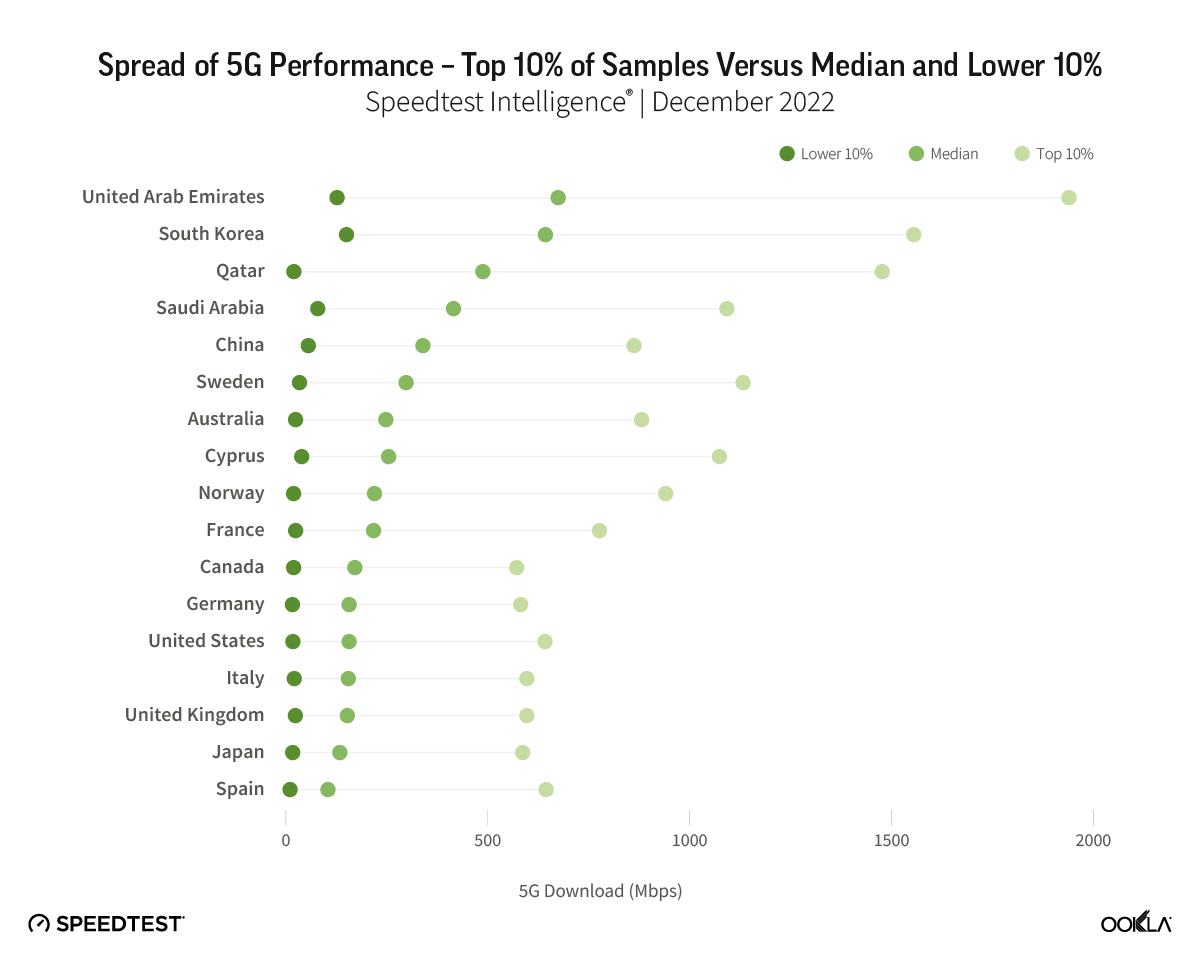

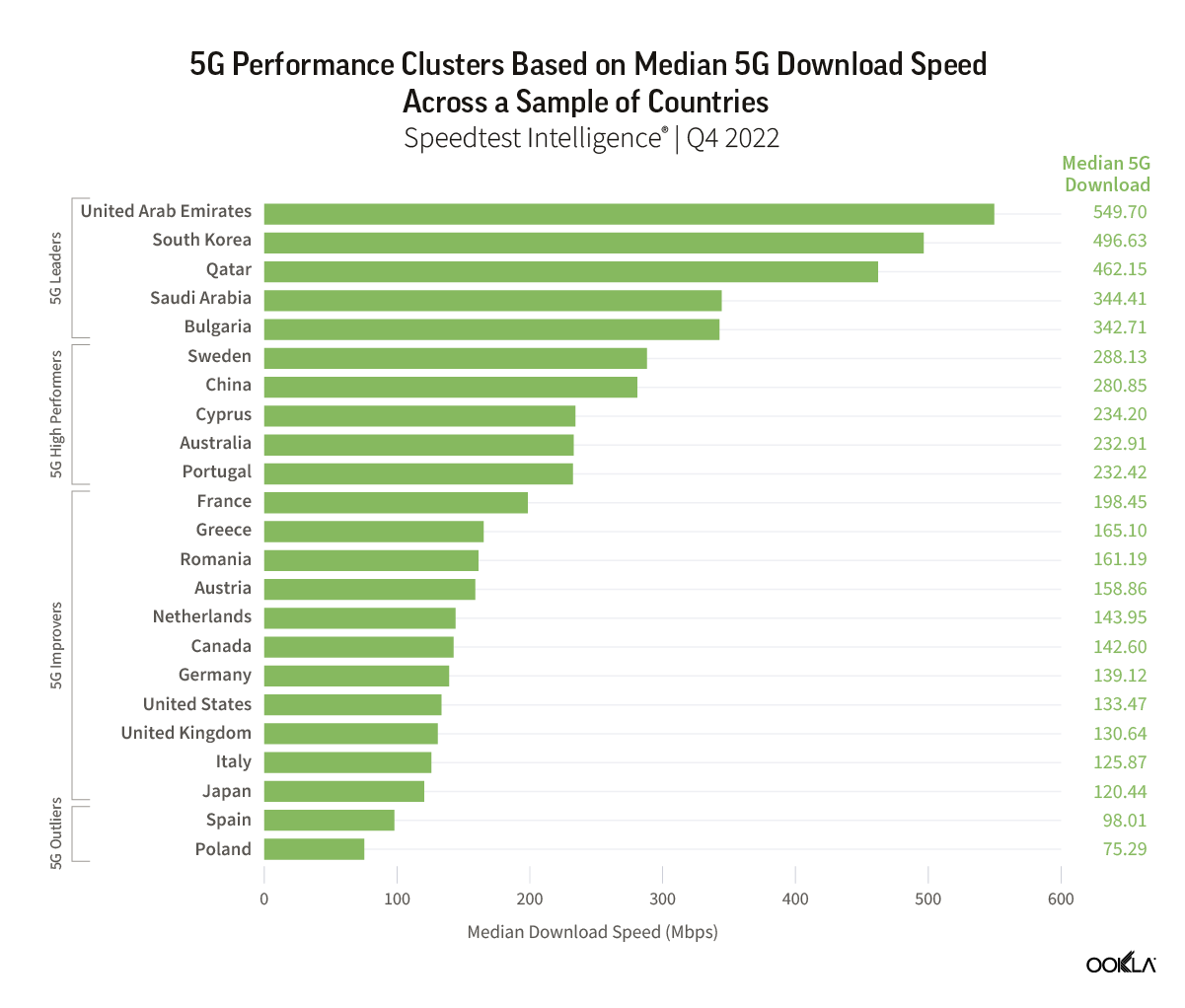

In-market 5G performance varies widely. Reviewing the top 10% and worst 10% of Ookla® Speedtest Intelligence® samples reveals significant variance in the consumer experience on today’s 5G networks, with 5G speeds peaking at over 1 Gbps for the top 10% of users in the U.A.E on average, but falling to below 20 Mbps for the lower 10% in Norway, the U.S., Japan, Germany, and Spain.

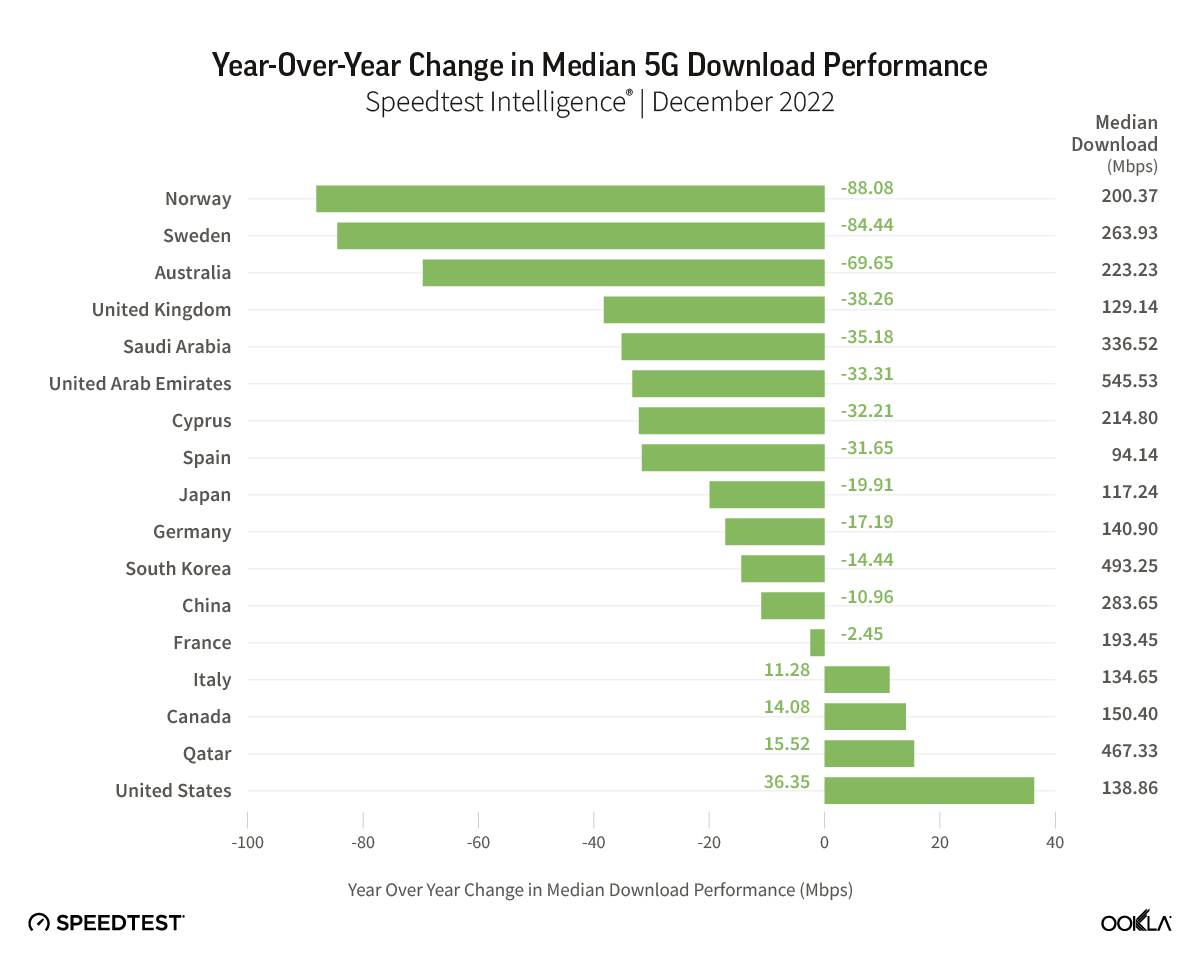

Median 5G performance is declining in many early launch 5G markets. While understandable as 5G adoption grows and users in more remote locations access 5G, declining median download speeds also point to investment and deployment challenges in some markets. At the same time, many of these markets are facing economic headwinds, placing more emphasis than ever on cost control. As a result, operators must carefully balance network investment priorities.

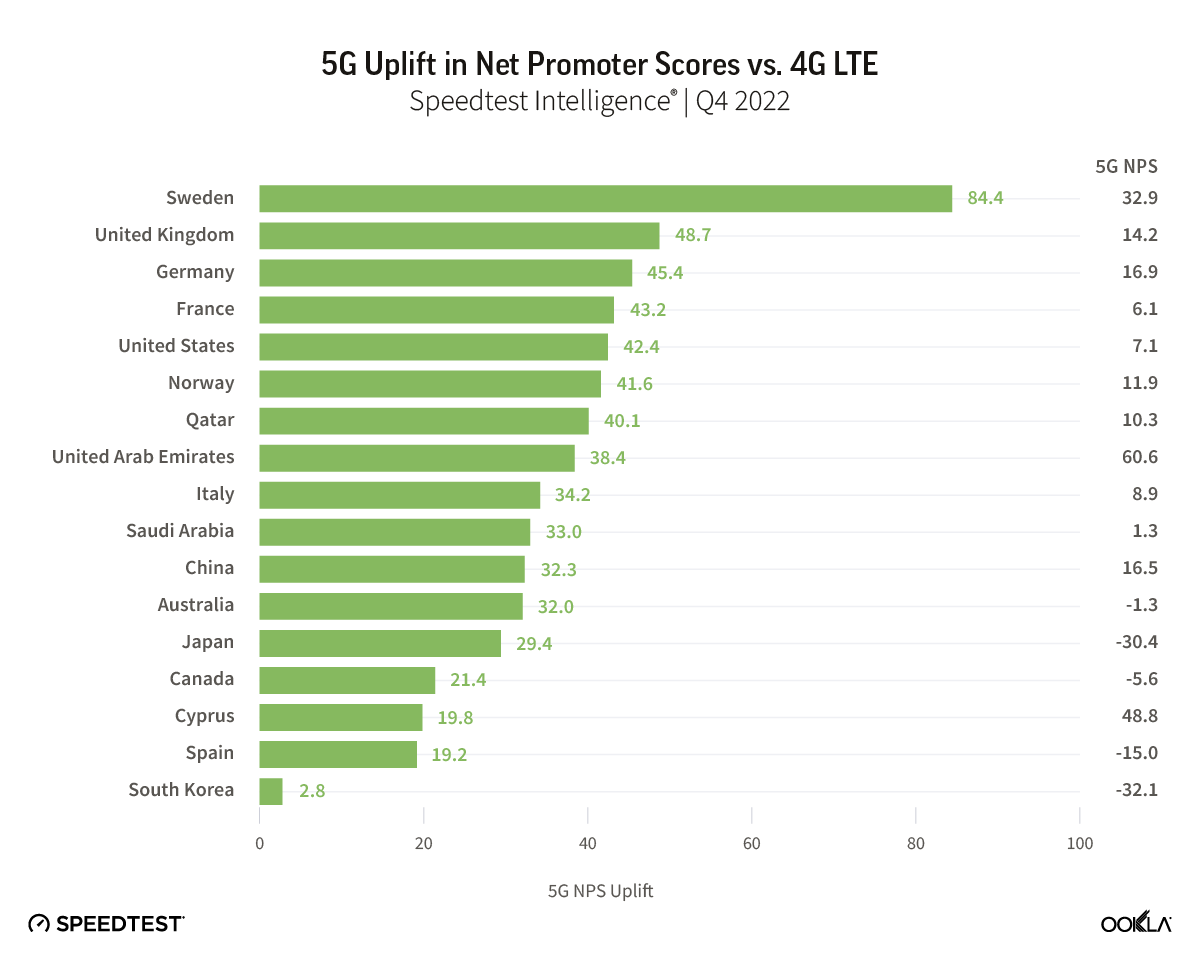

5G Net Promoter Scores (NPS) significantly higher than 4G LTE in most markets, but waning. With the exception of Sweden and Qatar, all the early launch 5G markets in our analysis saw 5G NPS fall year-over-year. Operators’ 5G NPS still trade at a premium compared to 4G, and while performance is just one part of the equation, operators should take care to build on the positive sentiment that 5G has brought to date.

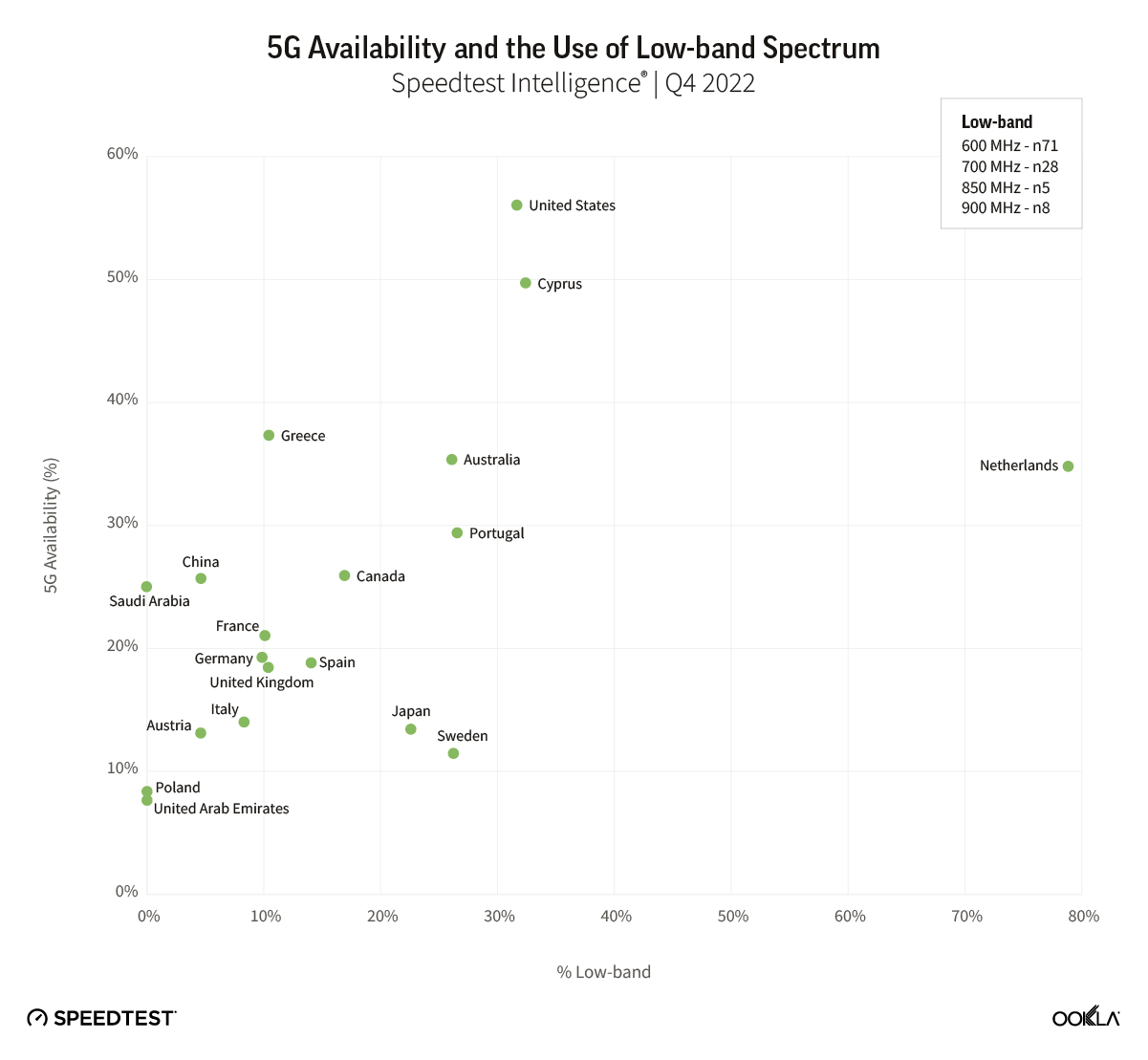

Despite impressive headline speeds, 5G performance varies a lot

Median 5G performance allows us to gauge the midpoint of user experience on 5G networks, however it doesn’t paint the full picture. While headline 5G speeds impress, Speedtest Intelligence data lays bare the ups and downs of 5G performance for consumers, even in early launch, advanced 5G markets. We recently looked at 5G network performance over high frequency (mmW) bands, painting a view of the true potential of 5G networks. However, if we look at performance on today’s 5G networks, looking beyond the median at the range of performance between users in the top 10% and those in the lower 10%, Speedtest Intelligence data reveals huge variance in the performance users experience.

The U.A.E. was the fastest 5G market in our analysis, based on median download performance of 545.53 Mbps in December 2022, followed by South Korea and Qatar. However, the top 10% of users in the U.A.E. recorded speeds of at least 1,266.49 Mbps on average, while the lowest 10% of users experienced speeds of 127.52 Mbps or slower on average. At the other end of the scale, Spain recorded a median 5G speed of 94.14 Mbps, but also demonstrated wide variance between the top 10% of samples at 537.95 Mbps or faster and the lowest 10% with 10.67 Mbps or less.

Based on many of the marketing messages around 5G, consumers are led to expect a big bang change in performance. However, with 5G operating over a greater range of spectrum bands than previous generations, including high frequency spectrum which has relatively poorer propagation, it’s understandable that 5G performance will vary more than previous generations of mobile network technology.

5G markets set to face performance challenges during 2023

While globally 5G speeds have remained stable, for many of the markets in our analysis, median 5G download speeds have fallen over the past year. The U.S. was the main outlier, recording the strongest uplift in 5G performance as T-Mobile continued to drive home its performance advantage in the market, while Verizon’s performance improved early in 2022 through its deployment of 5G in C-band spectrum. This trend is likely to continue in 2023 in the U.S., as more C-band spectrum is made available. However, the picture remains concerning for a number of other 5G markets, particularly those where median 5G speeds are at the lower end of the spectrum.

In some markets, 5G was initially priced at a premium to 4G, with operators focused on driving incremental returns on the new network technology. However, operators have been increasingly opening up 5G access by removing incremental costs for consumers and adding prepaid plans too. As 5G adoption scales, it places more strain on the new networks. The challenge for many of these markets is that network performance is likely to degrade further unless network densification picks up.

