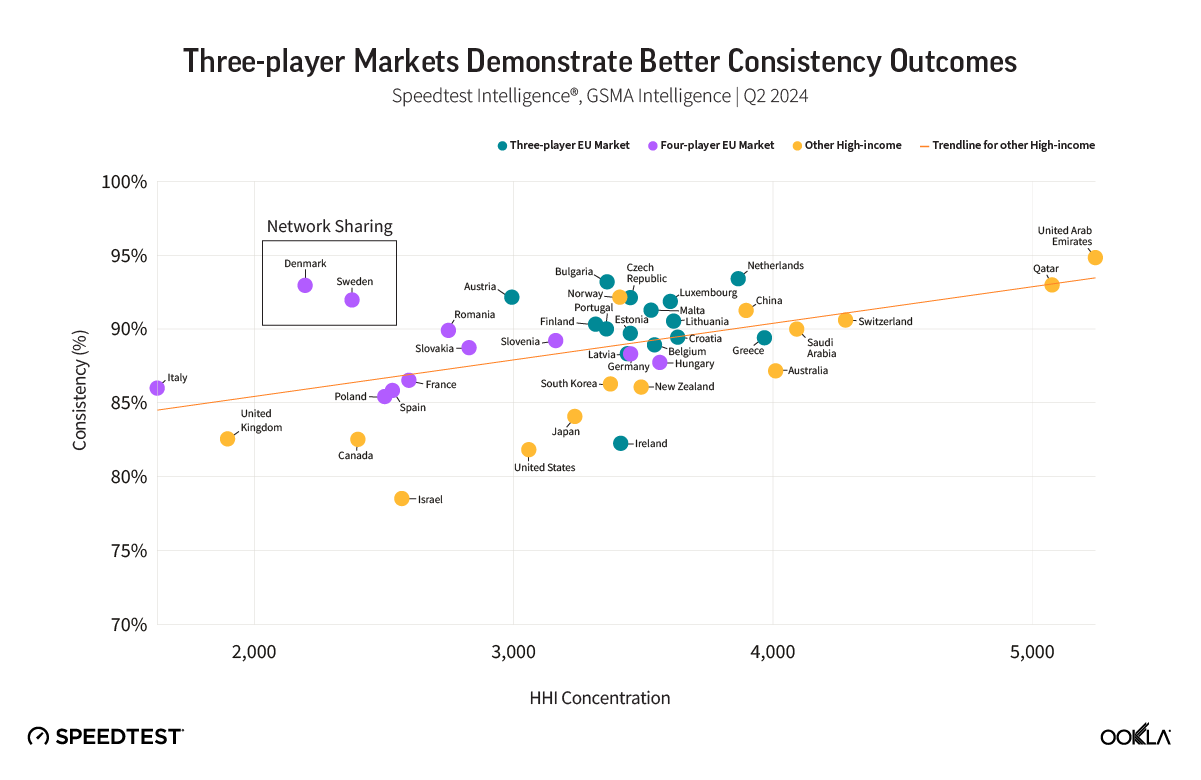

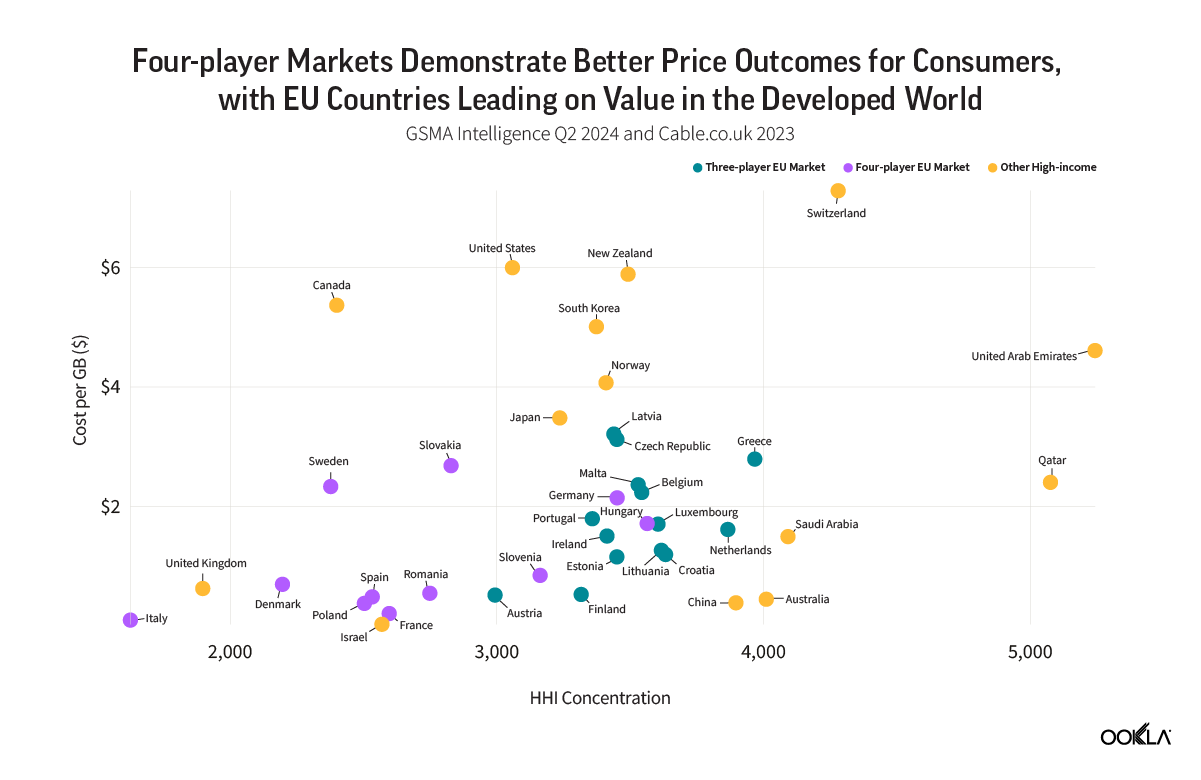

Three-player mobile markets in the EU and other high-income countries exhibit better network performance and consumer sentiment outcomes.

This trend is consistent across all technologies and at similar levels of market concentration. Among the top ten European countries ranked by median download speed in Q2-Q3 2024, seven are three-player markets. The other three — Denmark, Sweden, and France — are four-player markets where operators engage in network sharing, whether in spectrum, site infrastructure or multi-operator core networks. This suggests that the level of network sharing in these countries is more extensive than in most other four-player markets. Overall, the studied three-player markets in the EU delivered median download speeds that were 56% higher than those in four-player markets during Q2-Q3, according to Speedtest Intelligence® data.