For network operators, this investment imperative is occuring amidst macroeconomic headwinds, which are driving up operating costs and putting pressure on consumer and enterprise spend. In addition, there remain challenges in deploying additional 5G cell sites in dense urban areas where demand is strongest, while in some markets EMF limits and other regulations can limit the deployment of high-capacity 5G sites.

Net Promoter Score (NPS) from Speedtest Intelligence paints a largely positive picture of current 5G networks. NPS is a key performance indicator of customer experience, categorizing users into Detractors (score 0-6), Passives (score 7-8), and Promoters (score 9-10), with the NPS representing the percentage of Promoters minus the percent of Detractors, displayed in the range from -100 to 100. Across the markets we analyzed, 5G users on average rated their network operator with NPS scores that were universally higher than those for 4G LTE users. However, consumer sentiment for users on 5G networks is beginning to shift, with NPS scores falling, coinciding with lower median 5G performance in many of the markets we analyzed.

Declining performance levels will be a factor driving NPS down for some 5G users. It’s also important to remember that as 5G scales in many of these early launch markets, the profile of 5G users is also changing from predominantly urban-based users, to more of a mix of urban, suburban, and rural users, which brings additional coverage and performance challenges for network operators. We plan to examine the relationship between 5G performance and spectrum in an up-coming content piece. Please get in touch if you’d like to learn more about Speedtest Intelligence data.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

5G continues to offer new and exciting ways of rethinking everything from streaming video to performing remote surgery. However, not everyone shares equally in these possibilities as many countries do not have access to 5G and even those that do, do not experience the same level of performance from their 5G connections. We examined Speedtest Intelligence® data from Q3 2021 Speedtest® results to see how 5G speeds have changed, where download speeds are the fastest at the country and capital level, where 5G deployments have increased and what worldwide 5G Availability looked like in Q3 2021. We also looked at countries that don’t yet have 5G to understand where consumers are seeing improvements in 4G access.

5G slowed down at the global level

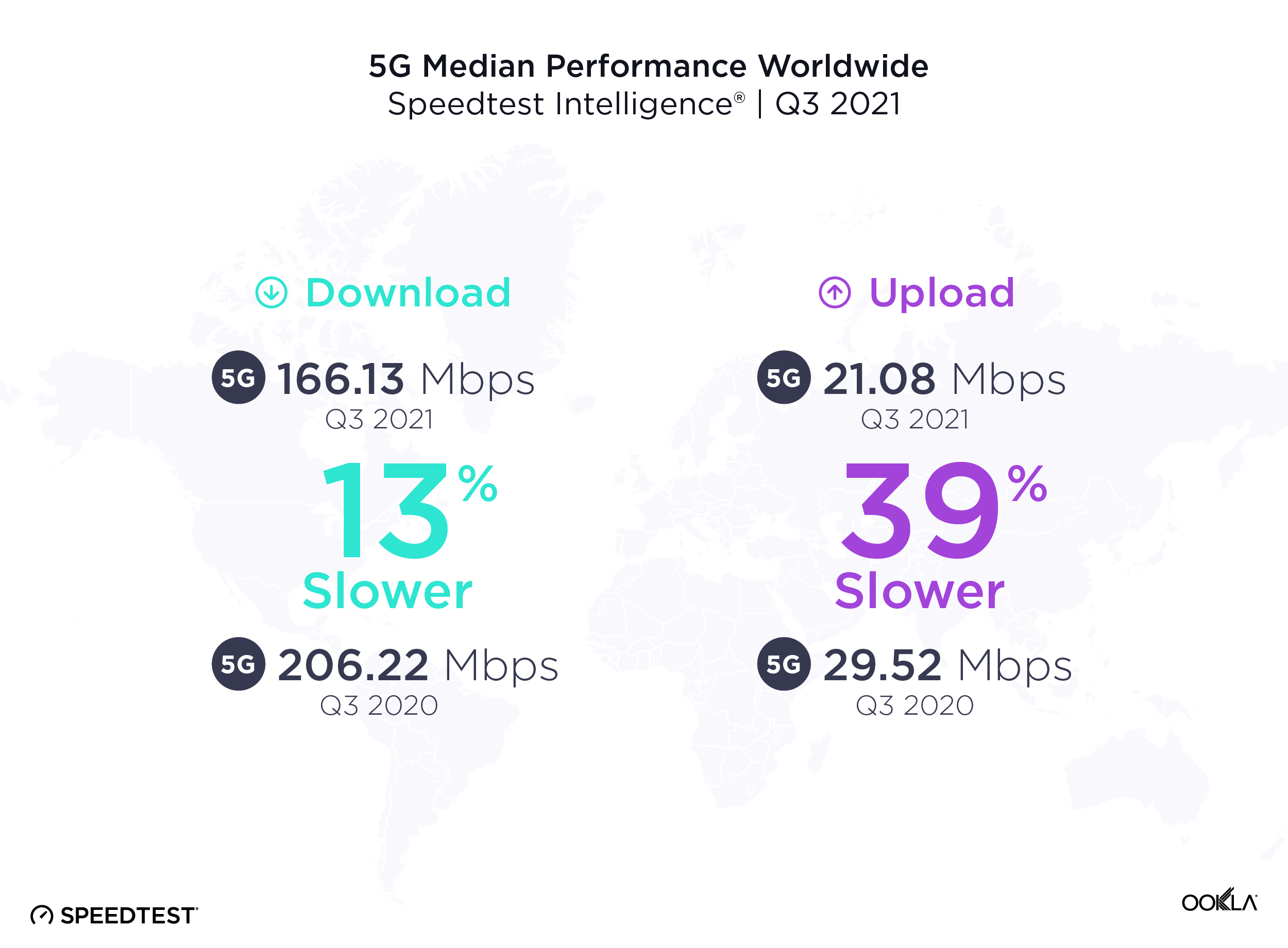

It’s common to see new mobile access technologies slow down as adoption scales, particularly early on in the tech cycle. Over the past year from Q3 2020 to Q3 2021, the median global 5G download speed fell to 166.13 Mbps, down from 206.22 Mbps in Q3 2020. Median upload speed over 5G also slowed to 21.08 Mbps (from 29.52 Mbps) during the same period.

More users are logging on to existing 5G networks, and we’re also at the stage in the evolution of 5G where countries that have historically had slower speeds are starting to offer 5G. In addition, the widespread use of dynamic spectrum sharing that has been used to boost early 5G coverage weighs on 5G download speeds. While the dip in speeds looks like a letdown, it’s more of a compromise to enable broader access. With additional spectrum and further deployments slated for 2022, we anticipate speeds will begin to pick up again.

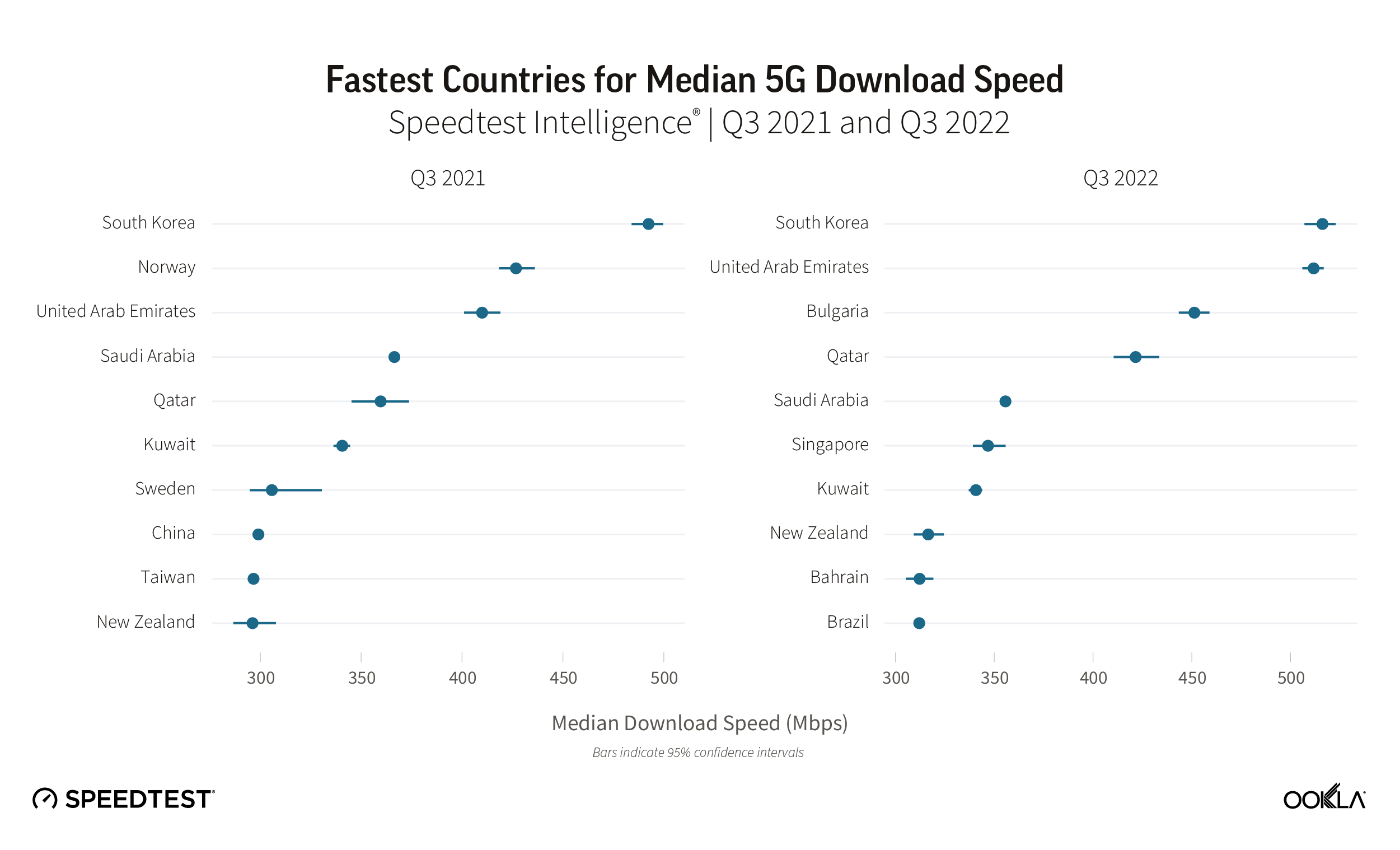

South Korea had the fastest 5G in the world

South Korea had the fastest median download speed over 5G during Q3 2021, leading a top 10 list that included Norway, United Arab Emirates, Saudi Arabia, Qatar, Kuwait, Sweden, China, Taiwan and New Zealand. Sweden, China, Taiwan and New Zealand were new to the top 10 in 2021 while South Africa (whose 5G was brand new last year), Spain and Hungary fell out of the top 10.

5G expanded to 13 additional countries

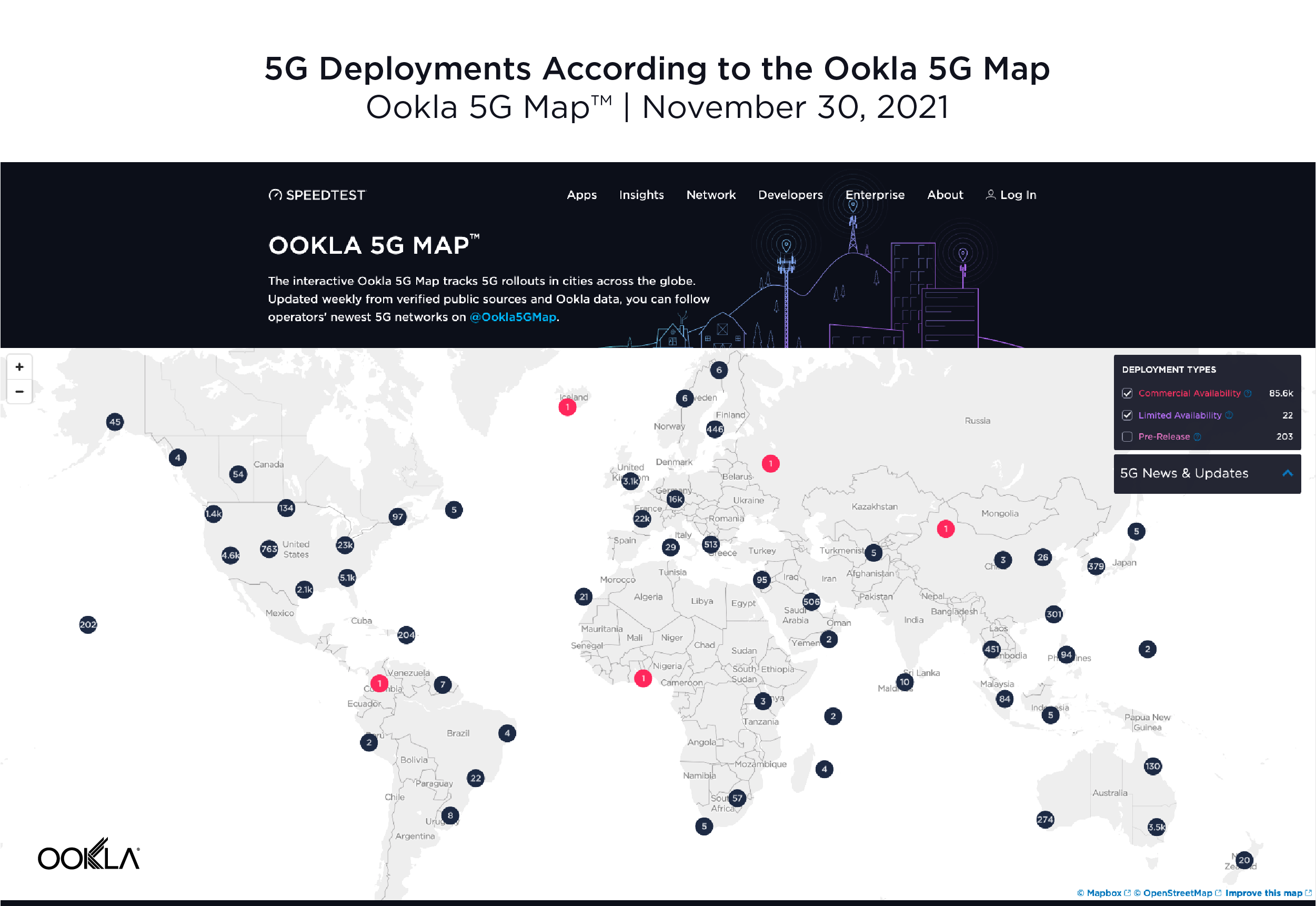

According to the Ookla® 5G Map™, there were 5G deployments in 112 countries as of November 30, 2021. That’s up from 99 countries on the same date a year ago. The total number of deployments increased dramatically during the same time period with 85,602 deployments on November 30, 2021 compared to 17,428 on November 30, 2020, highlighting the degree to which 5G networks scaled during the year. Note that there are often multiple deployments in a given city.

Seoul and Oslo lead world capitals for 5G

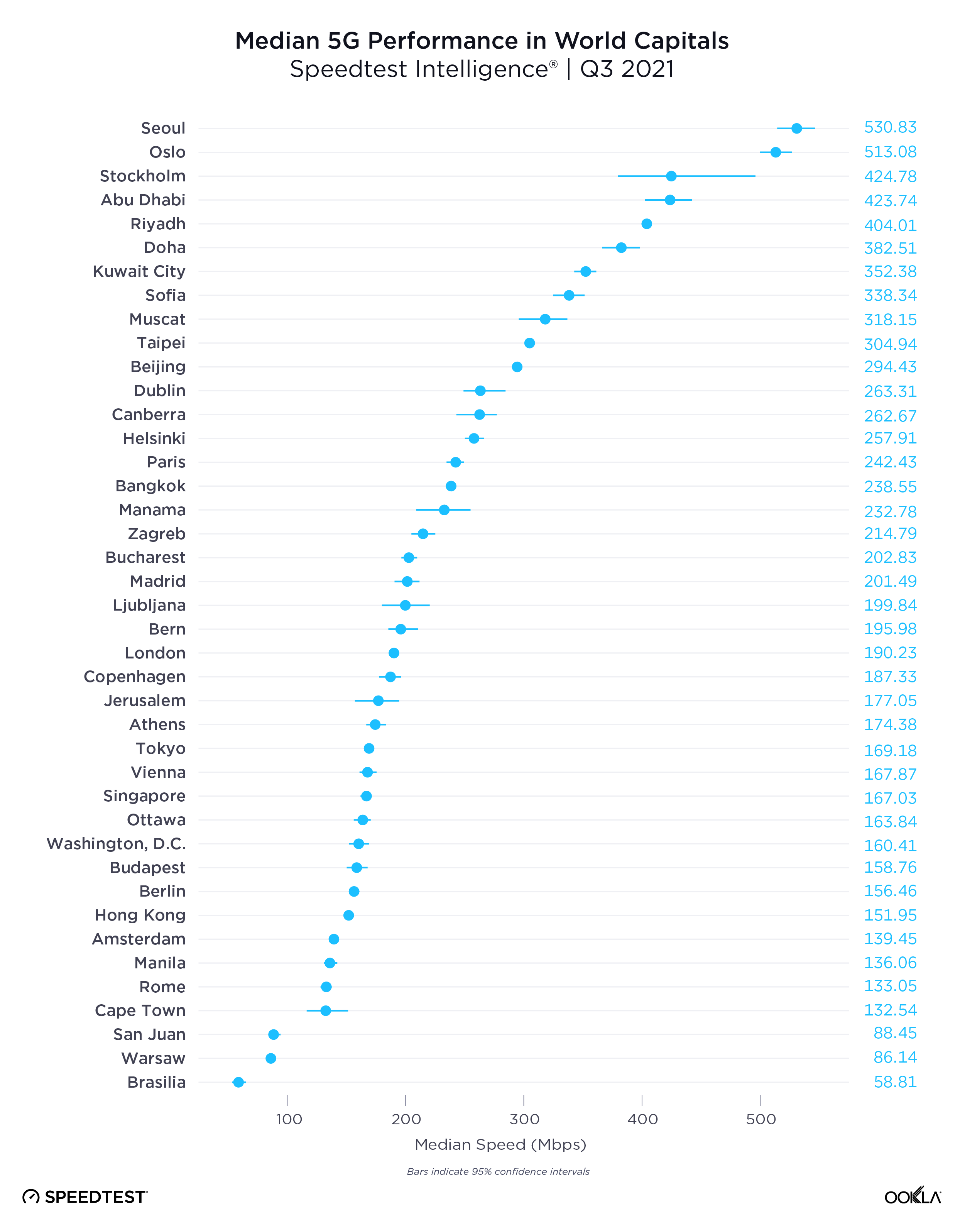

Speedtest Intelligence data from Q3 2021 shows a wide range of median 5G speeds among global capitals. Seoul, South Korea and Oslo, Norway were in the lead with 530.83 Mbps and 513.08 Mbps, respectively; Abu Dhabi, United Arab Emirates; Riyadh, Saudi Arabia and Doha Qatar followed. Brasilia, Brazil had the slowest median download speed over 5G on our list, followed by Warsaw, Poland; Cape Town, South Africa and Rome, Italy. Stockholm, Sweden and Oslo, Norway had some of the the fastest median upload speeds over 5G at 56.26 Mbps and 49.95 Mbps, respectively, while Cape Town had the slowest at 14.53 Mbps.

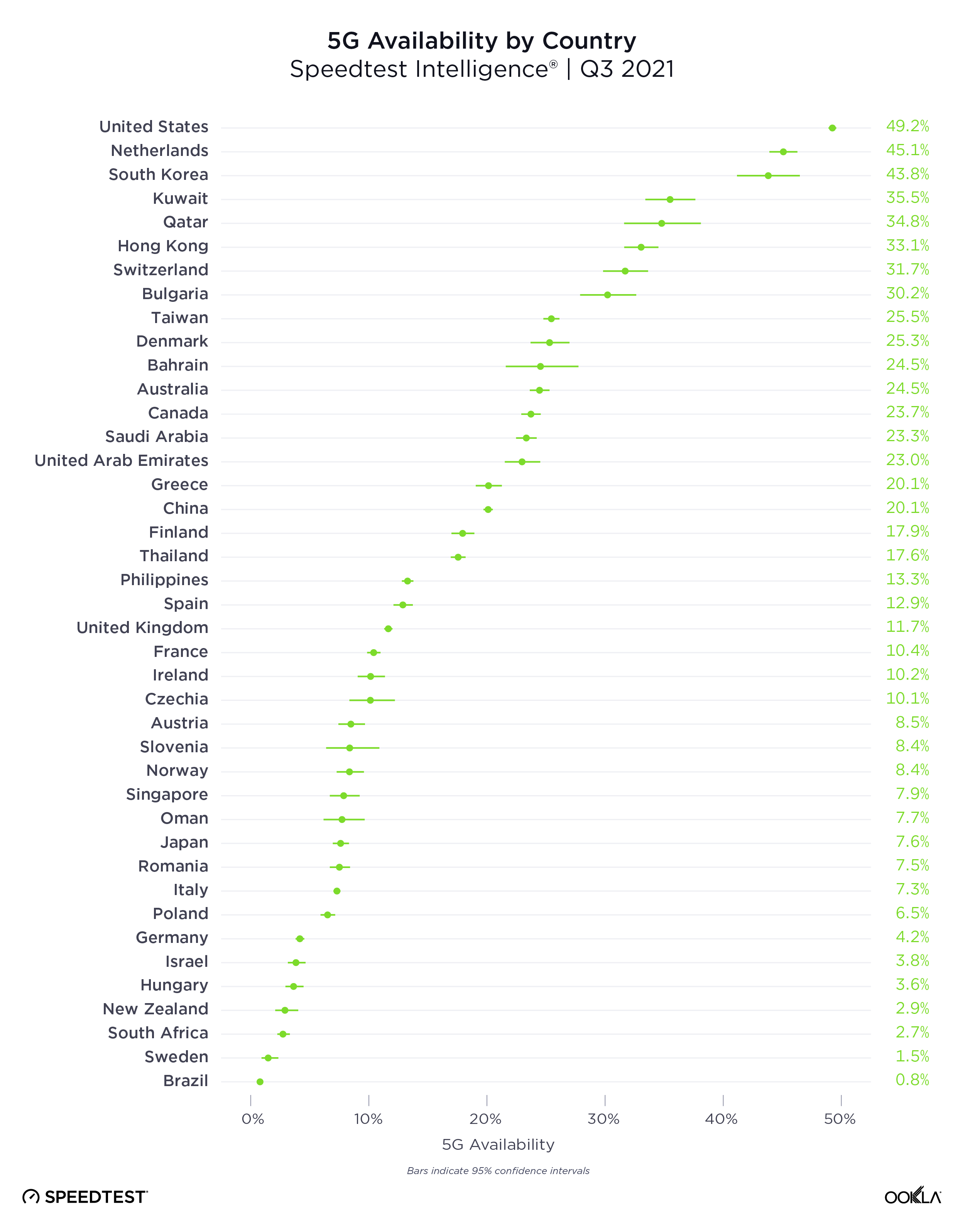

The U.S. had the highest 5G Availability

The presence of 5G is only one indicator in a market, because even in markets where 5G has launched, coverage and adoption can be pretty low. We analyzed 5G Availability to see what percent of users on 5G-capable devices spent the majority of their time on 5G, both roaming and on-network during Q3 2021.

The United States had the highest 5G Availability at 49.2%, followed by the Netherlands (45.1%), South Korea (43.8%), Kuwait (35.5%) and Qatar (34.8%). Brazil had the lowest 5G Availability on our list at 0.8%, followed by Sweden (1.5%), South Africa (2.7%), New Zealand (2.9%) and Hungary (3.6%).

Not all 5G networks are created equal

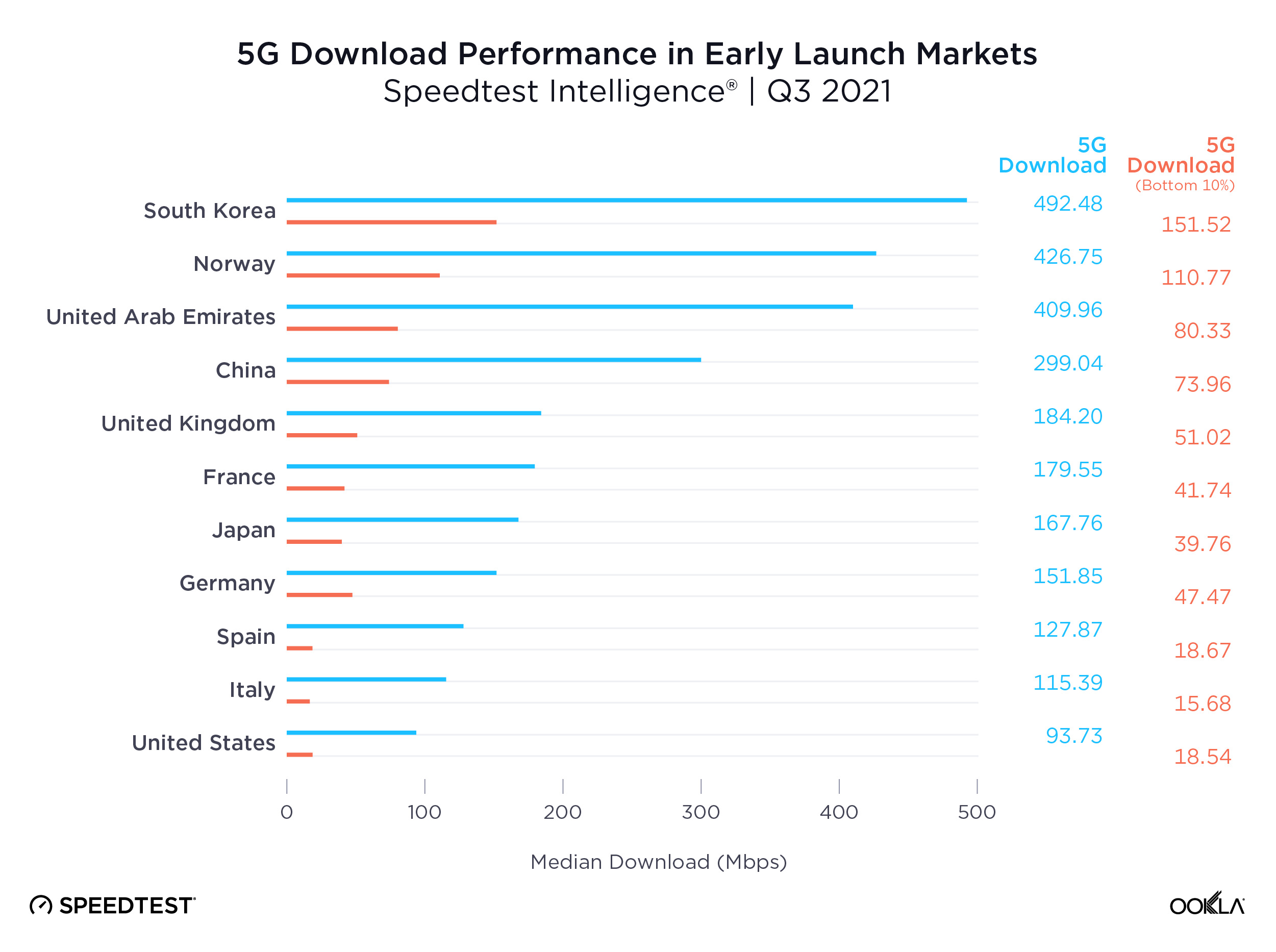

Ookla Speedtest Intelligence data shows a growing disparity in the performance of 5G networks worldwide, even among the pioneer markets who were among the first to launch the new technology. We see leading markets such as South Korea, Norway, the UAE and China pulling well ahead of key European markets, the U.S. and Japan on 5G download speeds, creating what increasingly looks like two tiers of 5G markets.

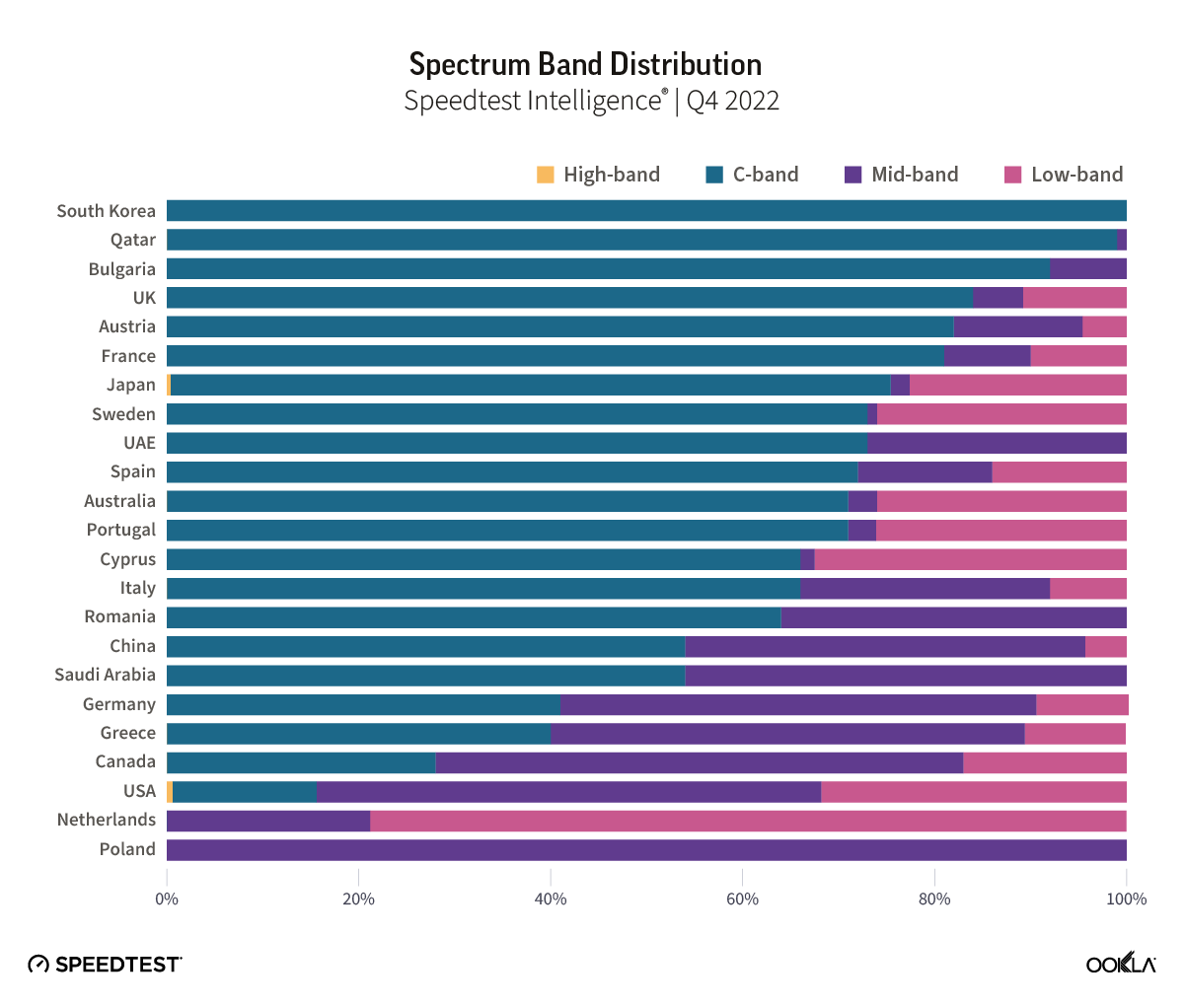

Part of the reason for this divergence is access to key 5G spectrum bands, with Verizon and AT&T in the U.S. for example, soon to deploy their C-band spectrum holdings for 5G use. However, what really seems to separate these markets is the level of 5G network densification. The number of people per 5G base station ranges from 319 in South Korea and 1,531 in China, to 4,224 in the EU and 6,590 in the US, according to the European 5G Observatory’s International Scoreboard during October 2021.

Despite the noise around 6G, 5G still has a long way to run

Median 5G mobile download speeds across these markets are respectable relative to the International Telecommunication Union’s (ITU) IMT-2020 target of 100 Mbps for user experienced download data rates. However, 5G Speedtest® results in each market demonstrate significant variability, with the bottom 10th percentile only recording speeds in excess of the IMT-2020 target in South Korea and Norway, and falling significantly short in many other markets, with Spain, Italy and the U.S. below 20 Mbps.

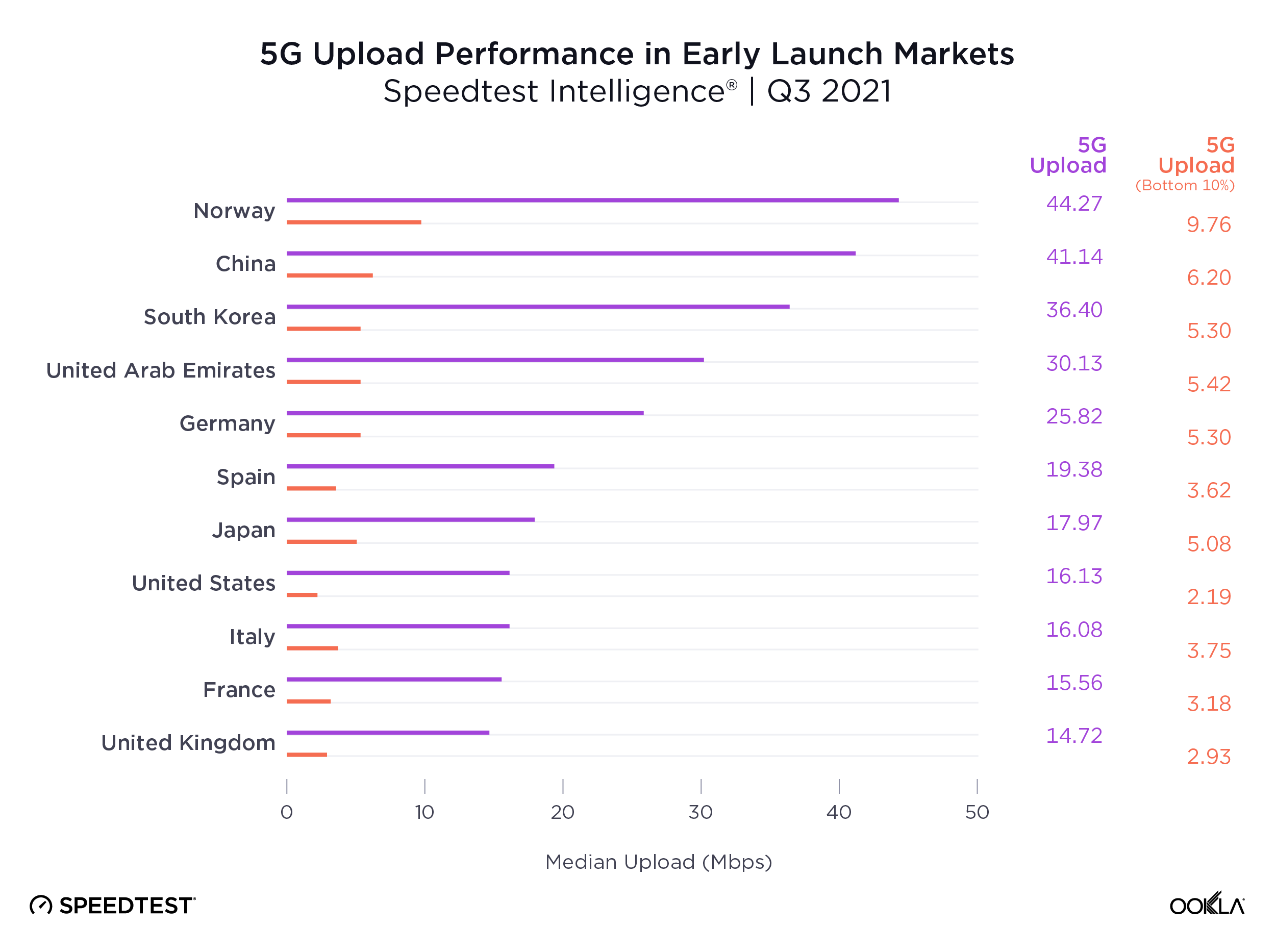

The story gets worse for upload speeds, where no market’s median speed broke the IMT-2020 recommended 50 Mbps, and where the bottom 10th percentile lay in single digits across the board. Operators are clearly prioritizing download speeds over upload, which makes sense given the asymmetric nature of demand, with most consumer applications requiring higher download speeds. However, as operators increasingly look to target the enterprise market with 5G connectivity and consumer demand for services such as video calling and mobile gaming continues to rise, operators will need to boost upload speeds.

Demand for mobile internet bandwidth continues to grow, up 43% year-on-year in Q3 2021 according to Ericsson’s latest mobility report. Looking ahead to 2022, operators will need to increase the capacity of their 5G networks to tackle this growing demand while driving network speeds to new heights. We’ve seen the impact the deployment of new spectrum can have on congested networks during 2021, with Reliance Jio witnessing a bump in 4G LTE performance and consumer sentiment following its acquisition of additional spectrum in India.

Where 5G still fails to reach

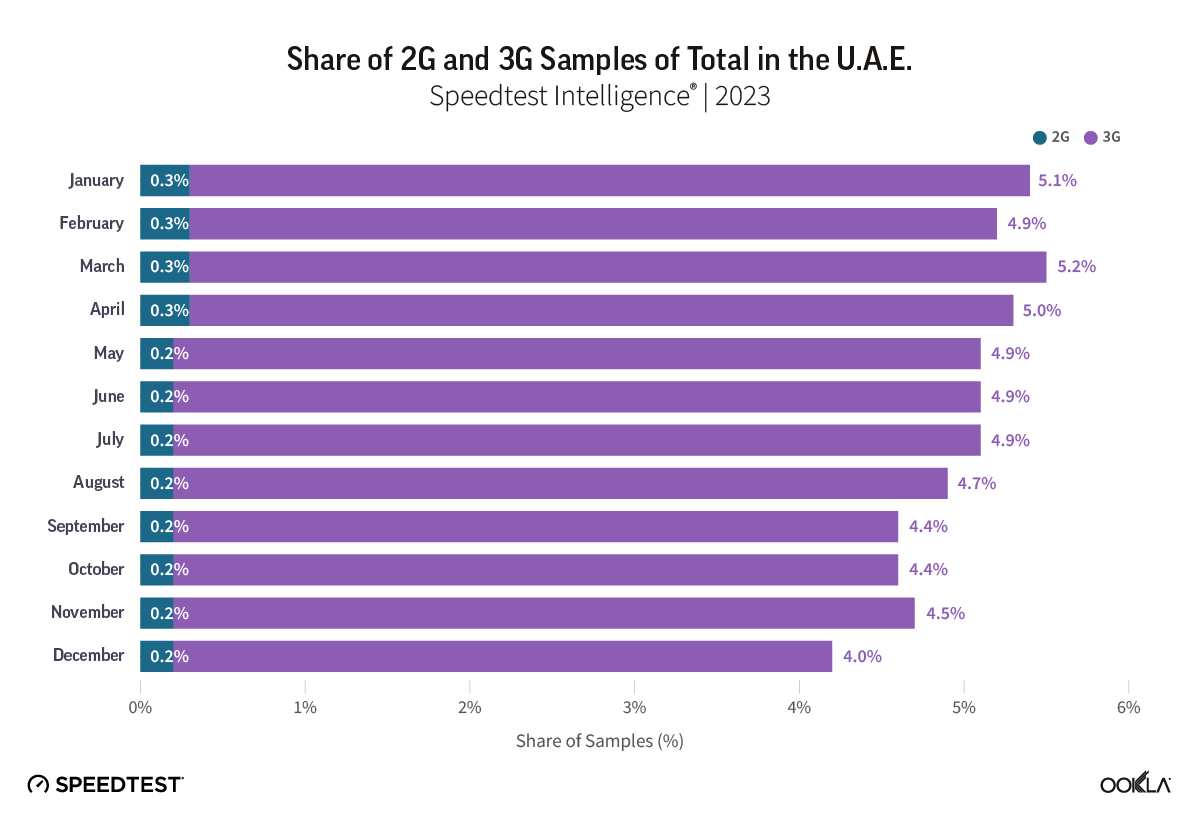

Speedtest Intelligence showed 70 countries in the world where more than 20% of samples were from 2G and 3G connections (combined) during Q3 2021 and met our statistical threshold to be included. These are mostly countries where 5G is still aspirational for a majority of the population. As excited as we are about the expansion of 5G, we do not want to see these countries left behind. Not only are 2G and 3G decades old, they are only sufficient for basic voice and texting, social media and navigation apps. To deliver rich media experiences or video calling, users need access to 4G or higher. Having so many consumers on 2G and 3G also prevents mobile operators from refarming that spectrum to make 4G and 5G networks more efficient.

Countries That Still Rely Heavily on 2G and 3G Connections

Speedtest IntelligenceⓇ | Q3 2021

Country

2G & 3G Samples

Central African Republic

89.9%

Palestine

84.7%

Yemen

72.4%

Turkmenistan

71.8%

Micronesia

56.3%

Madagascar

55.0%

Belarus

53.2%

Rwanda

51.7%

Kiribati

48.4%

Equatorial Guinea

47.6%

Afghanistan

44.4%

South Sudan

43.4%

Guyana

42.3%

Guinea

37.0%

Angola

36.8%

Cape Verde

35.9%

Tajikistan

35.6%

Zimbabwe

34.7%

Benin

34.4%

Togo

33.8%

Ghana

33.0%

Sierra Leone

31.7%

Antigua and Barbuda

30.2%

Vanuatu

30.1%

Lesotho

30.0%

Syria

29.6%

Moldova

29.4%

Saint Kitts and Nevis

28.9%

Mozambique

28.8%

Sudan

28.4%

Palau

28.3%

Grenada

28.1%

Tanzania

27.6%

Uganda

27.5%

Niger

27.5%

Gabon

27.5%

Haiti

27.4%

Suriname

27.4%

Tonga

27.3%

Liberia

27.0%

Namibia

26.7%

Swaziland

26.5%

The Gambia

26.3%

Saint Vincent and the Grenadines

26.3%

Dominica

26.3%

Somalia

26.1%

Cook Islands

26.0%

Zambia

25.9%

Barbados

25.7%

Armenia

25.5%

Algeria

25.4%

Papua New Guinea

25.2%

Jamaica

24.5%

Venezuela

24.2%

Ethiopia

24.1%

Uzbekistan

24.0%

El Salvador

23.5%

Honduras

23.1%

Nigeria

23.0%

Solomon Islands

22.8%

Caribbean Netherlands

22.7%

Botswana

22.3%

Anguilla

21.7%

Mauritania

20.6%

Saint Lucia

20.5%

Bosnia and Herzegovina

20.3%

Burundi

20.3%

Ecuador

20.2%

Ukraine

20.1%

Trinidad and Tobago

20.0%

We were pleased to see the following countries come off the list from last year, having dropped below the 20% threshold: Azerbaijan, Bangladesh, Belize, Burkina Faso, Cameroon, Costa Rica, Côte d’Ivoire, DR Congo, Iraq, Kenya, Laos, Libya, Maldives, Mali, Mauritius, Mongolia, Nicaragua, Paraguay and Tunisia. While countries like Palestine, Suriname, Ethiopia, Haiti and Antigua and Barbuda are still on this list, they have improved the percentage of their samples on these outmoded technologies when compared to last year (dropping 10-15 points, respectively), 2G and 3G samples in Belarus increased 6.7 points when comparing Q3 2021 to Q3 2020.