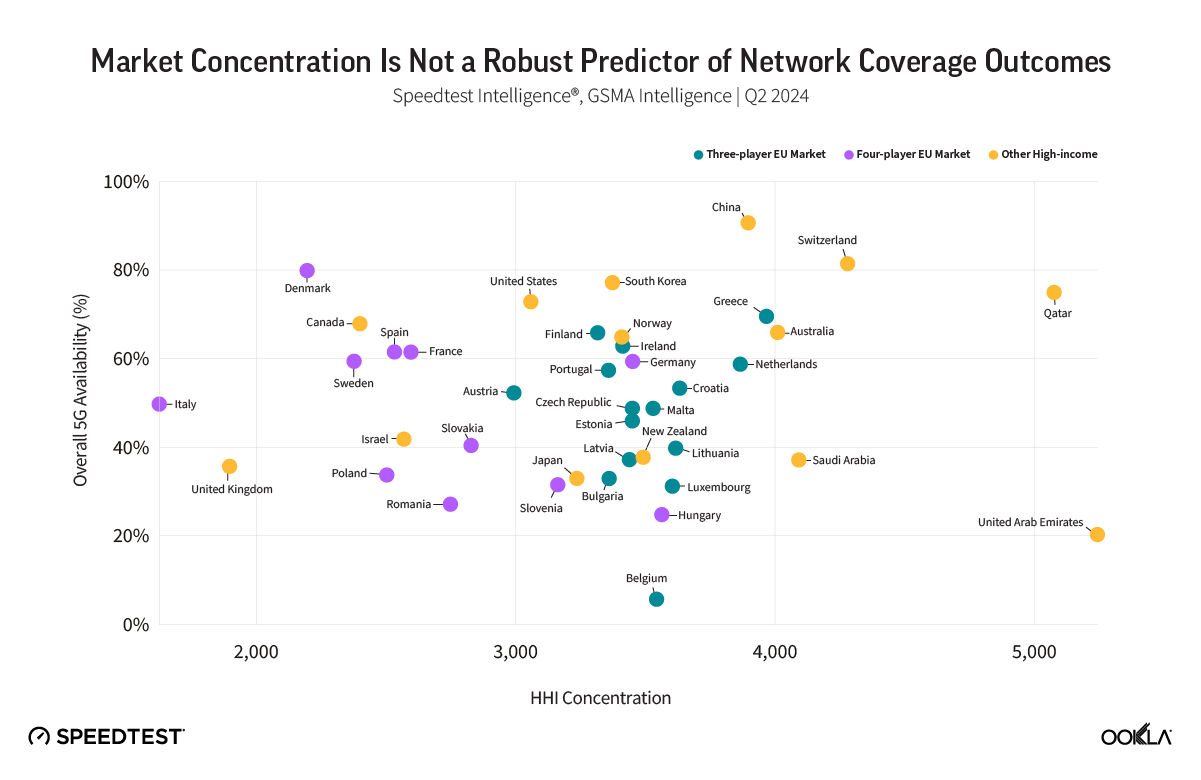

Market concentration is not a robust predictor of 5G coverage outcomes.

Socio-economic factors such as population distribution and economic development impart a greater impact on metrics relating to overall network reach, with wealthier, more urbanised countries enjoying investment conditions that are more conducive to the attainment of very high levels of service coverage and network availability. In four-player markets, however, disparities in overall 4G availability between the best- and worst-performing operators tend to be more pronounced than their three-player counterparts.

Intense price-based competition leads to markedly lower mobile data pricing outcomes in four-player markets over time.

The median consumer cost per gigabyte in highly concentrated markets — often seen in countries with the three-player structure — is nearly five times higher than in low-concentration markets. In four-player, lower-concentration markets, depressed ARPU and higher median capital intensity may result more from limited absolute revenues constraining reinvestment than from increased competition spurring greater investment. Conversely, in some highly concentrated non-EU high-income countries, greater market concentration is associated with lower capital intensity per operator, as larger players may face reduced incentives to invest.

There is no one-size-fits-all concentration profile that uniformly optimises network quality and consumer pricing outcomes in every country.

Exceptional outcomes in countries such as Denmark — a four-player market with low concentration but very high median download speed — and the Netherlands — a three-player market with high concentration and also high median download speed — suggest a targeted policy toolkit, rather than the blunt instrument of consolidation, is needed to achieve balanced outcomes across a bloc with highly diverse market contexts.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

Luke Kehoe leads Ookla’s research and thought leadership efforts in Europe.

An electronic engineering alumnus of University College Dublin, Luke has extensive experience collaborating with mobile operators, telecoms vendors, and government agencies in research and advisory roles across Europe. He has contributed to internationally recognised thought leadership publications in areas such as 5G, IoT, open RAN, and edge computing, working with prestigious organisations like the Telecom Infra Project and the World Economic Forum.