We’re excited to see how performance levels will normalize as 5G expands to more and more countries and access improves. Keep track of how well your country is performing on Ookla’s Speedtest Global Index™.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

The Gulf region and Turkey have experienced a surge in air passenger traffic. The growth is expected to remain robust in key hubs such as Dubai, Doha, and Istanbul. As airports prepare to accommodate this influx of travelers, reliable and high-performance cellular networks have become increasingly important in shaping the overall passenger experience. This article benchmarks the network performance of the busiest airports in the Gulf region and Turkey, in terms of download and upload speeds, as well as latency, based on Speedtest Intelligence® data. It also provides recommendations on where travelers may get the best online experience.

Key Takeaways:

Zayed International Airport (AUH) achieves top-tier mobile download speeds of over 450 Mbps. Istanbul Airport (IST) excels in upload speed at 58.40 Mbps, making it particularly suitable for travelers who need to share content efficiently. On the other end, King Abdulaziz International Airport (JED) in Jeddah consistently underperforms across all metrics, with the highest latency and lowest upload speed.

Istanbul Airport significantly leads in 5G performance thanks to a dedicated 5G indoor network: IST achieved the highest download and upload speeds at 861.98 Mbps and 101.96 Mbps, respectively. Gulf-based airports showed a high contrast in median 5G download speeds, with those in Qatar and the UAE offering the fastest speeds at over 500 Mbps.

Most airports provided a median download speed of at least 200 Mbps, enabling an excellent online experience for passengers

While Turkey has long been a magnet for tourists, the Gulf region has emerged as one of the world’s premier travel hubs, attracting hundreds of millions of passengers annually. As a result, airport operators in the region face a pressing need to deliver seamless web browsing, lag-free online gaming, and high-quality streaming experiences to enhance the overall passenger experience and set a new standard for airport facilities. We used Speedtest Intelligence to analyze cellular network performance in the busiest airports in the Gulf region and Turkey.

Total Passengers In Selected Busiest Airports In The Gulf Region And Turkey

Wikipedia | 2024

Total Passengers In Selected Busiest Airports In The Gulf Region And Turkey

Download speed is the most important metric for content consumption and online experience. Zayed International Airport (AUH) had a median download speed of 453.18 Mbps. It was closely followed by Hamad International Airport (DOH), with a speed of 426.43 Mbps. King Khalid International Airport (RUH) and Istanbul International Airport (IST) also delivered excellent download speed performances at 329.04 Mbps and 314.84 Mbps, respectively.

In contrast, Sabiha Gökçen Airport (SAW) and Muscat International Airport (MCT) delivered sub-100Mbps speeds of 78.67 Mbps and 95.95 Mbps, respectively. Airports based in Dubai and Kuwait fall into the mid-range, with download speeds of around 250 Mbps.

Upload speed is important as it determines how efficiently users can upload documents, photos, and videos. IST stands out with a median upload speed of 58.40 Mbps, surpassing all other airports. RUH in Riyadh, DOH in Doha, and SAW in Istanbul follow with upload speeds of 32.83 Mbps, 30.10 Mbps, and 29.10 Mbps, respectively. King Abdul Aziz International Airport (JED) in Jeddah falls short, delivering the lowest upload speed of just 16.11 Mbps, while DXB pulls slightly ahead with 18.99 Mbps.

Latency measures the delay in transferring data and affects real-time services such as video calls, online gaming, and media streaming. Most airports offer a sub-40 ms latency, which ensures acceptable responsiveness for users. IST and Kuwait International Airport (KWT) have somewhat better conditions, with a delay of under 32 ms. JED stood out again as a poor performer with a latency of 89.98 ms, suggesting a significant impact on real-time applications such as gaming and video conferencing.

All Technologies Network Performance, Select Airports in the Gulf and Turkey

Speedtest Intelligence® | 2024

All Technologies Network Performance, Select Airports in the Gulf and Turkey

Istanbul Airport significantly leads the region in 5G performance thanks to a dedicated 5G indoor network

As 5G adoption increases, consumers and businesses expect the same level of coverage and performance wherever they go. Yet, the characteristics of ‘outdoor’ 5G, which typically operates in mid-band frequencies of 1.8 GHz to 3.5 GHz, pose a challenge for indoor coverage, as these frequencies struggle to penetrate walls and windows, particularly those built of glass and steel. Furthermore, telecom operators have prioritized outdoor coverage because it requires less CAPEX and OPEX per subscriber than indoor coverage and has a better return on investment. In addition, the traffic patterns in the airport are highly variable, which means that the network must be capable of accommodating different connectivity levels.

The introduction of 5G in Turkey lags significantly behind as 700 MHz, 3.5 GHz, and 26 GHz frequencies will be auctioned in 2025, with commercial launch expected in 2026. However, Istanbul International Airport (IST) deployed a dedicated indoor 5G network that serves only users within the airport’s premises. This deployment gives it performance advantages compared to public 5G networks. Speedtest Intelligence data shows that IST secured the top spot for 5G median download and upload speeds at 861.98 Mbps and 101.96 Mbps, respectively.

Airports in Abu Dhabi (AUH) and Doha (DOH) also have high 5G download speeds, at 678.11 Mbps and 657.56 Mbps, respectively. All other Gulf-based airports provided a median download speed of at least 107 Mbps, enabling users to stream multiple 4K videos over 5G.

Gulf airports lagged significantly behind IST in upload speeds, with four locations’ speeds ranging from around 30 Mbps to 45 Mbps. The other four Gulf-based airports underperformed, with MCT and JED at the bottom of the list with a median upload speed of 15.09 Mbps and 17.84 Mbps, respectively, despite deployingsolutions to improve indoor network coverage and capacity.

Most airports offer a relatively low 5G latency, around 30 ms to 36 ms, suggesting good service responsiveness. The only exception is JED, with a median latency of 86.59 ms, likely degrading the customer experience of real-time services such as video streaming.

5G Network Performance, Select Airports in the Gulf and Turkey

Speedtest Intelligence® | 2024

5G Network Performance, Select Airports in the Gulf and Turkey

As the results show, airports in the Gulf region and Turkey generally have excellent mobile network performance inside and around these facilities. These achievements were realized thanks to the deployment of 5G and investment in solutions to improve indoor coverage and capacity.

The tourism boom in Turkey and the Gulf region is set to continue and will drive infrastructure investment and economic growth

According to GlobalData, the number of international arrivals into the GCC (Gulf Cooperation Council) reached 73.64 million travelers in 2023. The U.A.E. leads the GCC in terms of tourist numbers with 28.2 million visitors in the city during H1 2024, while Saudi Arabia received 27.4 million visitors (including pilgrims) with the ambition to grow to 150 million by 2030. The tourism sector in Qatar is also a promising destination, with 3 million visitors in 2023, benefiting from the successful hosting of the World Cup in 2022. Oman welcomed 3.4 million tourists in 2023 and plans to attract 11.7 million by 2040.

These countries have invested heavily in infrastructure, including transport, to address the growing influx of tourists and translate into economic growth. They have also built new airports and upgraded existing ones to cater to the rise in air passenger traffic, which is expected to surge to 449 million in 2024, more than double its 2019 level.

The new Istanbul airport was inaugurated in 2018 to make Turkey’s capital one of the world’s largest financial and economic centers. It had an initial capacity of 90 million passengers annually, making it a major gateway for international visitors and contributing to the country’s economy. According to the Ministry of Culture and Tourism, the number of tourist arrivals in the country increased by 7% to 47.3 million during the first 10 months of 2024 compared to the same period the previous year. It plans to expand its capacity to 120 million passengers in 2025.

As the Gulf region and Turkey continue to experience a surge in air passenger traffic, it is essential to meet their expectations for fast and reliable connectivity to enhance their overall experience and gain a competitive edge over other airports. By doing so, they can unlock new growth opportunities, improve customer loyalty, and strengthen their position as major global travel hubs.We will continue to monitor network performance in key locations where people spend their time and how it impacts their online experience. If you are interested in Speedtest Intelligence, please contact us.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

5G is no longer a new technology, however, consumers in many countries are still waiting to see the full benefits of 5G (or even to connect to 5G at all). We examined Speedtest Intelligence® data from Q3 2022 Speedtest® results to see how 5G performance has changed since last year, where download speeds are the fastest at the country level, and how satellite technologies are offering additional options to connect. We also looked at countries that don’t yet have 5G to understand where consumers are seeing improvements in 4G LTE access.

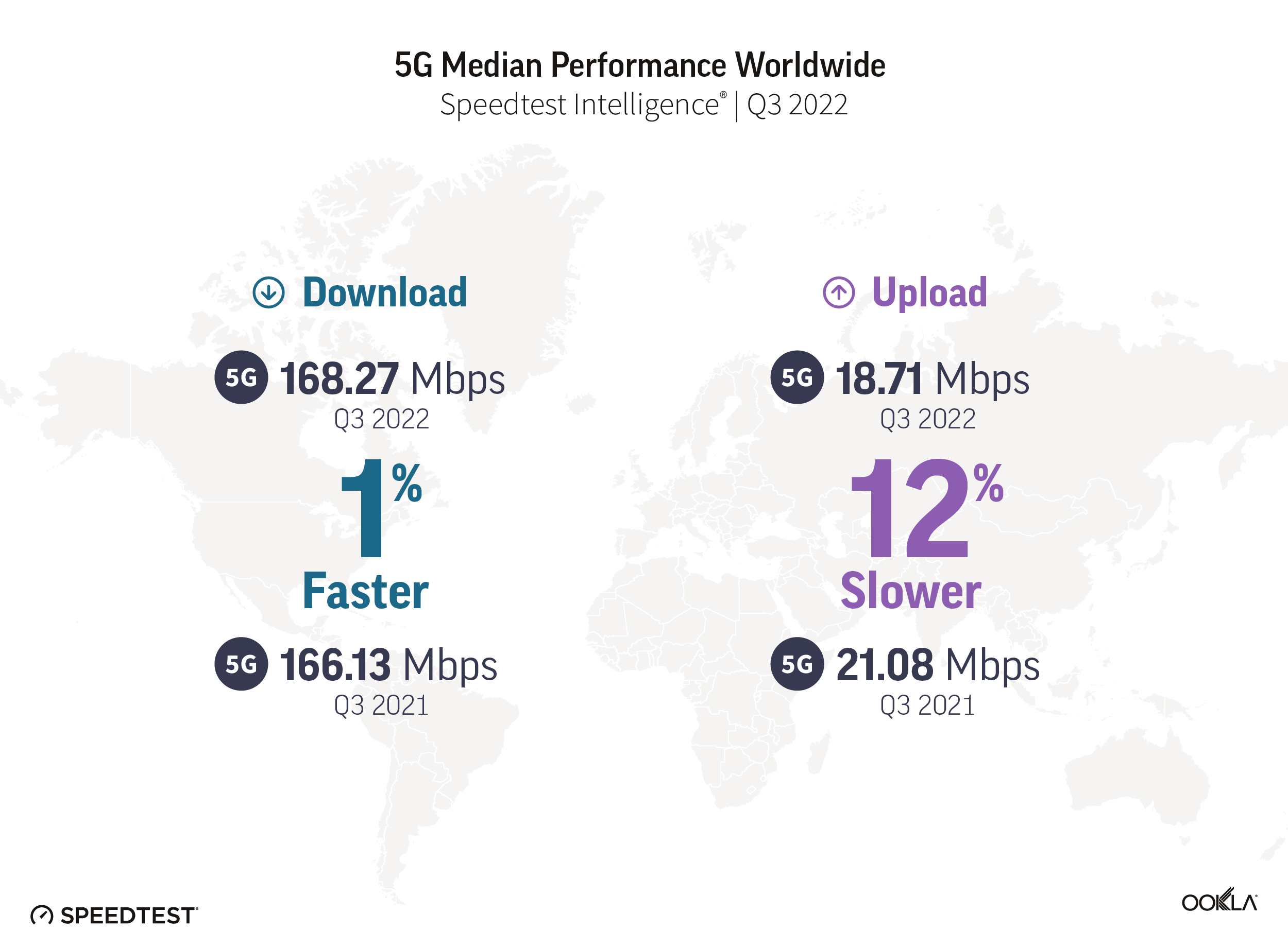

5G speeds were stable at the global level

In 2021, we discussed how an expansion of 5G access led to a decline in overall speed at the global level. This year showed a stabilization in overall speed, even as 5G access broadened, with a median global 5G download speed of 168.27 Mbps in Q3 2022 as compared to 166.13 Mbps in Q3 2021. Median upload speed over 5G slowed slightly to 18.71 Mbps (from 21.08 Mbps) during the same period. According to the Ookla® 5G Map™, there were 127,509 5G deployments in 128 countries as of November 30, 2022, compared to 85,602 in 112 countries the year prior.

South Korea and the United Arab Emirates led countries for 5G speeds

South Korea and the U.A.E. had the fastest median download speed over 5G at 516.15 Mbps and 511.70 Mbps, respectively, during Q3 2022, leading a top 10 list that included Bulgaria, Qatar, Saudi Arabia, Singapore, Kuwait, New Zealand, Bahrain, and Brazil. Bulgaria, Singapore, Bahrain, and Brazil were new to the top 10 in 2022, while Norway, Sweden, China, and Taiwan fell out of the top 10.

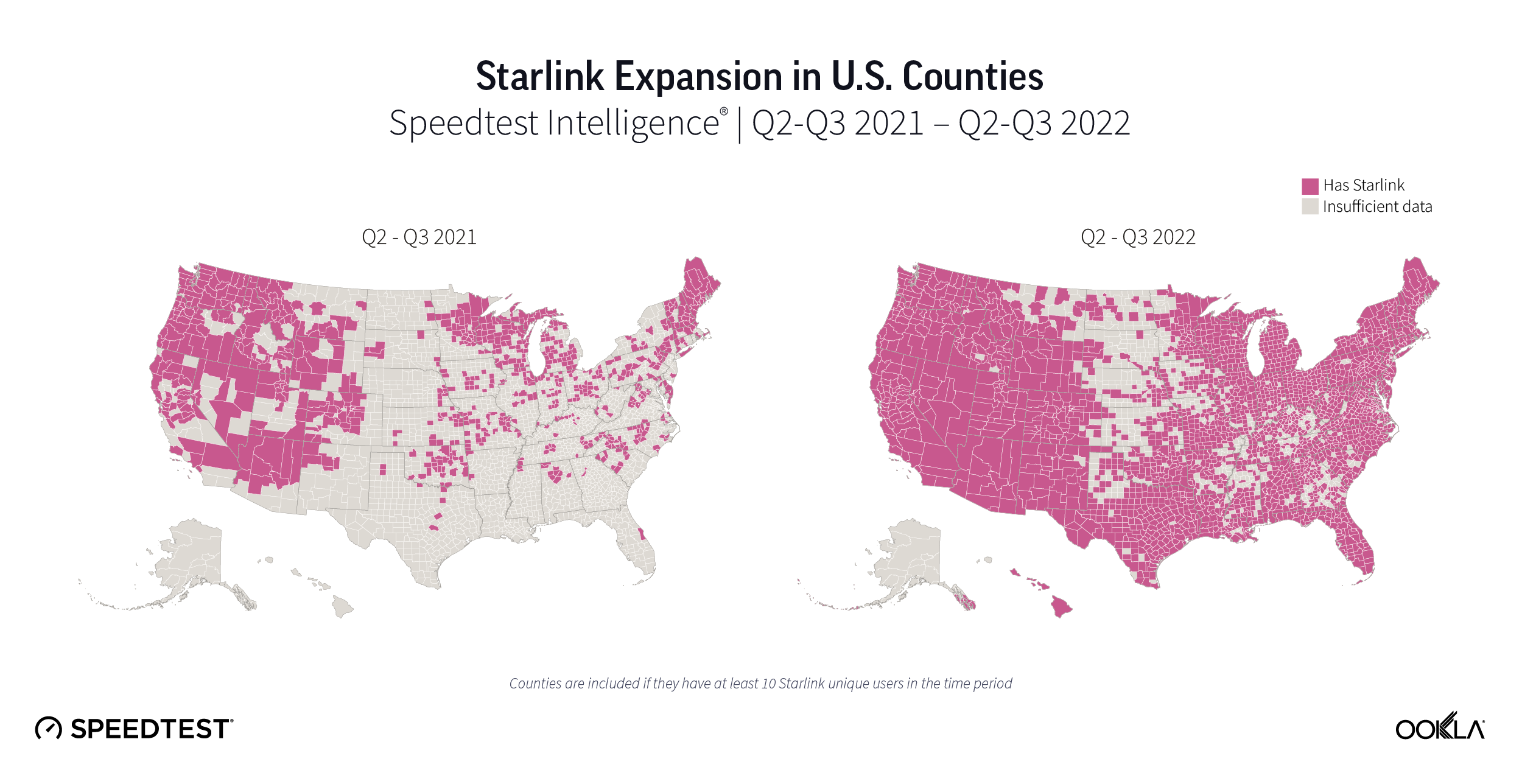

Satellite became more accessible but performance slowed

2022 saw a proliferation of fast, low-earth orbit (LEO) satellite internet from Starlink across the world. Q1 2022 saw Starlink speeds increase year over year in Canada and the U.S., with Starlink in Mexico having the fastest satellite internet in North America, Starlink in Lithuania the fastest in Europe, Starlink in Chile the fastest in South America, and Starlink in Australia the fastest in Oceania.

Q2 2022 saw Starlink speeds decrease in Canada, France, Germany, New Zealand, the U.K., and the U.S. from Q1 2022 as Starlink crossed the 400,000 user threshold across the world. Starlink in Puerto Rico debuted as the fastest satellite provider in North America. Starlink outperformed fixed broadband averages in 16 European countries. Starlink in Brazil had the fastest satellite speeds in South America. And Starlink in New Zealand was the fastest satellite provider in Oceania.

During Q3 2022, Starlink performance dipped once again from Q2 2022 in Canada and the U.S., while remaining about the same in Chile. Starlink in Puerto Rico and the U.S. Virgin Islands had the fastest satellite speeds in North America, while Starlink in Brazil again was the fastest satellite provider in South America.

With Viasat, HughesNet, and Project Kuiper set to launch huge LEO constellations in 2023, consumers around the world are poised to have more fast satellite internet options, particularly as the European Commission makes its own play for a constellation and Eutelsat and OneWeb potentially merging.

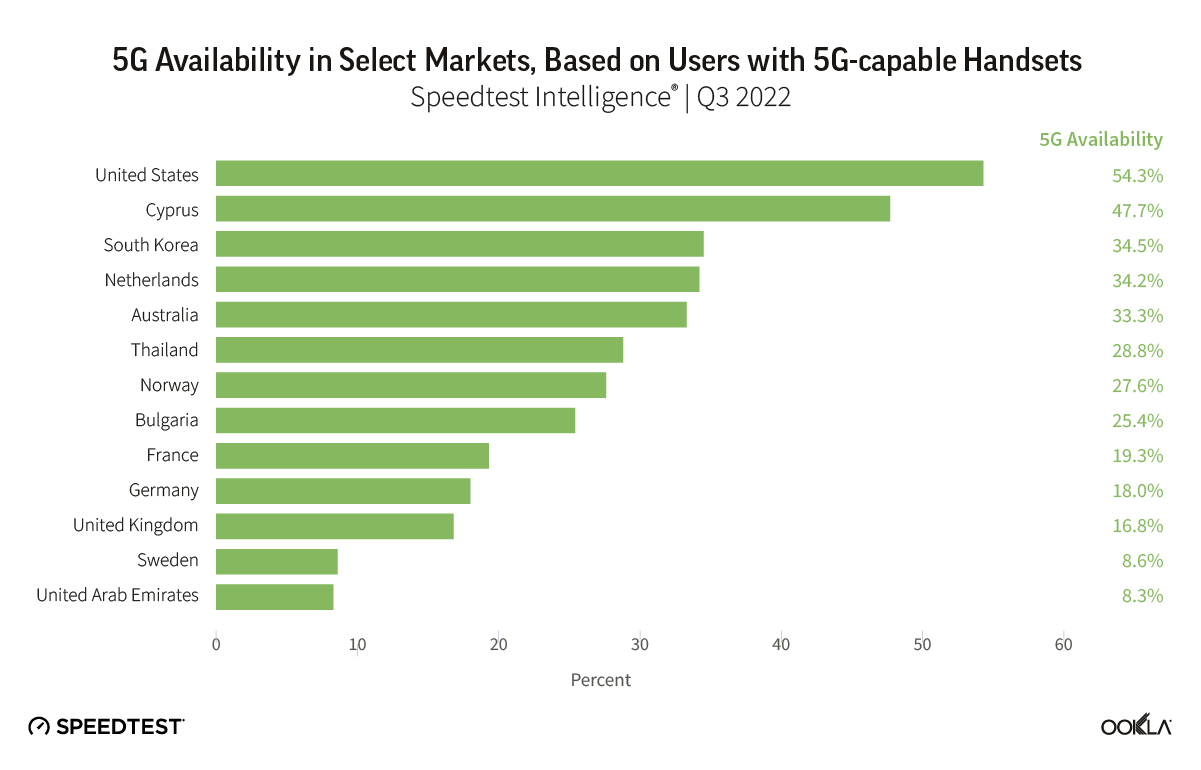

5G Availability points to on-going challenges

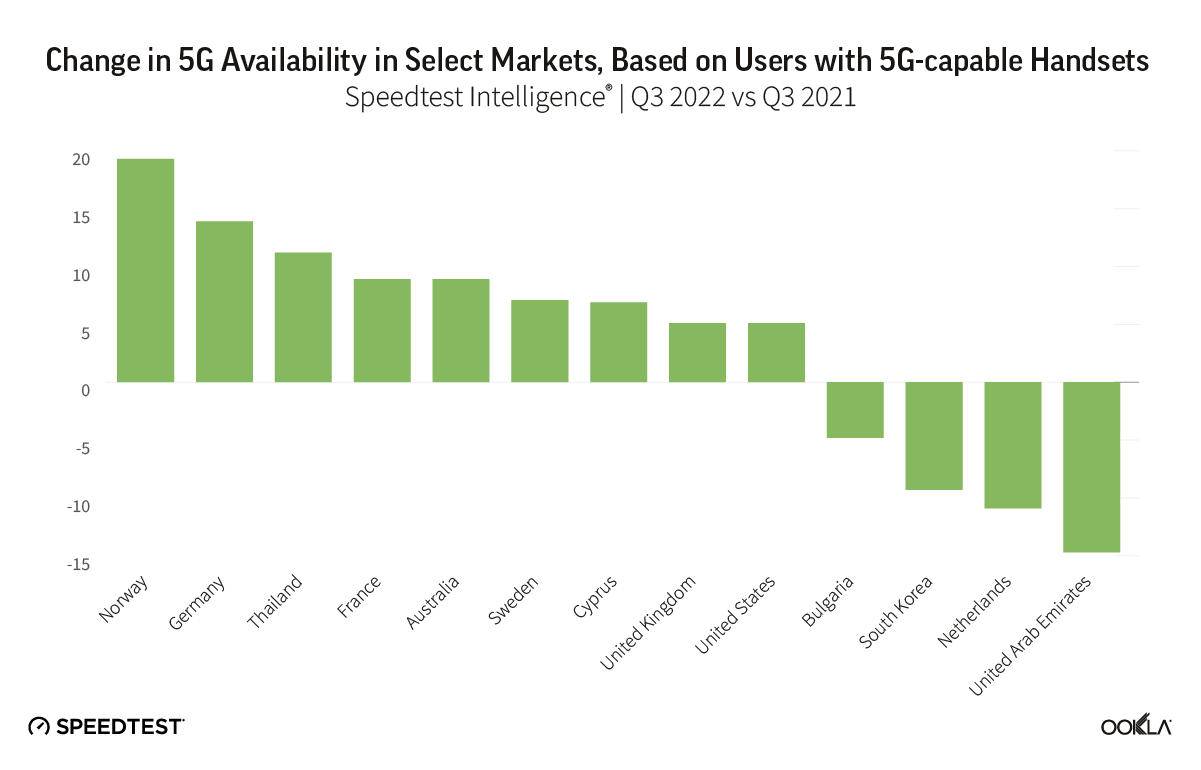

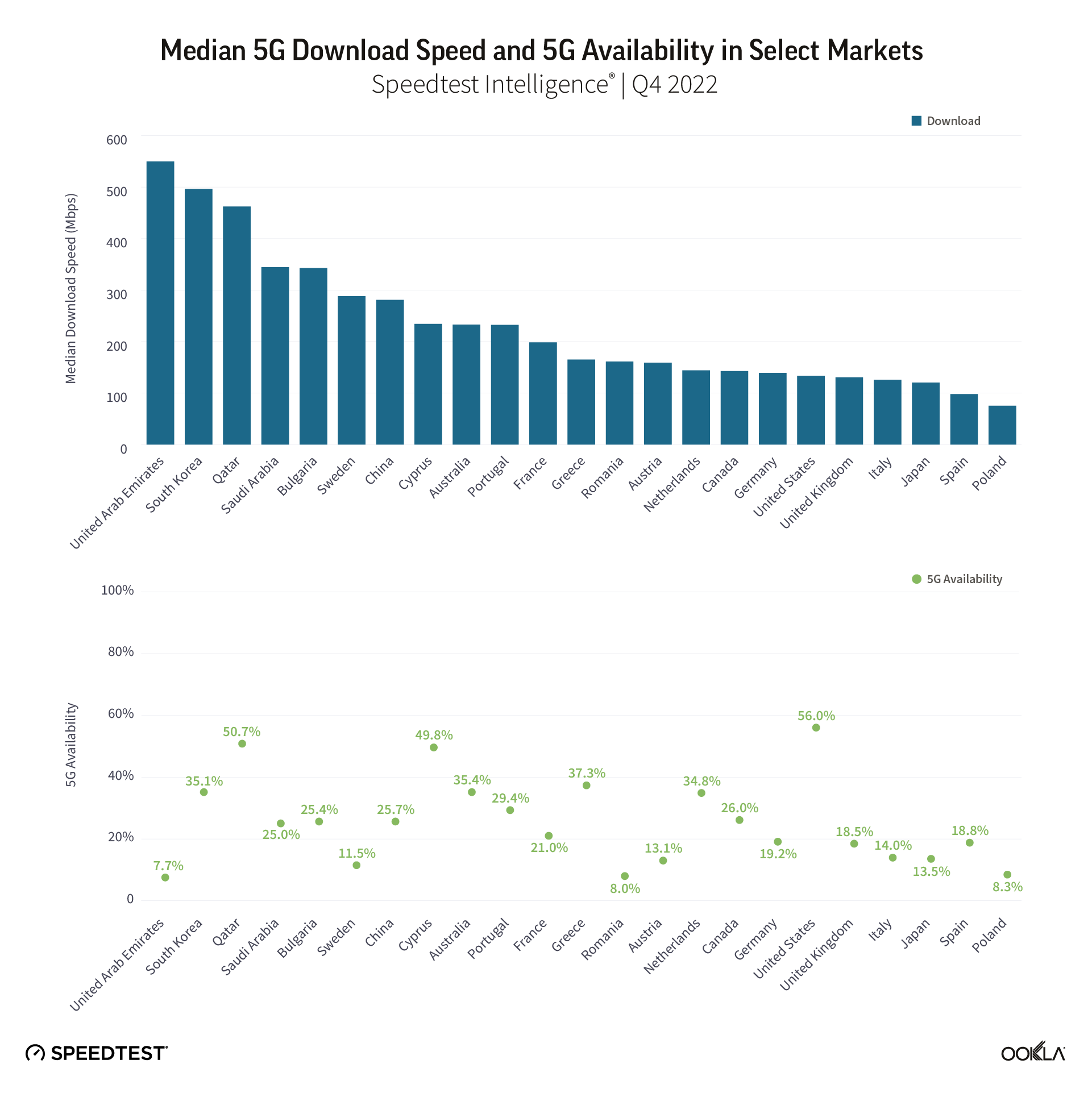

5G Availability measures the proportion of Speedtest users with 5G-capable handsets, who spend a majority of time connected to 5G networks. It’s therefore a function of 5G coverage and adoption. We see wide disparity in 5G Availability among markets worldwide, with for example the U.S. recording 54.3% in Q3 2022, well ahead of markets such as Sweden and the U.A.E., with 8.6% and 8.3% respectively.

Critical levers for mobile operators to increase 5G Availability include:

Increasing 5G coverage by deploying additional base stations

Obtaining access to, or refarming, sub-GHz spectrum, to help broaden 5G coverage, as sub-GHz spectrum has superior propagation properties than that of higher frequency spectrum bands.

Encouraging 5G adoption among users with 5G-capable handsets.

Speedtest Intelligence points to 5G adoption challenges in some markets, with 5G Availability dropping in Bulgaria, South Korea, the Netherlands, and the U.A.E. As more users acquire 5G-capable devices, operators need to balance their pricing models to ensure users have sufficient incentives to purchase a 5G tariff.

Where 5G continues to fail to reach

Speedtest Intelligence showed 29 countries in the world where more than 20% of samples were from 2G and 3G connections (combined) during Q3 2022 and met our statistical threshold to be included (down from 70 in Q3 2021). These are mostly countries where 5G is still aspirational for a majority of the population, which is being left behind technologically, having to rely on decades-old technologies that are only sufficient for basic voice and texting, social media, and navigation apps. We’re glad to see so many countries fall off this list, but having so many consumers on 2G and 3G also prevents mobile operators from making 4G and 5G networks more efficient. If operators and regulators are able to work to upgrade their users to 4G and higher, everyone will benefit.

Countries That Still Rely Heavily on 2G and 3G Connections

Speedtest IntelligenceⓇ | Q3 2021

Country

2G & 3G Samples

Central African Republic

76.2%

Turkmenistan

58.5%

Kiribati

51.6%

Micronesia

47.4%

Rwanda

41.1%

Belarus

39.7%

Equatorial Guinea

37.7%

Afghanistan

36.7%

Palestine

33.5%

Madagascar

27.5%

Sudan

27.4%

Lesotho

26.5%

South Sudan

26.3%

Benin

26.0%

Guinea

25.5%

Cape Verde

24.3%

Tonga

24.3%

Syria

23.4%

The Gambia

23.4%

Ghana

23.3%

Palau

22.9%

Niger

22.8%

Tajikistan

22.7%

Mozambique

22.4%

Guyana

21.8%

Togo

21.8%

Congo

21.1%

Moldova

20.8%

Saint Kitts and Nevis

20.0%

We were pleased to see the following countries come off the list from last year, having dropped below the 20% threshold: Algeria, Angola, Anguilla, Antigua and Barbuda, Armenia, Barbados, Bosnia and Herzegovina, Botswana, Burundi, Caribbean Netherlands, Cook Islands, Dominica, Ecuador, El Salvador, Ethiopia, Gabon, Grenada, Haiti, Honduras, Jamaica, Liberia, Mauritania, Namibia, Nigeria, Papua New Guinea, Saint Lucia, Saint Vincent and the Grenadines, Sierra Leone, Solomon Islands, Somalia, Suriname, Swaziland, Tanzania, Trinidad and Tobago, Uganda, Ukraine, Uzbekistan, Vanuatu, Venezuela, Yemen, Zambia, and Zimbabwe. While countries like Belarus, Cape Verde, Central African Republic, Guinea, Guyana, Madagascar, Palestine, Rwanda, South Sudan, Tajikistan, Togo, and Turkmenistan are still on this list, they have improved the percentage of their samples on these outmoded technologies when compared to last year by at least 10 points. Palestine improved by more than 50 points. 2G and 3G samples in Kiribati increased 3.2 points when comparing Q3 2022 to Q3 2021.

We’re glad to see performance levels normalize as 5G expands to more and more countries and access improves and we are optimistic that 2023 will bring further improvements. Keep track of how well your country is performing on Ookla’s Speedtest Global Index™ or track performance in thousands of cities worldwide with the Speedtest Performance Directory™.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

Several Middle Eastern countries, including Bahrain, Jordan, Qatar, and the U.A.E., have emerged as leaders in fiber deployment and adoption. The introduction of gigabit packages and the increase in entry-level speeds have significantly boosted their ranking in the Speedtest Global Index® for fixed broadband. This article examines the factors driving performance in these countries, the initiatives of ISPs to enhance indoor performance, and key enablers for wider gigabit internet adoption in the region.

Key Takeaways:

According to Ookla’s Speedtest Intelligence®, the U.A.E. leads the Middle East in fixed broadband performance in Q1 2024. The U.A.E. achieved a median download speed of 270.91 Mbps and an upload speed of 124.37 Mbps. Meanwhile, Bahrain and Qatar saw significant improvements in download and upload speeds, while the median download speed in Jordan rose rapidly from a small base, surpassing Saudi Arabia by Q1 2024.

ISPs are addressing indoor performance bottlenecks with more modern consumer premise equipment (CPE). In-premise connectivity is crucial to guarantee maximum throughput on-premise. That is why ISPs started bundling Wi-Fi 6 compatible CPEs and deploying fiber-to-the-room (FTTR) for ubiquitous gigabit wireless access indoors.

Affordability is a barrier to wider gigabit adoption in the Middle East. While geography, level of competition, and government policies all impact fiber deployment, affordability is key to unlocking faster speeds in the region. Making gigabit plans more accessible can help operators boost fiber subscribers and aspiring countries to move up the Speedtest Global Index.

The U.A.E. tops the Middle East in Speedtest Global Index for fixed broadband

The analysis focuses on countries in the Middle East that are leading in fiber coverage, adoption, and speed enhancements, namely Bahrain, Jordan, Qatar, Saudi Arabia, and the U.A.E. These achievements were thanks to significant progress by local ISPs in extending fiber coverage, encouraging migration to higher-speed plans, and making services more affordable. Government support has been vital in accelerating fiber roll-outs to keep pace with the demand for data services and to ensure universal access to high-speed internet as part of national broadband development strategies.

As a result, these countries continue to improve their Speedtest Global Index rankings. For example, the U.A.E rose from 18th in June 2020 to the second position in March 2024. Jordan jumped from 64th to 33rd while Bahrain jumped up 32 places to 63rd in the Index over the same period. Qatar’s position fluctuated between 29 and 45, with steady improvements since 2021. Saudi Arabia’s speed increase rate has been more modest than in other markets, causing a drop in the global ranking by 11 places to 46th in March 2024. The country is the largest in the group, which makes fiber coverage more limited outside the big cities, while there is a relatively large base of legacy copper connections.

Speedtest Global Index™ Rankings for Fixed Broadband, Select Countries in the Middle East

Speedtest Intelligence® | June 2020-March 2024

Speedtest Global Index Rankings for Fixed Broadband, Select Countries in the Middle East

Fixed broadband performance improved as faster entry-level fiber plans and gigabit packages were introduced

According to Speedtest Intelligence, the U.A.E. leads the Gulf region in median download speeds at 270.91 Mbps in Q1 2024, more than double the Q3 2022 figure. This represents the largest speed improvement among the reviewed countries. The turning point came in Q4 2022 when ISPs lifted the minimum broadband package speed from 250 Mbps to 500 Mbps and offered aggressive discounts to encourage upselling to faster fiber packages. The median upload speed also saw notable improvement, reaching 124.37 Mbps in March 2024.

Median Download Speeds for Fixed Broadband, Select Countries in the Middle East

Speedtest Intelligence® | Q1 2022-Q1 2024

Median Download Speeds for Fixed Broadband, Select Countries in the Middle East

Bahrain and Qatar also experienced significant and rapid rises in median download speeds, reaching 83.09 Mbps and 135.34 Mbps, respectively. The ISPs in the two countries saw significant improvements in upload speeds too. Users in Qatar saw the biggest jump in median upload speed, tripling from Q1 2022 to Q1 2024 to 115.74 Mbps. In Bahrain, the median upload speed increased by over 2.7x but remained the lowest of the group at 20.70 Mbps.

In Bahrain, the telecoms regulator mandated ISPs to double the speed of entry-level fiber packages in April 2023 while maintaining the same wholesale prices. This immediately impacted the market, with median broadband download speeds jumping from 48.14 Mbps in Q1 2023 to 70.17 Mbps in Q2 2023 (over 40%).

Qatar was the first country in the GCC to offer 10 Gbps consumer broadband packages. However, Ooredoo and Vodafone maintained a relatively low download speed on entry-level tariffs at 100 Mbps. This changed in June 2023, when they raised the minimum speed to 1 Gbps while offering discounts on more expensive fiber packages. These initiatives resulted in a step change in download speeds, increasing by 41% in Q1 2024 compared to Q2 2023.

Jordan began ramping up its fiber infrastructure in 2013-2014, with strong take-up since 2019 driven by increased competition, extended coverage outside the capital, and rising demand due to the COVID-19 pandemic. The launch of Fibertech, a fiber wholesale company, in 2019 significantly boosted service competition and led to more accessible and affordable fiber services for consumers. Fibertech, set up as a joint venture between ISP Umniah and Jordan Electricity Company, covered 1.2 Million households by July 2023 and planned to reach 1.4 million premises, 70% of Jordan’s households, by the end of that year.

Fiber overtook fixed wireless access (FWA) and ADSL connections in Q2 2021 and represented 56% of fixed broadband connections by the end of 2022. Fiber maintained its upward trajectory, capturing 64% of the market in 3Q 2023 with 513,744 active connections according to the last reported data from the Telecommunication Regulatory Commission (TRC)). Local ISPs have also been increasing the speed of entry-level plans and offering gigabit packages. For example, Orange Jordan introduced 2 Gbps and 10 Gbps plans in May 2023. This accelerated fiber take-up boosted the median speeds for both download and upload, reaching 130.41 Mbps and 108.08 Mbps, respectively, in Q1 2024. Notably, Jordan doubled its median upload speed in two years, narrowing the gap with its median download speed.

In Saudi Arabia, stc led the way by increasing the minimum download speed from 100 Mbps to 300 Mbps in the summer of 2022. Mobily followed suit in 2023 by doubling the speed of its entry-level package and introducing a 1 Gbps broadband plan during Q2 2023. Zain initially reserved higher download speeds (ranging from 200 Mbps to 500 Mbps) for customers on 2-year contracts, while those on 12-month contracts received speeds between 100 Mbps and 300 Mbps. However, in 2023, Zain merged its plans into a standard 18-month contract starting at 200 Mbps, with 1 Gbps at the high end. These initiatives began to impact the market in Q2 2023, when the median download speed surpassed 90 Mbps for the first time, reaching 108.95 Mbps by Q1 2024. Upload speeds also saw significant growth, rising to 53.75 Mbps during this period.

Speedtest Intelligence’s Enrichment API allows us to track the adoption and performance of individual fixed broadband technologies and assess their impact on the Saudi market. For example, the fiber share of stc Speedtest samples has been growing – fiber represented 75.4% of Speedtest samples in March 2024, up from 69.9% in Q4 2023. This increased fiber adoption contributed to raising overall fixed broadband performance across download, upload, and latency metrics and widened the performance gap with legacy DSL lines. This result also highlights the potential for further improvement if most samples (and by extension, customers) switch to fiber.

DSL and Fiber Performance, Saudi Arabia

Speedtest Intelligence® | Q4 2022 – Q1 2024

DSL and Fiber Performance, Saudi Arabia

Improving indoor coverage is key to ensuring maximum fiber performance delivery to customers

ISPs in the analyzed countries have rapidly expanded their fiber footprint and migrated customers to faster broadband services, helping to increase the median download speed. However, the last few meters indoors, closer to the end-users, can be a potential bottleneck to achieving maximum throughput. To address this, local ISPs have taken steps such as:

Offering upgraded CPEs that support Wi-Fi 6. The choice of Wi-Fi standards and spectrum bands directly influences indoor connectivity quality, throughput, and network coverage. Our recent analysis found that over one-third of test samples in the Gulf region reported using Wi-Fi 4 to connect to the fixed CPE. More ISPs are now offering Wi-Fi 6 compatible CPEs and including additional mesh Wi-Fi nodes at no extra costs to improve indoor coverage and speed.

Deploying fiber-to-the-room (FTTR). This relatively new technology involves deploying and extending fiber connectivity to each room, usually through transparent cables, to provide ubiquitous gigabit wireless access. ISPs started deploying this technology in East Asia to differentiate their broadband offering and it is now being adopted by ISPs in the Middle East, including Jordan (Umniah and Zain), Qatar (Ooredoo), Saudi Arabia (Salam, stc), and the U.A.E. (Etisalat by e&).

Making gigabit internet more accessible will unlock faster speeds and drive wider adoption

Countries with small landmasses and populations, and high urbanization, such as Singapore, the U.A.E., Hong Kong (SAR), Iceland, and Monaco, top the Global Speedtest Index. While such geographical and demographic characteristics give an advantage to smaller nations as they facilitate the deployment of fiber infrastructure, other factors including market competition, government support, and service affordability are key to driving mass adoption.

Many of the top 10 markets in the Global Speedtest Index have multiple ISPs competing which drives investments in better technology and continuous upgrades to attract customers. A competitive landscape benefits consumers because it helps to keep prices relatively low. It also accelerates increases in median speeds as ISPs tend to offer free speed upgrades to existing customers. For example, in Hong Kong (which had 28 licensed ISPs as of March 2024) and Singapore, gigabit broadband speeds have been available to residential customers since the early 2010s, and ISPs have eliminated sub-1 Gbps plans. As a result, 85% of residential homes in Singapore and 68.0% in Hong Kong have at least 1 Gbps services. Chile, Latin America’s leader in fixed line performance and fourth in the Speedtest Global Index in Q1 2024, has six ISPs with more than 5% market share, all of which are heavily focused on migrating customers to fiber.

Governments in these leading countries have also prioritized strong digital infrastructure development with significant investment in infrastructure. For example, China has pursued a state-coordinated infrastructure deployment program to promote economic development. In France, the government’s “France Très Haut Débit” initiative aimed to provide fiber optic access to all citizens by 2025 through public-private partnerships. The Singaporean government invested S$1 billion to build the infrastructure of its National Broadband Network (NBN) which supported speeds of up to 10 Gbps and reached more than 95% premises in 2013. In February 2023, it announced an additional investment of up to S$100 million to upgrade the NBN to enable more than half a million households to benefit from speeds of up to 10Gbps by 2028.

While the broadband infrastructure in some countries from the Middle East is gigabit internet-ready, the disparity in income and the high price of these packages hinder the adoption rate of high-speed broadband services. For example, a 1 Gbps fiber line in Hong Kong or Singapore could cost as little as $30 per month, and a plan with a similar speed starts at $100 per month in Qatar, $150 in the U.A.E., $250 in Saudi Arabia, and $345 in Bahrain. This highlights the need to make gigabit plans more affordable if the operators want to boost fiber subscribers and countries aspire to move up the Speedtest Global Index.

As demand for high-speed internet continues to grow, we expect increased adoption of 10 Gbps speeds to support more demanding applications and improve the user experience. Work is underway in some developed markets to build higher-capacity broadband networks to enable new cases and make the infrastructure future-ready. For example, In March 2024, Hong Kong Telecom announced the availability of 50 Gbps lines for residential and business customers. This trend is slowly emerging in the Middle East – Etisalat by E& in the U.A.E and Ooredoo in Qatar announced early experiments with 50G PON technology. We anticipate continued innovation and competition in the region, driving further advancements that will ultimately benefit end-users by delivering faster and more affordable gigabit connectivity options.

For more information about Speedtest Intelligence data and insights, please contact us.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

As 5G adoption increases, consumers and businesses expect the same level of coverage and performance wherever they go. Yet, the characteristics of 5G, which typically operates in mid-band frequencies of 1.8 GHz to 3.5 GHz, pose a challenge for indoor coverage, as these frequencies struggle to penetrate walls and windows depending on the materials used in construction. Therefore, operators need to invest in additional solutions to enhance indoor coverage and potentially offload onto in-building Wi-Fi systems.