Poland Races to Regain 5G Competitiveness in Europe with Mid-Band Rollout | Polska galopuje do odzyskania konkurencyjności 5G w Europie dzięki wdrożeniu średniego pasma częstotliwości

Poland’s operators are rapidly deploying mid-band 5G in an attempt to capture the growing premium market segment

Late to the game in staging a mid-band auction, Poland has lagged behind its European peers in 5G deployment in recent years. This delay has weighed on the country’s global competitiveness in mobile network performance and slowed its progress toward meeting the European Commission’s flagship 5G deployment targets, which require universal 5G coverage across every EU member state by the end of the decade. This article examines the state of Poland’s mobile market and its broader regional 5G competitiveness in the context of ongoing mid-band deployments. A follow-up report will assess the longer-term impact of the commercialization of the recently awarded low-band spectrum and ongoing network sunsets on network coverage and availability.

Key Takeaways:

Intensive capital spending on mid-band deployment drives substantial uplift in 5G performance across Polish operators from Q1 2024, pushing the country ahead of regional peers over the last year.Median 5G download speeds in Poland jumped by over 50% to 160.30 Mbps between Q1 2024 and Q1 2025, based on Speedtest Intelligence® data, propelling the country ahead of Czechia, Romania, and Slovakia for the first time in 5G performance. Despite this progress, Poland continues to trail its regional peers in 5G network Consistency, a measure of how reliably a mobile connection remains “fast enough” for normal use.

T-Mobile and Orange surpass Play and Plus in speed and select Quality of Experience (QoE) measures. Differences in how quickly and extensively Polish operators have deployed their mid-band spectrum assets have led to a diverging market profile since Q1 2024, with T-Mobile and Orange significantly extending their speed lead over their rivals. Between Q1 2024 and Q1 2025, median 5G download speeds rose by as much as 72% on Play (to 122.64 Mbps), 86% on T-Mobile (to 201.76 Mbps), and 90% on Orange (to 222.10 Mbps)—while declining by over 10% on Plus (to 116.76 Mbps).