In the Gulf region, where shopping malls are central to the economic and social lifestyle, bridging the indoor-outdoor coverage gap is ever more important. In this article, we use data from Cell Analytics™ to benchmark indoor 5G coverage provided by seven mobile operators across 28 malls in Qatar (Doha), Saudi Arabia (Jeddah and Riyadh), and the U.A.E. (Abu Dhabi and Dubai) based on crowdsourced measurements collected between December 2022 and November 2023.

Key takeaways

Good indoor coverage is vital for 5G more than for previous generations. Indoor 5G coverage is more crucial than ever since people spend 90% of their time indoors, and an increasing number of consumers and businesses depend on its availability and expect near gigabit speeds wherever they are.

Top U.A.E. malls have superior indoor 5G coverage compared to top malls in Qatar and Saudi Arabia. du leads the way in the U.A.E. (particularly in Abu Dhabi), while in Saudi Arabia, Mobily has the edge in terms of the number of malls where it has better indoor 5G coverage. In Qatar, Ooredoo comes first for indoor coverage and its lead over Vodafone is more evident than in the other two countries.

Efficient deployment of indoor network coverage solutions requires addressing non-technical challenges. Beyond cost and technical factors, operators must anticipate other issues when aiming to improve indoor coverage, such as site acquisition and permission and compliance, all of which can be facilitated through regulatory measures.

5G underscores the importance of indoor coverage more than previous generations of mobile technologies

Before 4G, mobile networks were designed primarily for outdoor voice coverage. That is why outdoor deployment took precedence over indoor coverage in previous generations of mobile networks since coverage maps were important marketing collateral to grow market shares. With 5G, consumers and businesses expect high-speed and consistent mobile connectivity everywhere. As they rely heavily on continuous 5G availability, operators are pressured to deliver a similar quality of experience indoors and outdoors. Delivering consistent high-speed data connectivity across both indoor and outdoor networks is far more challenging since the performance of a 5G network is limited by interference.

5G is also the main data growth driver of usage for the operators and most of the usage is likely to be generated indoors. According to Ericsson, we spend 90% of our time indoors, and up to 80% of our data is consumed indoors. Therefore, operators should strive to improve coverage and capacity indoors if they want to capitalize on data growth, reduce churn, and support new consumer and business use cases.

Indeed, 5G enables a wide range of applications because it supports high bandwidth, low latency, and high device density. As 5G adoption increases, there will be more use cases where an excellent indoor 5G experience will be essential to end users and commercially beneficial to the operators.

Technical and commercial reasons also explain why indoor 5G performance is typically inferior to outdoors. The mid-band frequencies (1.8 GHz to 3.5 GHz) used in 5G deployment do not effectively penetrate walls and windows. The increasing use of insulating materials and metal structures further hamper the propagation of radio waves. Furthermore, indoor network systems need to be designed to fit within the site-specific requirements for antenna placement, connectivity, and power distribution systems, minimize interference with careful coordination between adjacent sites, and connect more customers per square meter than outdoors which impacts network performance.

Commercially, operators have prioritized outdoor coverage because it requires less CAPEX and OPEX per subscriber compared to indoor coverage and has a better return on investment. Additionally, operators need to adapt their indoor network solution to suit different venues and building configurations, find other service providers to share deployment costs with, and convince venue owners to offset some of them.

Technical solutions exist to address the 5G coverage gap

Spectrum is arguably the most influential factor for 5G coverage and speed. High frequencies (shorter wavelengths) carry data faster but have a shorter range than lower frequencies, leading to lower coverage levels and inferior indoor quality of service.

Operators can opt for higher towers to cover a large area to compensate for the shorter range or adjust spectrum usage in specific areas to maximize coverage while not too negatively impacting performance.

Alternative technical solutions also exist to address indoor cellular coverage challenges (see table below). Most of these solutions were designed originally for 3G and 4G but were upgraded by increasing their power and the number of antennas to enable greater performance and improve spectral and energy efficiency. However, deploying some of these solutions can be complex and costly. For example, a DAS that supports MIMO costs multiple times a typical outdoor macro site. They may also lead to unnecessary duplication of infrastructure if operators do not share their assets.

Examples of solutions to improve indoor 5G coverage

Solution

Description

Limitations

Amplifiers

• Strengthen a weak external cellular signal by amplifying it inside the building

• Could cause interferences with signals from the macro cells

Small cells (microcells, picocells, and femtocells)

• Low-power antennas that provide localized coverage and add capacity in dense locations • Connected to the macro cell through backhaul

• More suitable for small indoor areas (e.g. a room or floor), not shopping malls • Not cost-effective to cover a large area

Distributed Antenna System (DAS)

• Set of antennas distributed around a venue to amplify the signal and provide consistent coverage and capacity throughout • DAS is connected to one or more base stations via cable

• Could be expensive and complex to deploy and upgrade due to the multiple radio heads and cable connections required

Private LTE/5G Networks

• Localized cellular networks deployed to offer customized indoor coverage and capacity solutions • Cater to specific indoor environments such as factories, warehouses, and corporate offices

• Acquiring dedicated spectrum is challenging and costly • Deployment complexity and cost can make it prohibitive for smaller organizations • Navigating regulatory frameworks can be challenging

Indoor 5G coverage is more vital in Gulf countries because shopping malls play an essential economic and social role

The Gulf region has been a global 5G pioneer. Most countries have attained nationwide 5G coverage by 2023. 5G penetration among mobile users has also skyrocketed since the beginning of 2022. It reached 28.11%, 22.48%, and 26.86% in Qatar, Saudi Arabia, and the U.A.E. in Q3 2023, according to GSMA Intelligence.

Indoor network coverage is arguably more critical in the Gulf region. The high temperatures and long summers mean that people spend most of their time indoors, especially in shopping centers. These malls are the heart of the economic, social, and cultural life in the region for residents and tourists alike.

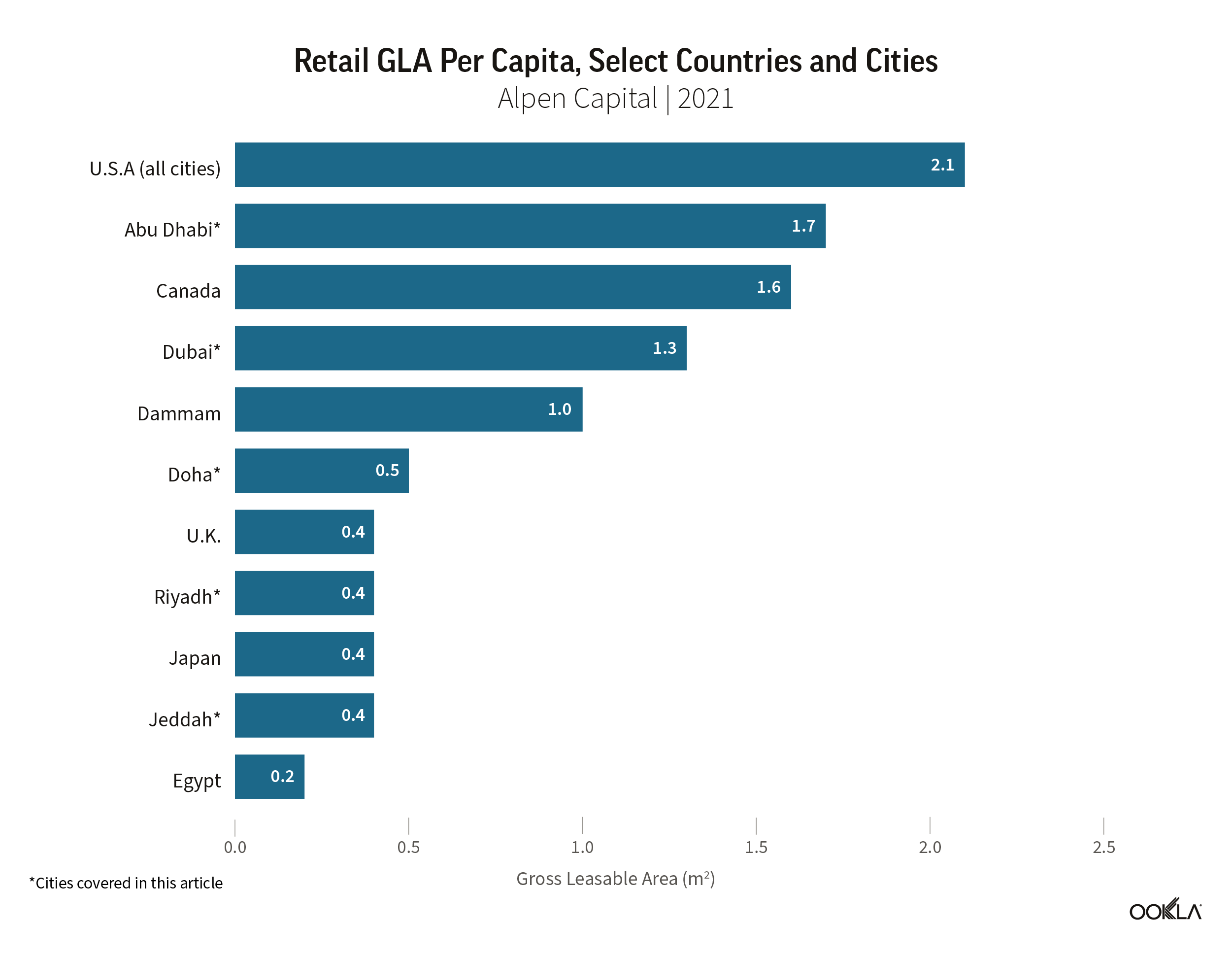

Aided by retail-friendly policies, such as low taxes and late opening times, malls experienced a boom in footfall and retail transactions. Despite the rapid rise in online shopping, especially after COVID-19 lockdowns, brick-and-mortar remains a pillar of national economies and accounts for the largest share of all retail transactions. The retail segment has also room to grow further as the retail gross leasable area (GLA) per capita across major GCC cities remains below that of developed markets like the U.S.A., despite being higher than other markets in the Middle East and North Africa.

5G connectivity inside the malls is not just crucial for consumers but also businesses. Stores can use the network to connect video cameras, point-of-sale (PoS) devices, and signage systems. Good indoor connectivity also enables shops to offer a hybrid retail experience, combining physical and digital sales channels. For example, customers can order items online for in-store pick-up. Indeed, nearly 60% of surveyed shoppers in the U.A.E. use their smartphones in-store to research products, compare prices, or look for offers. Excellent indoor 5G coverage also underpins future in-mall experiences that mix physical and digital interactions through technologies like AR/VR.

Operators and venue owners can also benefit from offering seamless connectivity in the malls. For example, operators can improve their brand image and prestige by associating themselves with iconic venues such as Dubai Mall in Dubai, Mall of Qatar in Doha, and Mall of Arabia in Jeddah. For landlords, exceptional indoor coverage and quality can serve as a key differentiator for the mall, potentially resulting in higher rental rates.

Operators can offload onto Wi-Fi as an alternative to extending 5G indoors, provided these systems are designed, optimized, and operated with equivalent quality of experience, using, for example, Ekahau®. While many malls in the region have Wi-Fi infrastructure, we believe that 5G complements rather than competes with Wi-Fi. Direct access to a 5G network offers more convenience for consumers and is intrinsically more secure than 4G or Wi-Fi.

The latest generations of Wi-Fi technology, including Wi-Fi 6 and Wi-Fi 7, are likely to play a more pivotal role in enhancing indoor coverage thanks to their improved performance, higher speeds, and increased capacity. Wi-Fi’s seamless integration with cellular coverage enables the offloading of cellular traffic in congested areas, maintains connectivity in deep indoor locations, and provides a robust and interconnected network experience for users.

Major differences in indoor 5G coverage quality between malls, operators, and countries in the Gulf region

In this analysis, we examine the variations in the strength of indoor 5G coverage across select shopping malls in Qatar, Saudi Arabia, and the U.A.E.. We use data from Cell Analytics based on crowdsourced measurements of consumers’ mobile devices worldwide. The tool captures RF measurement and data usage, both indoors and outdoors, enabling us to benchmark signal metrics and generate user density and competitive coverage difference maps.

We use the average Reference Signal Received Power (RSRP) as a measure of network coverage. RSRP represents the network signal strength received by a mobile phone. An RSRP value that exceeds -90 dBm indicates superior coverage. If the signal strength is between -90 dBm and -100 dBm then network coverage is considered good. Lower RSRP values signify lower download speeds and an increased probability of network disconnection.

In the sections below, we examine 5G RSRP measurements inside major malls in Qatar (Doha), Saudi Arabia (Jeddah and Riyadh), and the U.A.E. (Abu Dhabi and Dubai) from December 2022 to November 2023. For each location, we compare operators’ RSRP values to determine which ones offer superior 5G coverage. We included locations where we received sufficient samples to achieve a confidence level of 95%.

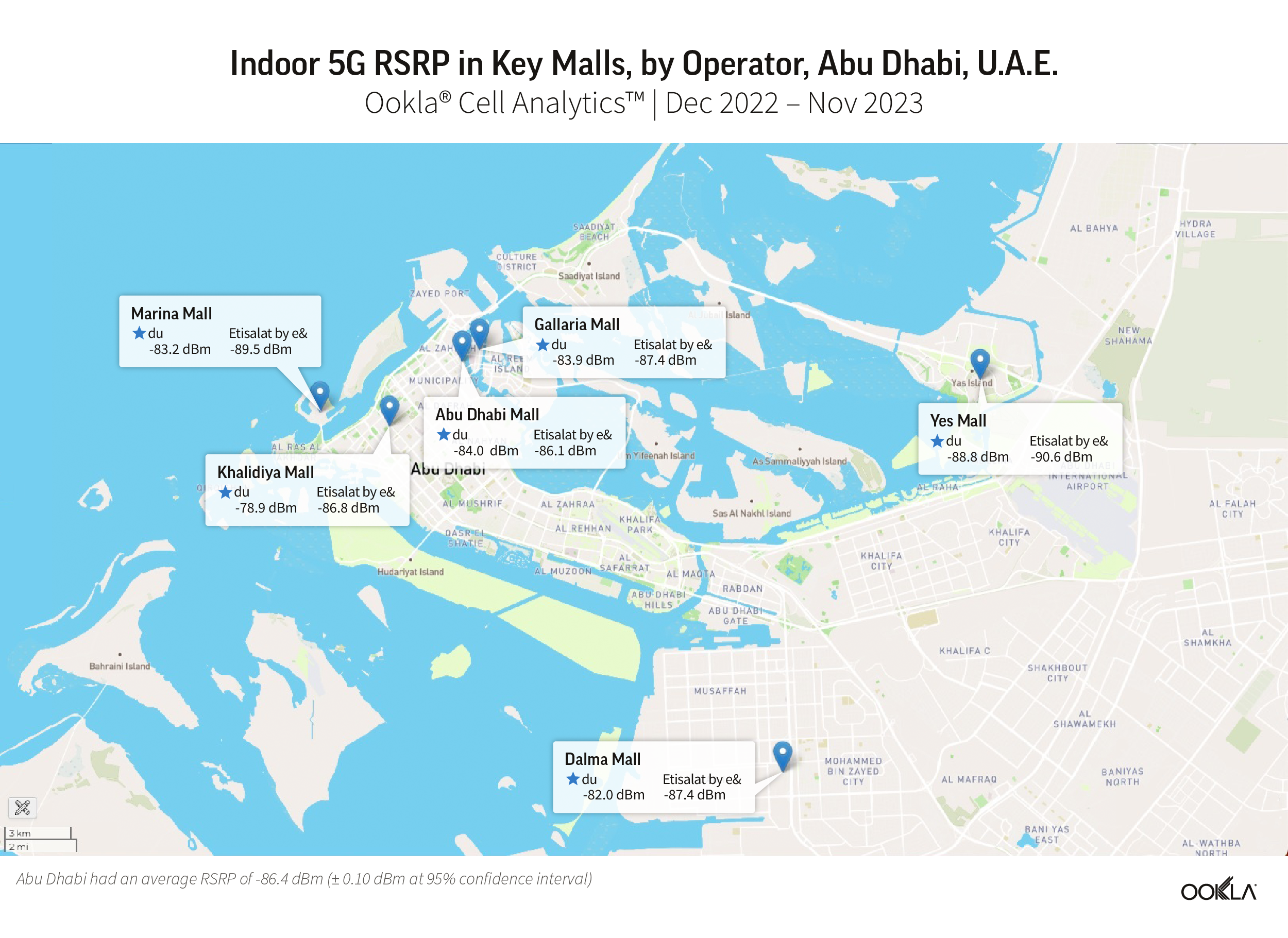

du commands a lead in indoor 5G coverage in more U.A.E. malls than Etisalat by e&

The U.A.E. emerged as the fastest 5G market globally in Q2 2023, according to Ookla® Speedtest Intelligence®. This achievement was facilitated by an almost nationwide 5G coverage of the population. Both operators, du and Etisalat by e&, have sought to continually enhance customer experience by improving network coverage and quality.

du reported 98.5% 5G coverage of the population in November 2023 and attributed much of its CAPEX to 5G deployment and specifically to enhancing indoor coverage. For example, it has installed small cell antennas in apartments and offices and expanded DAS in new mall locations. It also launched 5G Standalone (SA) and Voice over New Radio (VoNR) in 2023.

The chart below depicts indoor 5G RSRP values for du and Etisalat by e&, across 12 malls in Dubai and six others in Abu Dhabi. Both operators have the same number of malls in Dubai where they lead in indoor coverage. In Abu Dhabi, du consistently outperformed Etisalat by e& in terms of indoor coverage in all the malls we reviewed.

Overall, top U.A.E. malls have better indoor 5G coverage than those in Qatar and Saudi Arabia. The weighted average RSRP per mall is at least -86 dBm in 9 out of the 18 locations analyzed, suggesting excellent indoor coverage. However, in some locations, such as Ibn Battuta Mall, Mall of Emirates (for both operators), Wafi Mall and Yas Mall (for Etisalat by e&), and Dubai Mall (for du), the signal power is equal or less than -90 dBm.

du consistently outperforms Etisalat by e& in indoor 5G coverage across all the six malls in Abu Dhabi. For example, du is 10% better than Etisalat by e& in Khalidiya Mall and 8% better in Marina Mall.

The difference in signal power in Dubai locations is generally smaller, implying that consumers are unlikely to perceive a difference in 5G coverage while shopping there. For example, the RSRP gap between operators is inferior to 1.5 dBm in Deira City Mall, Festival City Mall, Ibn Battuta Mall, Mirdif City Centre, and Wafi Mall. This could be because both operators share the same indoor coverage infrastructure in these malls to avoid duplication and to reduce costs.

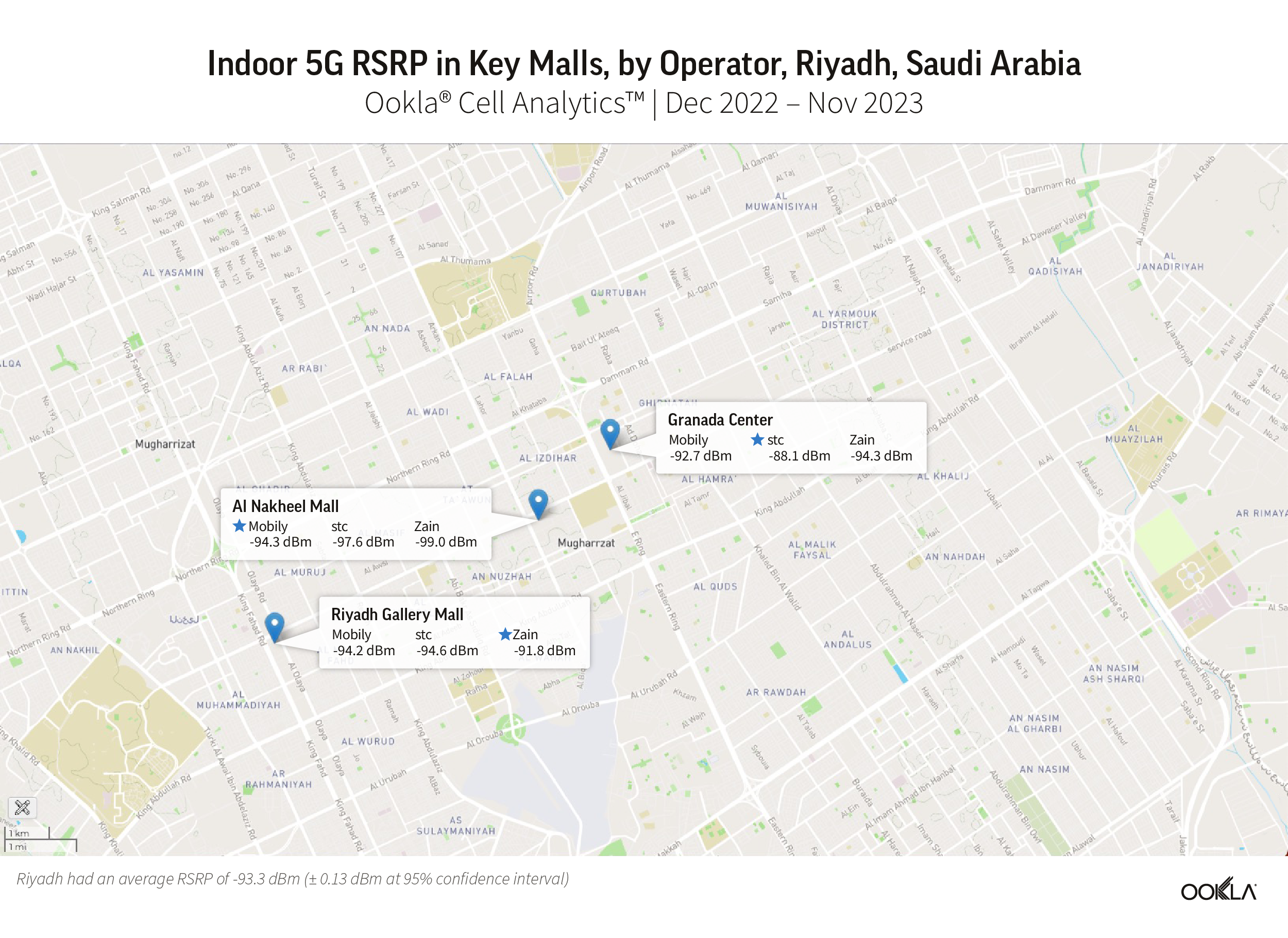

Mobily and Zain are the frontrunners for indoor 5G coverage in Saudi malls

The Saudi Communications, Space & Technology Commission (CST) reported that 5G coverage reached 97 governorates in March 2023 (out of 136 governorates), up from 84 a year earlier. This is a substantial jump from the 35 governorates it first reported in Q2 2020.