Network investments have broadened 5G coverage in Poland, but significant regional disparities remain. Nationally, 5G availability rose from 28.5% in Q1 2024 to 43.1% in Q1 2025, driven by continued Dynamic Spectrum Sharing (DSS) rollouts and the activation of mid-band spectrum—placing the country ahead of regional peers Bulgaria, Romania, and Hungary in 5G availability. Nonetheless, by Q4 2024, a pronounced coverage gap persisted between the country’s best- and worst-served provinces, with 5G availability in the populous Masovian Voivodeship (47.2%) double that of the Lubusz Voivodeship (23.6%).

Over the last year, Polish operators have been locked in an intense four-way race to catch up with their regional peers in 5G deployment, driven by stringent coverage obligations imposed by the Polish telecoms regulator (UKE), a wave of funding support from Brussels, and a growing push to compete for a larger share of the country’s widening premium market segment, where network performance has emerged as a key competitive differentiator.

Poland’s mobile market is today awash with deployment activity, as operators ramp up capital spending to the highest levels in years to equip thousands of mobile sites with mid-band spectrum, accelerate the sunset of 3G networks, and lay the groundwork for launching 5G standalone (SA) in the coming years. This flurry of activity follows the completion of the 700/800 MHz auction at the end of March this year, where all Polish operators secured low-band 5G spectrum for the first time—paving the way for improved rural and deep in-building 5G coverage and rounding out the country’s 5G spectrum release plans.

While 5G capital spending has slowed across much of Europe, Poland sees different dynamics due to late spectrum auctions

Poland was notably late in releasing dedicated 5G spectrum in the ‘pioneer bands’ identified by the European Commission as critical to the timely commercialization and rollout of 5G across EU member states. The country’s mid-band (3.6 GHz) auction, initially planned for mid-2020, was repeatedly delayed—by more than three years—due to the pandemic and a protracted security legislation process.

These delays in spectrum availability have contributed to Poland’s divergence from much of the rest of Europe in both the economic and technical dimensions of the 5G rollout. Until recently, Polish mobile operators exhibited lower capital intensity (they invested less of their revenue) compared to peers in other European countries. Most of their spending went into upgrading 4G sites and preparing for the 3G shutdown, instead of building a new 5G mid-band capacity layer or expanding 5G coverage using low-band (700 MHz) spectrum.

Orange's Rising Mobile Capex Reflects 5G Network Expansion

Analysis of Orange Poland accounts | 2020 – 2024

Analysis of financial data published by Orange, Poland’s largest mobile operator by subscriber count, confirms that the era of lower capital intensity (relative to elsewhere in Europe) is over. The recent spectrum auctions have triggered a new cycle of investment, with Orange doubling its mobile network spending in the past three years. Play has also rapidly increased its investment, as its French parent Iliad reported injecting record amounts into Play’s mobile infrastructure last year.

Play's Contribution to Capex in the Iliad Group Surges as 5G Buildout Ramps Up

Analysis of Iliad Group accounts | 2020 – 2024

On the technical side, meanwhile, Poland’s spectrum delay meant that three of the country’s four operators were forced to rely heavily on Dynamic Spectrum Sharing (DSS)—a technology that allows 4G and 5G to operate on the same band and adjust ‘dynamically’ to demand—in an effort to deliver early 5G coverage in the 2100 MHz band while awaiting spectrum auctions. This strategy resulted in Poland’s initial 5G performance more closely resembling those typical of 4G networks, as DSS deployments are typically based on a 10 MHz carrier where part of the capacity is still reserved for 4G signals, making 5G speeds with DSS around 15–25 % lower than if the band were dedicated solely to 5G.

The limitations of using DSS to deliver a “5G experience” were exemplified by the speed advantage maintained by Plus earlier in the 5G rollout. Importantly, Plus was the only Polish operator that did not rely on DSS and instead dedicated a full 40 MHz carrier in the 2600 MHz (TDD) band to 5G before mid-band spectrum became available at the start of last year. Prior to the 3.5 GHz band coming online, when the other operators were still wholly dependent on DSS for 5G coverage, Plus’s median 5G download speed of 133.34 Mbps was as much as 77 % higher than T-Mobile’s, 81 % higher than Orange’s, and 92 % higher than Play’s.

Polish operators move from mid-band spectrum acquisition to mass commercial deployment in record time

The pent-up demand for mid-band spectrum in Poland was evident when mobile operators like Orange, T-Mobile, and Play launched commercial services just three months after acquiring mid-band spectrum, moving quickly from the auction in October 2023 to commercial launches by January 2024. T-Mobile reported that its mid-band 5G network already covered more than 25% of the Polish population by April 2024, with more than 2,100 sites active, while Orange announced it had reached 40% coverage by mid-June.

This rollout pace is exceptional by European standards and indicative of the increased pace of deployment possible later in the 5G technology cycle. It took Spain’s Telefónica (Movistar) about six months to reach its first 1,000 mid-band sites by comparison, and Germany’s operators needed around nine months to achieve the same milestone.

Plus's Spectrum Holdings in the 2600 MHz TDD Band Lend it a Decisive Capacity Lead

Each operator secured a contiguous 100 MHz block of spectrum in the 3.5 GHz band, which is widely regarded as optimal due to the large channel bandwidth this configuration affords. However, Plus has been notably slower to commercialise this allocation at scale. Plus’s earlier strategy of deploying 5G in the dedicated 2600 MHz band (rather than relying on DSS), alongside later using the 2100 MHz band as well, gave it more flexibility to delay a broad mid-band rollout as it previously enjoyed a significant 5G speed advantage over competitors while they were still heavily dependent on DSS deployments.

Mid-band deployment shifts 5G performance rankings among Polish operators

Mass deployment of a new capacity layer by the other three operators has since decisively altered performance dynamics in the Polish market and eroded Plus’s lead. In the space of one year between Q1 2024 and Q1 2025, Plus has moved from market leader in median 5G download speed to laggard, becoming the only Polish operator to see a year-on-year decline in 5G speed, down 10%, indicating the increasing limitations of its 2600 MHz strategy.

Orange and T-Mobile Pull Ahead in 5G Performance with Mid-Band Deployment

Speedtest Intelligence® | Q1 2023 – Q1 2025

By contrast, mid-band deployment has boosted performance across the rest of the market, with median 5G speeds rising by as much as 72% on Play, 86% on T-Mobile, and 90% on Orange between Q1 2024 and Q1 2025. While Orange led the Polish market in Q1 with a median 5G download speed of 222.11 Mbps, the operator’s lead has narrowed significantly as T-Mobile’s mid-band buildout has progressed, with T-Mobile now recording median 5G download speeds of 201.76 Mbps, well ahead of third- and fourth-placed Play (122.64 Mbps) and Plus (116.76 Mbps), respectively.

Plus's Lead in 5G Consistency Narrows as 2600 MHz Advantage Recedes with Mid-Band Deployment

Speedtest Intelligence® | Q1 2023 – Q1 2025

Despite losing its lead in median 5G download speed, Plus continues to lead at the 10th percentile (29.44 Mbps in Q1 2025), meaning subscribers in its lowest-performing areas still enjoy comparatively better speeds than those on rival networks. This advantage is likely linked to Plus’s lower dependence on DSS. However, T-Mobile (24.48 Mbps) and Orange (21.88 Mbps) are quickly closing the gap, with their 10th percentile 5G speeds now converging toward Plus. Plus’s 5G network consistency, measured as the proportion of Speedtest samples meeting a minimum download and upload threshold of 25/3 Mbps, has also declined over the past year, although it remains the market leader.

On upload performance, meanwhile, Play’s 5G network led the market in Q1 2025, recording median speeds of 19.33 Mbps, followed by Orange (18.99 Mbps), T-Mobile (17.32 Mbps), and Plus (14.96 Mbps). Unlike the substantial gains seen in download speeds, there is limited evidence so far that the mid-band rollout has materially improved upload performance, with median upload speeds about 6% lower in Q1 2025 compared to the same quarter last year. This discrepancy arises primarily because all four operators continue to deploy 5G in non-standalone (NSA) mode, requiring devices to transmit uplink traffic via existing 4G anchor bands. Consequently, the newly available 3.5 GHz spectrum enhances downlink capacity but leaves the congested 4G uplink path unchanged.

Play Develops Lead in 5G Upload Performance

Speedtest Intelligence® | Q1 2023 – Q1 2025

The operators’ investments in deploying a new 5G capacity layer have coincided with a broader RAN refresh effort, translating into improved quality of experience for users in key use cases such as video streaming and web browsing. Median web page load times on T-Mobile’s network, for instance, improved by around 4% between Q3 2024 and Q1 2025. Orange led in video metrics such as start time, resolution, and uninterrupted playback in the last quarter.