This improvement is partially driven by the ongoing release of suitable spectrum for 5G. Indeed, operators had access to low-band spectrum (700 MHz and 800 MHz) from 4G that they could reuse for 5G, and auctions for 2.3 GHz, 2.6 GHz, and 3.5 GHz bands were completed in 2019. The CST also plans to auction 600 MHz, 700 MHz, and 3800 MHz bands in Q1 2024.

Operators have steadily invested in 5G infrastructure. stc reported that it provides 5G coverage to over 90% of its mobile site locations in major cities. In October 2023, it announced significant network investments to extend its reach to over 75 cities and governorates.

The two charts below show indoor 5G RSRP values for Mobily, stc, and Zain across three malls in Riyadh and three others in Jeddah. Despite the large investments in 5G infrastructure and access to low-band spectrum, Cell Analytics reveals a weighted average RSRP of -95.5 dBm across the six surveyed malls, which is significantly lower than the weighted averages in Qatar and the U.A.E. at -85.3 dBm and -87.4 dBm, respectively.

Saudi Arabia is home to the five malls with the poorest indoor 5G coverage among the 28 malls analyzed in this article. The RSRP weighted averages ranged from -98.8 dBm in Al Salam Mall in Jeddah to -93.8 dBm in Riyadh Gallery Mall in Riyadh (the other lagging malls are Mall of Arabia and Red Sea Mall in Jeddah, and Al Nakheel Mall in Riyadh).

Mobily had better indoor 5G coverage than its competitors in three malls while Zain outperformed them in two of the malls. Mobily is quite ahead of its competitors in Mall of Arabia, one of the biggest malls in Saudi Arabia, with an RSRP of -92.8 dBm, a signal strength that is 6.5 dBm higher than Zain’s and 8.8 dBm stronger than stc’s.

Zain leads Mobily in two malls, Riyadh Gallery Mall and Red Sea Mall, by 2.4 dBm and 1.7 dBm, respectively. On the other hand, stc leads in 5G coverage inside Granada Center with an RSRP of -88.1 dBm, the highest signal power among the analyzed malls in Saudi Arabia. The RSRP difference between the three operators in the other malls varies between 3.3 dBm and 4.6 dBm, which suggests that operator choice can affect signal reception when shopping in these venues.

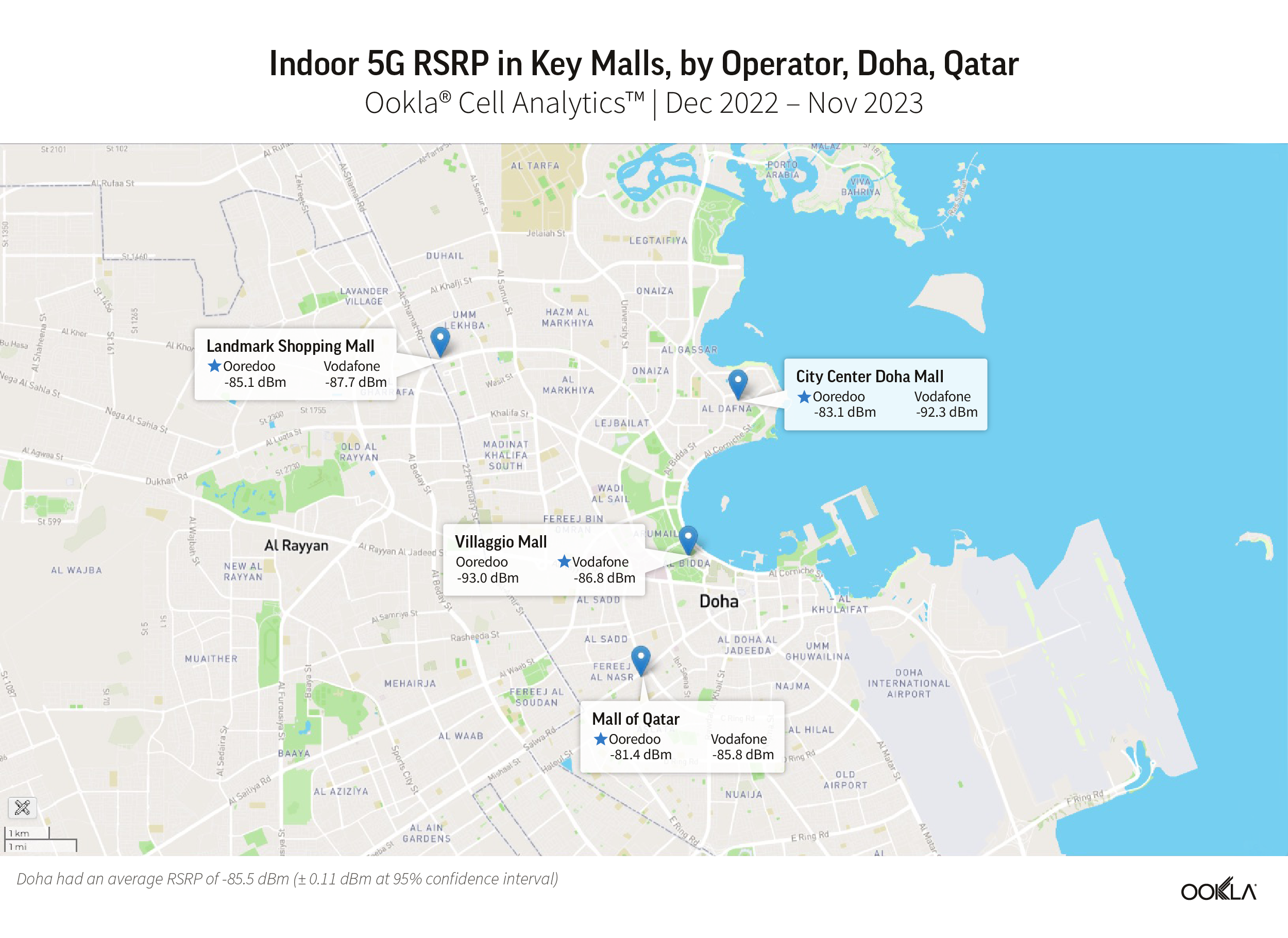

Ooredoo leads in 5G coverage inside the malls in Qatar

Likewise, Vodafone nearly doubled its radio network sites, upgraded the existing sites’ technologies, and increased 5G coverage, especially indoors. It reported that over 1188 TB of data were consumed across all stadiums during the World Cup. These initiatives helped to make Vodafone the world’s fastest mobile network operator in 2022. By June 2023, 85% of Vodafone’s 2250 radio network sites were 5G enabled.

The chart below shows indoor 5G RSRP values for Ooredoo and Vodafone across four malls in Doha. It reveals that Ooredoo delivered superior indoor coverage in all of them, except for Villaggio Mall, where Vodafone outperformed.

The difference in RSRP is highest in City Center Doha Mall where Ooredoo was ahead of Vodafone by 9.2 dBm. In the country’s largest shopping center, the Mall of Qatar, the difference in indoor signal strength between the two operators is sizable, standing at 4.4 dBm. However, since both operators offer excellent coverage simultaneously, with an RSRP of -81.4 and -85.8 for Ooredoo and Vodafone, respectively, consumers are unlikely to perceive a difference in coverage.

Operators need to consider non-technical aspects when deploying indoor solutions

Measures should be in place to encourage operators to make indoor network deployments more efficient. For instance, the Chinese government mandated that operators share the mid-band spectrum (3.3-3.4 GHz) for indoor coverage to promote co-development and cost-sharing. In Europe, mobile network operators (MNOs) share indoor networks deployed by neutral hosts, such as Cellnex, with a revenue model based on charging the venue or building owner for the network instead of the operator.

In the United States, the primary ownership model for DAS often involves a combination of ownership by neutral host operators, MNOs, and venue owners depending on agreements, partnerships, and specific needs of the venue or location. Neutral host operators often play a significant role in deploying shared DAS infrastructure, while venue owners, managers, or MNOs may also have ownership stakes or involvement in specific deployments to enhance indoor wireless coverage.

Beyond cost and technical considerations, operators need to carefully address other factors and practical challenges before and during the implementation of an indoor network coverage solution. These include site acquisition and permission, physical space and aesthetics, and regulatory compliance needs.

Regulators can have a proactive role in reducing bureaucratic hurdles and encouraging government-industry collaboration. For example, in South Korea, the regulator promotes the parallel development of indoor and outdoor 5G coverage across the country. Another example is the Telecom Regulatory Authority of India (TRAI) which recently requested industry views on the mechanism to rate digital connectivity in buildings. TRAI’s initiative illustrates the importance of devising standard guidelines, incentivizing investments in in-building infrastructure, and ultimately ensuring seamless and reliable indoor connectivity for consumers and businesses.

Ookla can support operators and venue owners in improving indoor cellular coverage

As consumers’ expectations for network speed and consistent connectivity rise with the advent of 5G, operators should prioritize addressing indoor coverage issues to improve customer experience, drive data usage, and outperform their competitors.

As more consumers and businesses rely on 5G, an excellent indoor 5G experience will become even more essential. It will also pave the way for innovations that blend in-store with digital experiences. The future of physical malls in the region hinges on their ability to adopt new technologies and use them to transform the consumer experience.

Ookla can assist operators in identifying buildings or indoor venues with coverage or capacity issues using crowdsourced and controlled test data and the execution of precise walk tests for diagnosis. Cell Analytics helps to identify specific indoor areas with low signal-to-interference-and-noise ratio (SINR) and signal quality (RSRQ), causing sluggish data speeds despite adequate coverage (RSRP).

Equipped with this knowledge, mobile network operators can promptly deploy personnel for on-site walk-tests using Wind™, Ookla’s handheld walk-and-drive controlled testing platform. Wind enables testers to simulate user behavior while meticulously capturing detailed RF data in the background and processing it in near-real time. This allows operators to implement corrective actions to boost network performance within any venue.

An alternative to deploying in-building 5G systems is to selectively offload usage to Wi-Fi provided these systems are designed, optimized, and operated to deliver an equivalent quality of experience – this can be done using Ekahau.

Ookla retains ownership of this article including all of the intellectual property rights, data, content graphs and analysis. This article may not be quoted, reproduced, distributed or published for any commercial purpose without prior consent. Members of the press and others using the findings in this article for non-commercial purposes are welcome to publicly share and link to report information with attribution to Ookla.

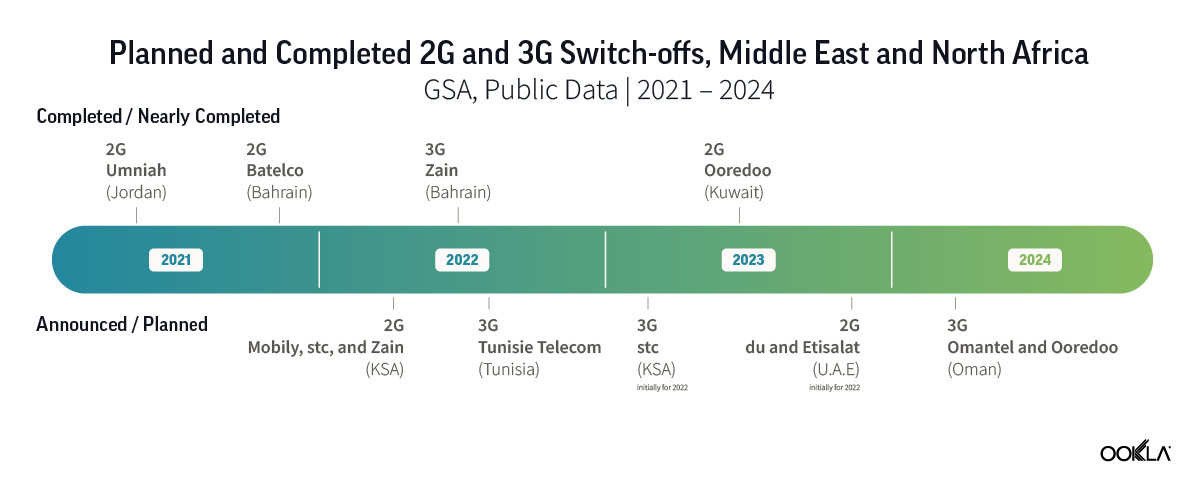

Operators seek additional spectrum, a generally scarce and costly resource, to improve the coverage and capacity of 4G and 5G networks. This need led to the decommissioning of legacy technologies and the refarming (i.e. repurposing) of existing spectrum. In this article, we examine operators’ plans for sunsetting 2G and 3G networks in the Middle East and North Africa (MENA), focusing on developments in Oman, Saudi Arabia, and the U.A.E. We evaluate the impact of network shutdowns on performance and customer satisfaction for operators that completed the process and highlight key considerations for a successful network transition to mitigate commercial and brand risks.

Key Takeaways:

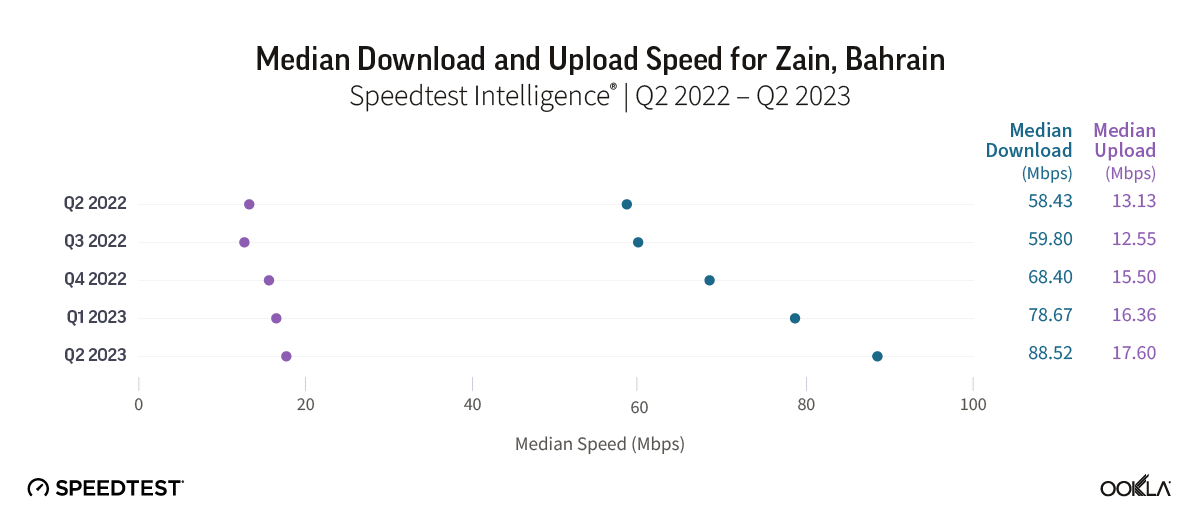

Sunsetting legacy networks contribute to improvements in performance and customer satisfaction. For example, Zain Bahrain, which decommissioned its 3G at the end of 2022, saw its median download speed increase from 58.43 Mbps in Q2 2022 to 88.52 Mbps in Q2 2023, while customer satisfaction ratings climbed steadily throughout 2023.

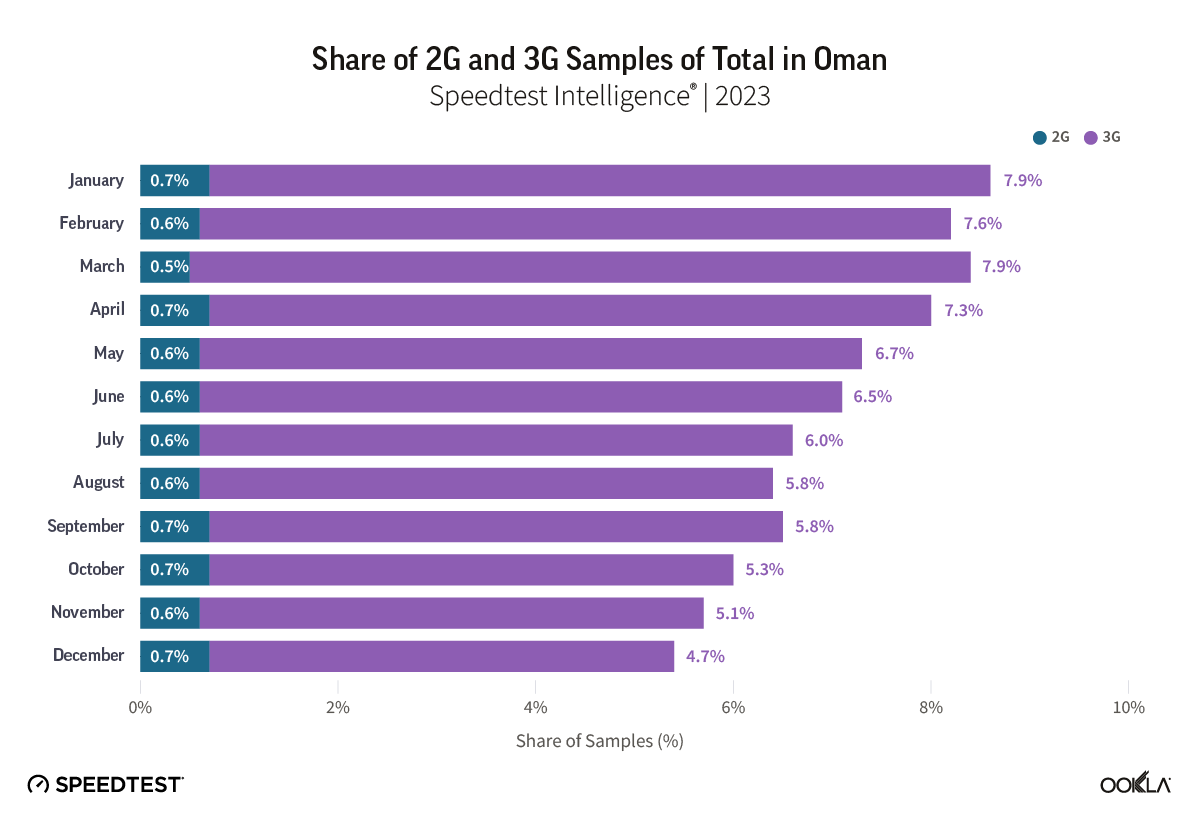

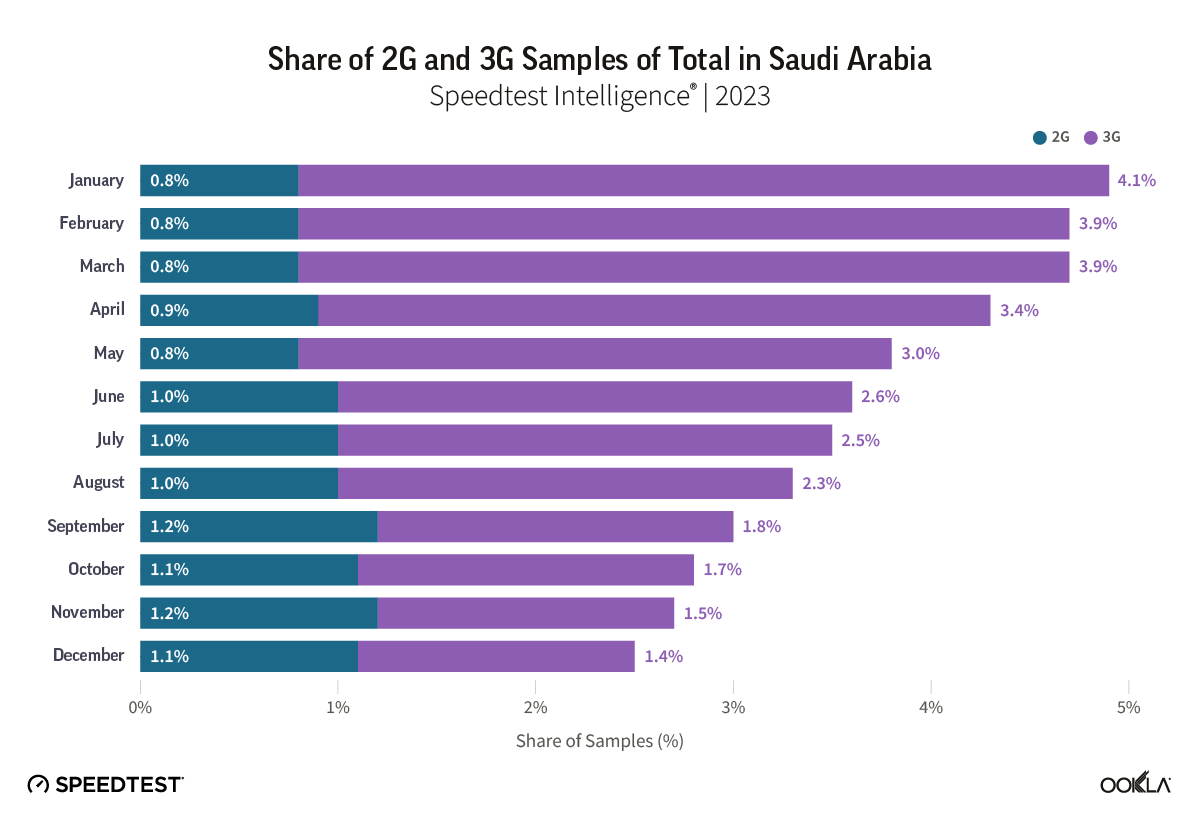

Gulf operators are generally on track to phase out their old networks by the end of 2024. Our data indicate that 3G share of samples in Oman dropped to 4.7% by the close of 2023 in anticipation of the scheduled shutdown of 3G services by Q3 2024. In Saudi Arabia, stc saw its 3G share of samples fall sharply in 2023, suggesting that the phase-out process is nearing completion. Meanwhile, 2G share of samples in the UAE dropped rapidly in 2023 as operators planned to turn off 2G by the end of the year.