5G Drives QoE Improvements in Use Cases like Web Browsing

Speedtest Intelligence® | Q1 2025

Capital investment expands 5G coverage, but Poland’s rural-urban digital divide persists

While investments in DSS and the mid-band rollout have enabled Polish operators to make significant strides in 5G availability, which increased nationally from 28.5% in Q1 2024 to 43.1% in Q1 2025, regional coverage disparities continue to be a feature of the mobile network experience in Poland. Operators have prioritized 5G deployments in the richest and densest parts of Poland where fiber is heavily deployed, including the Masovian (Warsaw) and Pomeranian (Tri-City) provinces. In these provinces, 5G availability reached more than 40% by the end of last year and contributed to driving materially higher median download speeds than the national average.

5G Availability Remains Highly Varied Across Poland Outside of Urbanized Areas

Speedtest Intelligence® | 5G Availability (%) in Q4 2024

By contrast, border provinces along the south and west of the country continue to experience much lower levels of 5G availability. Lubusz had the lowest availability (23.6% at the end of last year), where there is lower population density and lower subscriber spending, which reduces operators’ commercial incentives for widespread 5G investment. This trend has driven the development of a notable speed gap between provinces, with mobile subscribers in Lubusz also experiencing the lowest median download speeds (59.97 Mbps) in Poland, almost 33% below the leading Masovian province.

Mobile Download Speeds Are Lower in Less Urbanized Areas of Poland

Speedtest Intelligence® | Median Download Speed (Mbps) in Q4 2024

Mid-band deployment improves Poland’s mobile competitiveness, but 5G consistency continues to trail regional peers

From a regional competitiveness lens, intensive mid-band deployments have been successful in breaking Poland’s cycle of mobile network underperformance, with median 5G download speeds rising by over 50% on average to 160.30 Mbps between Q1 2024 and Q1 2025. This has propelled the country ahead of Czechia, Romania, and Slovakia for the first time in terms of 5G download speed performance.

Despite Poland’s progress on its mid-band 5G rollout, the lingering effects of reliance on DSS and limited 5G spectrum diversity—up until the recent 700/800 MHz auction—mean that Poland continues to trail its regional peers in terms of 5G network consistency. In Q1 2025, 82% of Speedtest samples in Poland met the minimum 5G performance threshold for a consistent mobile experience, compared to 86% in Hungary, 89% in Romania, and 93% in Bulgaria.

Poland’s previous reliance on DSS, driven by limited 5G spectrum diversity, likely contributed to its slower average revenue per user (ARPU) growth compared to neighboring countries in recent years. Polish operators initially introduced tariffs with “5G at no extra cost” bolted onto existing 4G bundles, keeping prices flat to defend market share (and thereby maintaining depressed ARPU levels relative to regional peers). Combined with the external shock induced by markedly higher energy prices, stagnant ARPU levels created challenging operating conditions in the Polish market and weighed on operator profitability.

Intense Priced-Based Competition Precipitated Revenue Erosion in Poland During the First Half of the 5G Cycle

Analysis of GSMA Intelligence Data | % Change in Mobile ARPU (Q1 2020 vs Q1 2023)

In neighboring markets, by contrast, operators were able to leverage mid-band spectrum deployments as both technical and marketing levers, shifting their strategies from price competition toward service-based differentiation. This enabled them to more effectively upsell premium speed tiers or monetize specific use cases, such as fixed wireless access (FWA), which dedicated mid-band 5G deployments uniquely support.

T-Mobile and Play Outpaced Rivals in Subscription Share Growth in Recent Years

Analysis of UKE Market Data | 2019 – 2023

Similarly, the delayed timing of Poland’s mid-band 5G auction likely dampened supply-side factors key for driving growth in mobile data traffic. Between Q1 2020 and Q4 2024, traffic volumes in neighboring Bulgaria converged with that in Poland for the first time, increasing by 4.8x vs. Poland’s 2.6x. Meanwhile, Bulgarian operators capitalized early on mid-band spectrum availability to aggressively promote competitive FWA solutions (a major driver of mobile traffic in developed markets) and to introduce cheap unlimited data tariffs with fewer usage restrictions.

Poland Maintains Regional Lead in Mobile Data Volumes, but Bulgaria is Catching Up

Analysis of GSMA Intelligence data | 2020 – 2024