A carefully managed, phased approach is crucial to minimize service disruption during the transition from 2G/3G to advanced networks. Retiring old technology can reduce operating and maintenance costs, optimize spectrum use, simplify network management, and accelerate service innovation. However, operators need to take into consideration existing deployments, potential revenue loss, traffic on older networks, and market readiness for 4G and 5G.

Network sunsetting – still an emerging trend in MENA

Operators across the globe are prioritizing the retirement of 2G and 3G networks to refarm spectrum for the more efficient 4G and 5G technologies. This shift aims to lower their operating costs and direct investments from maintaining outdated systems to deploying more efficient networks that support faster speeds and greater capacity.

The decision of which network to turn off first and the associated timeline varies depending on market conditions and operator readiness. In Asia, operators in China and Japan opted to decommission 2G networks while in Europe, operators typically retire (or plan to retire) 3G before 2G due to the latter’s widespread use in Internet of Things (IoT) applications in the utility and automotive industries. In the U.S.A., the three main operators, AT&T, T-Mobile, and Verizon completed their 3G sunsetting in 2022. However, that has not happened without hiccups. For example, carmakers including BMW, Ford, Porsche, and Volkswagen faced lawsuits because some of their car models’ connected services were rendered obsolete due to the 3G shutdown

The MENA region had fewer completed and planned legacy sunsets compared to Asia and Europe, with diverse strategies between and within markets. For example, in Bahrain, Batelco shut down its 2G network in November 2021, while competitors, stc and Zain, turned off their 3G networks in 2022. We expect network sunsets to peak by 2025 in the region as 4G becomes more prevalent, and 5G gathers momentum in the region. Some operators in Bahrain and Jordan, have either completed or made significant progress in their sunsetting efforts. Operators in Oman, Saudi Arabia, Tunisia, and the U.A.E. either initiated the process of sunsetting 2G or 3G or will do so within 1 to 2 years.

Network sunsetting can increase efficiency, reduce costs, and improve customer satisfaction

The phasing out of older technologies enables operators to greatly simplify network management since maintaining multiple radio technologies requires significant resources and personnel expertise. By streamlining their infrastructure, operators can reduce operational costs, direct resources towards optimizing 4G and 5G networks, and deploy innovative services based on newer technologies.

4G and 5G are also many times more spectral efficient than their predecessors. That means that modern networks can transmit much more data over the same spectrum than previous standards, and support more users per cell site. According to Coleago Consulting, while 2G and 3G can deliver 0.16 and 0.8 bits/Hz, respectively, 4G with a 2×2 MIMO antenna can deliver 1.9 bits/Hz, and the figure jumps to 4.8 bits per hertz for 5G with advanced 16×16 MIMO. This efficiency gain is important as the demand for high-speed and low-latency services grows in the MENA region. GSMA Intelligence expects mobile data traffic per smartphone will quadruple in Sub-Saharan Africa by 2028 to 19 GB per month, while the Middle East and North Africa will experience more than a threefold increase to 37 GB per month.

Refarming spectrum for 4G or 5G not only boosts capacity and expands service coverage but also saves operators from the expensive process of bidding for new spectrum. By freeing up the 900 MHz, 1800 MHz, and 2100 MHz bands, commonly used for 2G and 3G, operators can take advantage of their superior propagation characteristics to extend 4G/5G reach with fewer sites.

Furthermore, modern network equipment is more energy-efficient than older systems. This can help operators reduce their energy costs, lower OPEX, and progress towards sustainability goals. Case in point, Vodafone (UK) reported that sending 1 TB of data across 5G will use just 7% of the energy required for the same transfer over 3G. O2 Telefónica (UK) claimed a 90% reduction in power consumption per transmitted byte following the retirement of its 3G network in 2021.

The deployment of modern technologies also translates to greater throughput and potentially reduced costs for end-users. Ookla’s Speedtest Intelligence® data shows that operators that deactivated 2G or 3G networks improved their median download and upload speeds. For example, Zain Bahrain began 3G sunsetting in February 2022, refarmed the 2100 MHz spectrum, and gained access to 20 MHz bandwidth of contiguous spectrum. This move improved 4G capacity and spectral efficiency compared to using carrier aggregation. Switching off the 3G network at the end of 2022 (the first in the Middle East) combined with more 4G sites deployed resulted in increasing the operator’s median download speed from 58.43 Mbps in Q2 2022 to 88.52 Mbps in Q2 2023 while customer satisfaction ratings climbed steadily throughout 2023.

Operators should carefully plan the network sunsetting process to minimize service disruption

Careful planning is essential to minimize service disruption and negative impacts on finances and brand. Since this process should involve many stakeholders, including enterprise customers, and consumers, operators should expect 2 to 4 years to complete the switch-off.

Pulling the plug on 2G or 3G means disconnecting many consumers who use voice and SMS, potentially leading to massive churn and exacerbating the digital divide. The question becomes then whether these users can afford to acquire a feature phone or a smartphone and upgrade to 4G and 5G plans. The impact on inbound roamers, who might face connectivity issues or be unable to access emergency services, and the potential loss of roaming revenue are additional considerations.

Insights into the usage patterns of 2G and 3G services and the volume of inbound roamers lacking LTE roaming agreements with local operators are vital to assess the financial impact. Operators should gradually turn off their legacy networks based on traffic, prioritizing areas with minimum 2G/3G activity and excellent 4G/5G coverage. Regions with high 2G/3G presence should be last to transition.

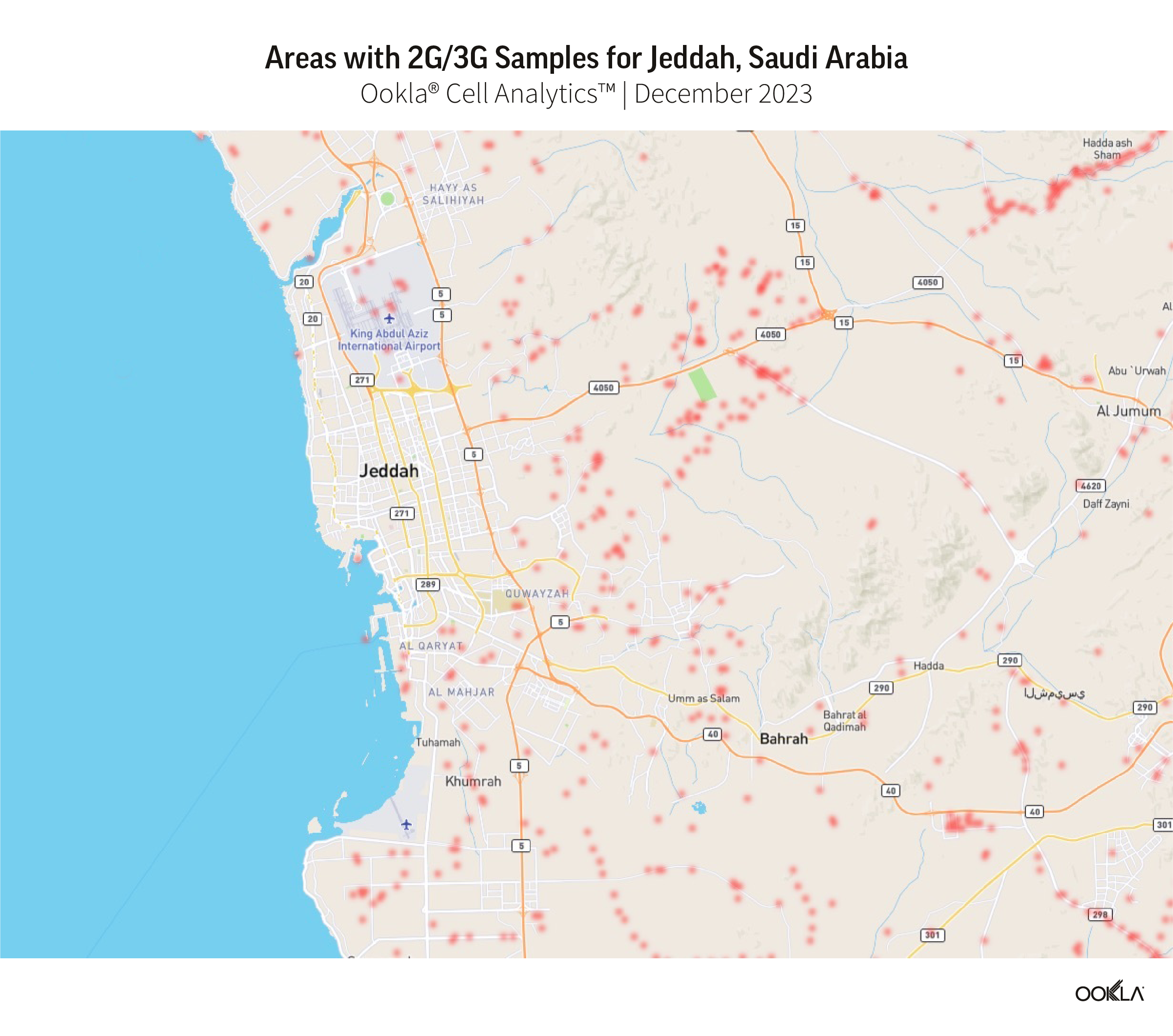

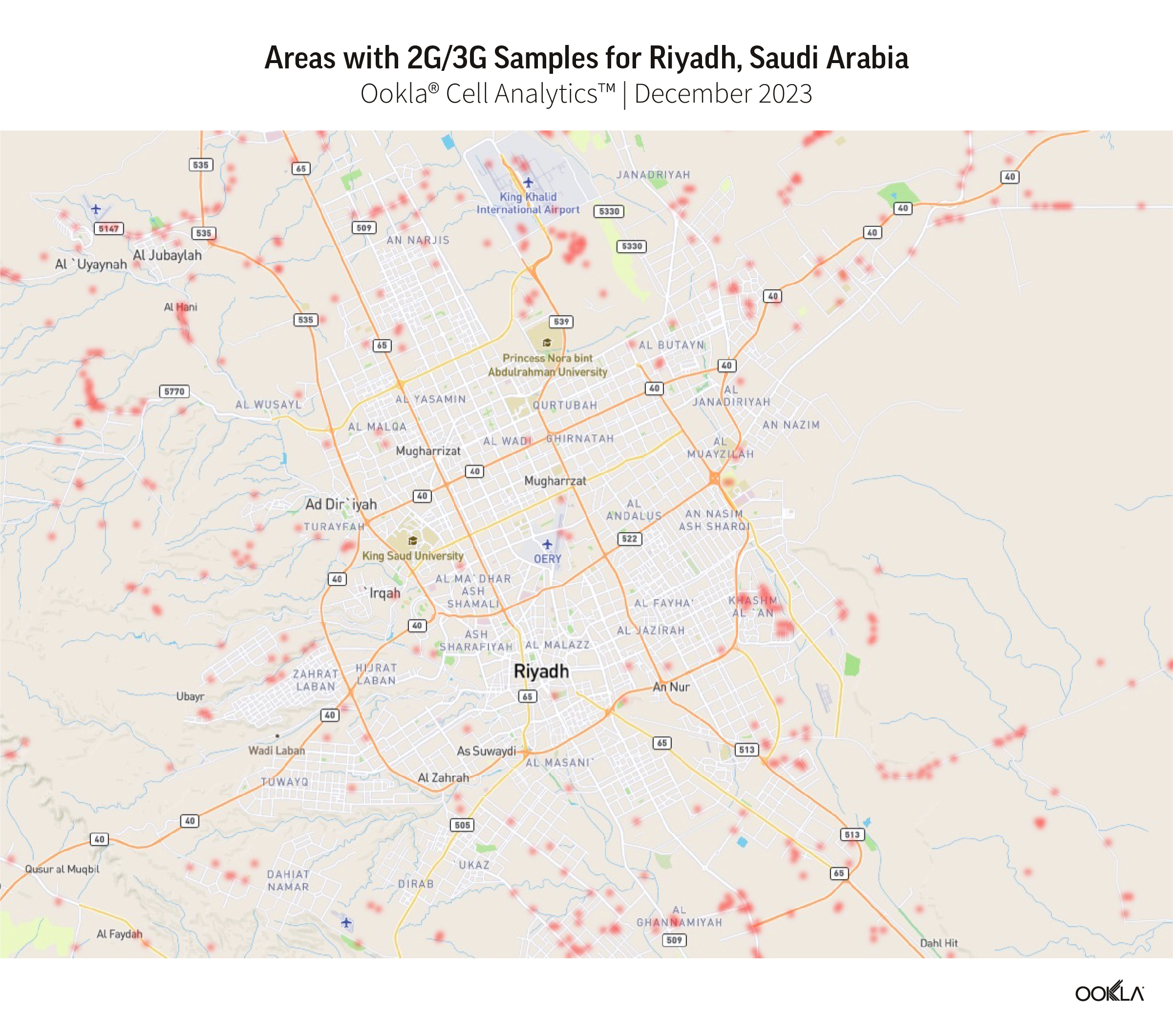

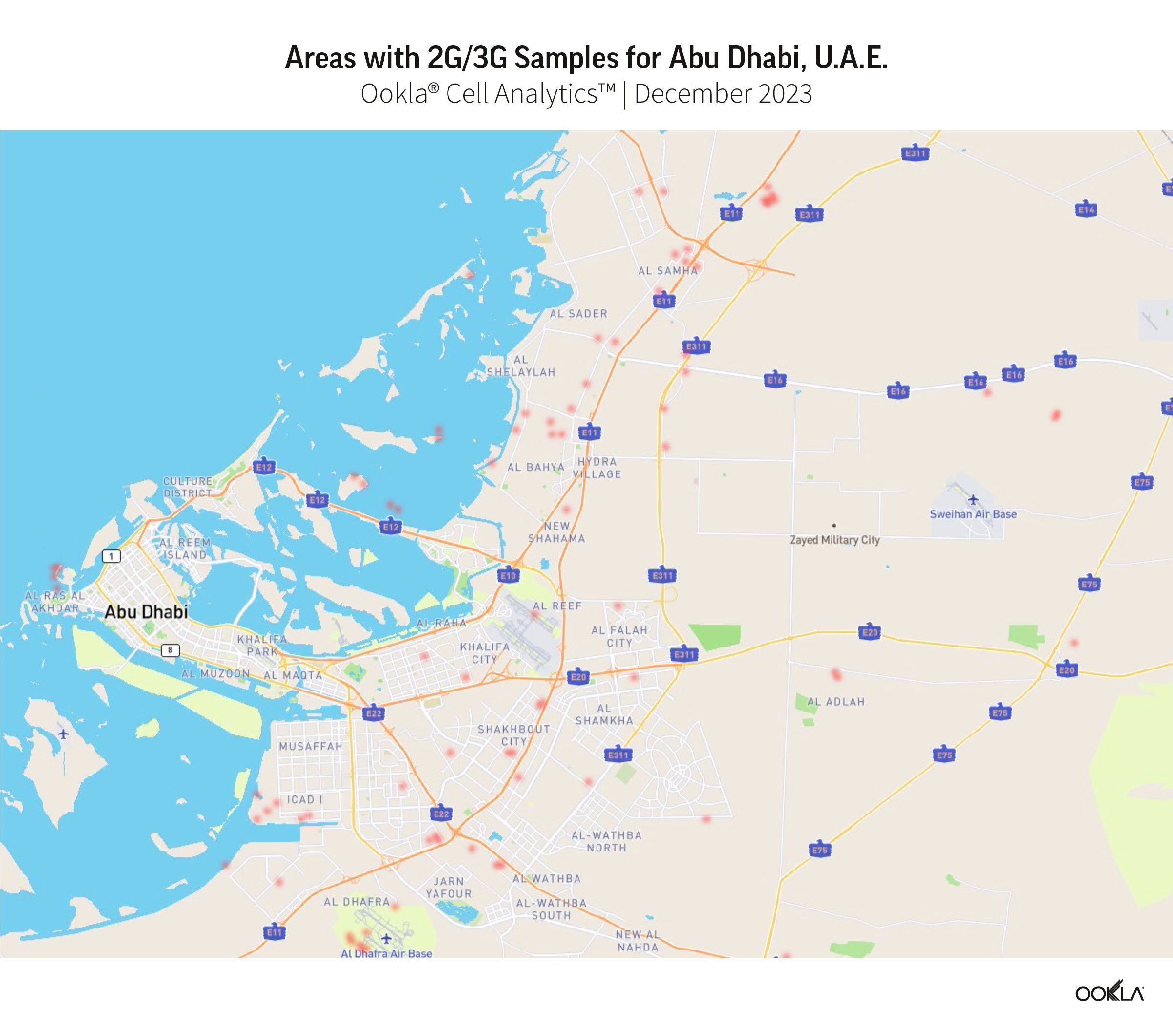

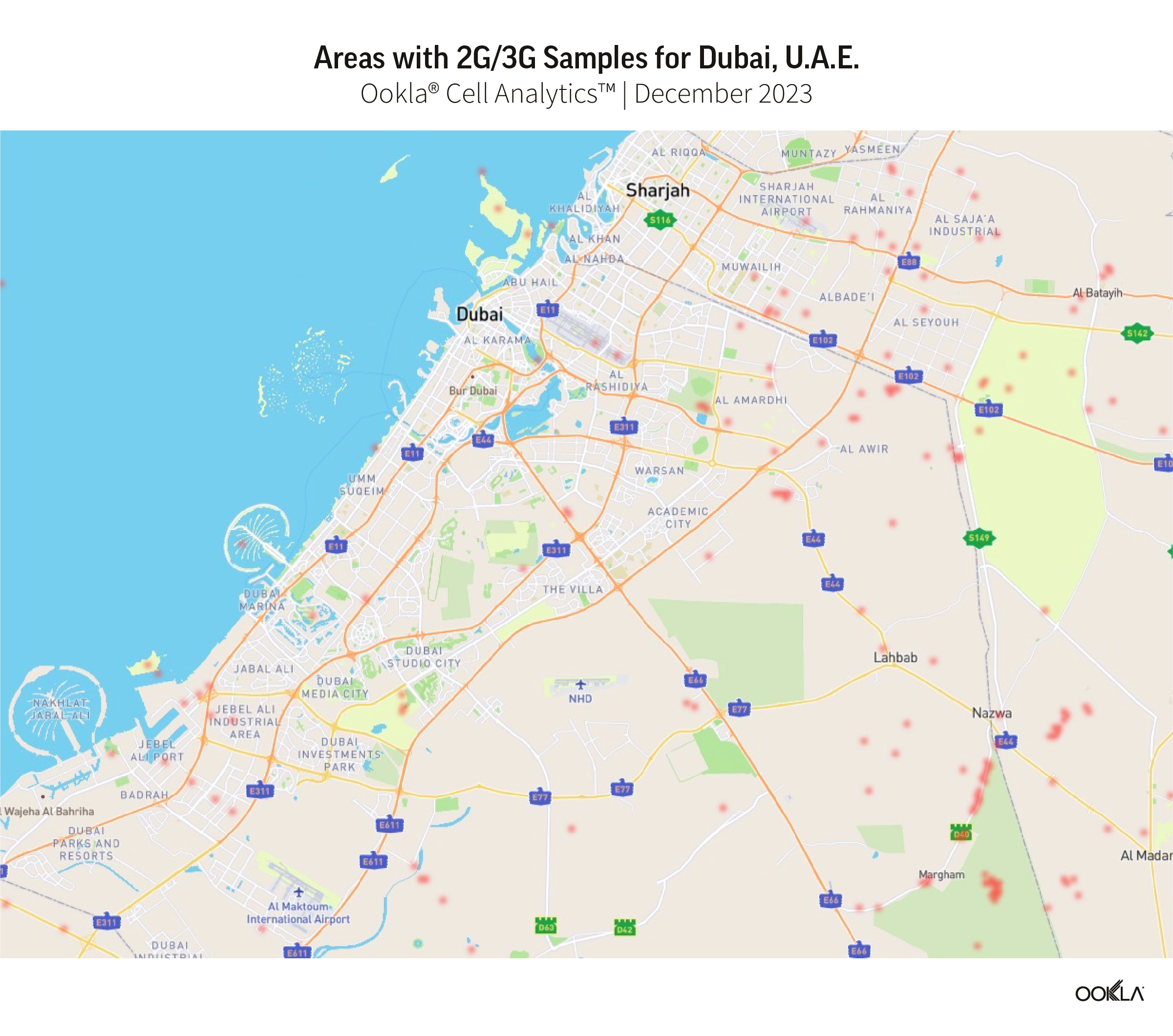

We used Ookla’s Cell Analytics™ to identify geographical regions with a concentration of 2G and 3G users in three countries, Oman, Saudi Arabia, and the U.A.E., that plan to sunset either or both technologies. The red dots on the map pinpoint customers connected to 2G and 3G because they have SIM cards not provisioned for LTE (including roamers), lack 4G coverage, or use devices incompatible with 4G. The maps below provide a high-level view of the coverage and activity level of the legacy network in each city. We used background measurements captured in December 2023.